.jpg)

30 Essential Final Accounts Questions & Answers

Final Accounts, also known as Financial Statements, represent the culmination of the accounting cycle for a business entity. There are certain Final Accounts Questions that you must be well aware off.

They are prepared at the end of the accounting period (usually a year) to determine the financial performance and position of the organization. The primary components include the Trading Account, Profit and Loss Account, Profit and Loss Appropriation Account (for companies), and the Balance Sheet.

Final Accounts Questions are a fundamental part of accountancy examinations at school, college, and professional levels (such as CA, CS, CMA, Class 11 & 12 CBSE/ISC). These questions test students’ understanding of preparing accounts from trial balance, making adjustments (e.g., outstanding expenses, prepaid expenses, depreciation, bad debts, provisions, accrued income), closing stock valuation, and presenting final statements in proper format (horizontal or vertical).

Table of Contents

- List Of Final Accounts Questions & Answers

- 1. What Are Final Accounts?

- 2. Why Is The Trading Account Prepared?

- 3. Which Expenses Are Debited To Trading Account?

- 4. Where Do You Show “ Salary To Partners” in The Final Accounts Of A Partnership Firm?

- 5. What Is The Treatment Of Interest on Drawings?

- 6. Closing Stock Appears In Trial Balance Where Will You Put It?

- 7. How Do You Treat “Provision For Doubtful Debts Appearing In Trial Balance?

- 8. Managers Commission Is 10% On Net Profit After Charging Such Commission. How It Is Calculated?

- 9. What Is The Double Entry For Creating A Reserve For Doubtful Debt?

- 10. Where Is Discount On Issue Of Debentures Are Showed?

- 11. Goods Are Sent On Approval Basis. Sales Value ₹50,000, Cost ₹40,000. Customer Has Not Responded Till Year-end. Treatment?

- 12. What is the treatment of “Bad Debts Recovered”?

- 13. Accrued Income And Unearned Income – Where Are They Shown?

- 14. How Do You Treat “Loss Of Stock By Fire” If The Insurance Claim Is Not Yet Settled?

- 15. What Is The Difference Between Provision And Reserve?

- 16. Can Gross Loss Occur? Give An Example.

- 17. Prepaid Expenses Appear In Trial Balance. How Will You Treat Them?

- 18. Why Is Depreciation Charged Even When The Business Is Incurring Losses?

- 19. What Is The Treatment Of “Dividend Received” In Final Accounts?

- 20. Where Do You Charge “Preliminary Expenses”?

- 21. How Is “Proposed Dividend” Shown In The Balance Sheet?

- 22. Where is “Unclaimed Dividend” shown?

- 23. What Is “Deferred Revenue Expenditure”? Give Two Examples.

- 24. How Do You Treat “Fictitious Assets”

- 25. Difference between Outstanding Expenses And Prepaid Expenses.

- 26. Why is “Drawings” Deducted From Capital In The Balance Sheet?

- 27. What Is “Contingent Liability”? Give examples.

- 28. Where Is The “Share Forfeiture Account” Shown After Reissue Of Shares?

- 29. How Is “Interest On Capital” Treated In Final Accounts Of A Company?

- 30. A machine purchased on 1st Oct 2024 for ₹2,00,000. Rate of depreciation 10% p.a. on straight-line basis. What is the depreciation for the year ending 31st March 2025?

- Bonus Questions For Final Accounts

- Final Takeaway

List Of Final Accounts Questions & Answers

Final Accounts, also known as Financial Statements, are crucial in accounting as they summarize a business’s financial performance and position at the end of an accounting period. They include the Trading Account (for gross profit), Profit and Loss Account (for net profit), and Balance Sheet (for assets, liabilities, and equity).

1. What Are Final Accounts?

Final Accounts are the comprehensive financial statements prepared at the end of an accounting period to reflect the business’s profitability and financial health. They typically consist of the Trading Account, Profit and Loss Account, and Balance Sheet. It is one of the basic Final accounts questions that you must know.

Final Accounts mark the end of the accounting cycle, starting from journal entries and ledger postings, culminating in a Trial Balance. The Trading Account calculates Gross Profit (Sales – Cost of Goods Sold), the Profit and Loss Account determines Net Profit after indirect expenses and incomes, and the Balance Sheet shows Assets = Liabilities + Capital. For companies, they adhere to Schedule III of the Companies Act, 2013 (in India) or IFRS/GAAP globally. They help stakeholders like investors and creditors assess performance.

Opt for a NAAC A + AICTE approved BBA Degree1-year paid internship + 10 Simulation Software + 4 Certifications. 90% Practical Learning. |

|

| Bachelor in Accounting and Finance |

2. Why Is The Trading Account Prepared?

The Trading Account is prepared to ascertain the Gross Profit or Gross Loss by comparing net sales with the direct cost of goods sold (COGS). It focuses on trading activities, debiting opening stock, purchases (less returns), and direct expenses like wages and carriage inwards, while crediting sales (less returns) and closing stock. Gross Profit = Net Sales – COGS.

This isolates manufacturing/trading efficiency from administrative costs. Journal entry for transfer: Gross Profit A/c Dr. to Trading A/c (if profit). It is one of the crucial final accounts questions to remember from your end. Final Accounts questions can be tricky if you are not aware of it.

3. Which Expenses Are Debited To Trading Account?

Direct expenses related to production or purchase of goods, such as opening stock, net purchases, wages, carriage inwards, freight, factory rent, power, and fuel. These are costs directly attributable to goods sold, following the matching principle. Opening stock is the previous year’s closing, purchases include cash/credit buys minus returns outward.

Wages are factory labor; carriage inwards is transport for incoming goods.

Example: If wages are ₹50,000 (factory) and ₹20,000 (office), only ₹50,000 debits Trading A/c. Adjustments like outstanding wages add to the debit side. This ensures accurate COGS calculation. In manufacturing firms, it expands to a Manufacturing Account. Pitfall: Debating carriage outwards (selling expense) – it goes to P&L.

4. Where Do You Show “ Salary To Partners” in The Final Accounts Of A Partnership Firm?

It is debited to the Profit and Loss Appropriation Account as an appropriation of profit, not as an expense in the Profit and Loss Account. This is one of the crucial final accounts questions that you should be well aware off.

In partnerships, partners’ salaries are not business expenses but distributions of profit, per the Partnership Deed. After Net Profit from P&L, it’s appropriated in Appropriation A/c along with interest on capital/drawings.

Journal: Partners’ Salary A/c Dr. to P&L Appropriation A/c.

Example: Net Profit ₹2,00,000; Partner A salary ₹50,000 → Debit Appropriation A/c, reducing distributable profit to ₹1,50,000. If no deed, no salary. For companies, director remuneration is an expense. Pitfall: Treating it as P&L expense reduces taxable profit incorrectly.

5. What Is The Treatment Of Interest on Drawings?

It is credited to the Profit and Loss Appropriation Account as it represents a charge on partners for withdrawing funds prematurely. Drawings reduce capital; interest compensates the firm for lost opportunity. Calculated on drawings amount for the period withdrawn (e.g., simple interest at 10% p.a.).

Journal: Drawings A/c Dr. to Interest on Drawings A/c; then Interest on Drawings A/c Dr. to P&L Appropriation A/c (transfer).

Example: Partner withdraws ₹10,000 for 6 months at 12% → Interest ₹600, credited to Appropriation A/c, increasing distributable profit. Shown as addition to drawings in the Balance Sheet. Pitfall: Ignoring time factor; use average period if multiple drawings.

6. Closing Stock Appears In Trial Balance Where Will You Put It?

It is shown only on the Assets side of the Balance Sheet as a Current Asset, as it implies the Trading Account has already been adjusted.

Normally, closing stock is an adjustment outside Trial Balance, credited to Trading A/c and assets in the Balance Sheet. If in Trial Balance (debit), it’s already valued and adjusted – no Trading A/c entry needed.

Example: Trial Balance shows Closing Stock ₹50,000 (Dr.) → Directly to Balance Sheet. This occurs if stock is physically verified post-Trial Balance. Pitfall: Double-counting by adding to Trading A/c again.

7. How Do You Treat “Provision For Doubtful Debts Appearing In Trial Balance?

The old provision is deducted from Debtors on the Assets side of the Balance Sheet. A new provision is calculated and debited to P&L if higher. Provision for Doubtful Debts (RDD) estimates uncollectible receivables. Old provision in Trial Balance (credit) means it’s a liability-like item. New RDD = % of Debtors after bad debts.

Journal for new: P&L A/c Dr. to RDD A/c (difference only).

Example: Debtors ₹1,00,000, Old RDD ₹5,000 (Cr. in TB), New 5% RDD = ₹5,000 → No P&L debit, deduct ₹5,000 from Debtors. If new ₹6,000, debit P&L ₹1,000. Pitfall: Forgetting to net off old provision.

8. Managers Commission Is 10% On Net Profit After Charging Such Commission. How It Is Calculated?

Commission = Net Profit before commission × Rate / (100 + Rate). For 10%, it’s X × 10/110.

This is “after charging,” so commission reduces profit before calculation. Let Net Profit before = X; Commission C = 10% of (X – C) → C = 0.1X – 0.1C → 1.1C = 0.1X → C = X/11. Journal: P&L A/c Dr. to Outstanding Commission A/c. Example: X = ₹1,10,000 → C = ₹10,000. If “before,” it’s simply 10% of X. Pitfall: Misreading “before/after” clause.

9. What Is The Double Entry For Creating A Reserve For Doubtful Debt?

Profit and Loss A/c Dr. To Reserve for Doubtful Debts A/c.

RDD is a contra-asset, reducing Debtors. It’s a P&L expense for prudence.

Example: 5% on ₹2,00,000 Debtors → Debit P&L ₹10,000, Credit RDD ₹10,000. Balance Sheet: Debtors ₹2,00,000 less RDD ₹10,000 = ₹1,90,000. Reversed if excess.

Pitfall: Confusing with Bad Debts (actual write-off).

10. Where Is Discount On Issue Of Debentures Are Showed?

It is shown on the Assets side under “Other Non-Current Assets” as a fictitious asset and gradually written off to P&L over the debenture tenure.

Discount is the difference between face value and issue price, treated as deferred finance cost. Journal: Bank A/c Dr., Discount on Debentures A/c Dr. To Debentures A/c. Written off: P&L A/c Dr. To Discount on Debentures A/c (annual portion). Example: ₹1,00,000 debentures at ₹90 → Discount ₹10,000, written off over 5 years = ₹2,000 p.a. Pitfall: Treating as immediate expense.

11. Goods Are Sent On Approval Basis. Sales Value ₹50,000, Cost ₹40,000. Customer Has Not Responded Till Year-end. Treatment?

Reduce sales and debtors by ₹50,000; add ₹40,000 to closing stock as “Stock on Approval.”

Detailed Explanation: Goods on approval aren’t sold until accepted. Journal: Sales A/c Dr. ₹50,000 To Debtors A/c ₹50,000 (reverse sale); Stock A/c Dr. ₹40,000 To Trading A/c ₹40,000. Balance Sheet: Stock includes ₹40,000. If accepted post-year, recognize next year. Pitfall: Recognizing as sale prematurely. It is one of the crucial final accounts questions to meet your needs.

12. What is the treatment of “Bad Debts Recovered”?

It is credited to the Profit and Loss Account as “Other Income.”

Bad debts recovered are unexpected inflows from previously written-off debtors.

Journal: Bank/Cash A/c Dr. To Bad Debts Recovered A/c; then Bad Debts Recovered A/c Dr. To P&L A/c.

Example: Recovered ₹5,000 from ₹10,000 bad debt → Credit P&L ₹5,000. Not added to debtors. Pitfall: Crediting to Debtors A/c.

13. Accrued Income And Unearned Income – Where Are They Shown?

Accrued Income: Current Asset in Balance Sheet. Unearned Income: Current Liability.

Accrued (earned but not received) follows accrual basis, e.g., interest receivable.

Journal: Accrued Income A/c Dr. To Income A/c. Unearned (received but not earned), e.g., advance rent.

Journal: Income A/c Dr. To Unearned Income A/c.

Example: Accrued ₹2,000 interest → Asset; Unearned ₹3,000 subscription → Liability. Pitfall: Mixing with prepaid/outstanding.

14. How Do You Treat “Loss Of Stock By Fire” If The Insurance Claim Is Not Yet Settled?

Debit P&L for net loss (Cost – Claim Admitted); show admitted claim as “Insurance Claim Receivable” asset.

Abnormal loss. Journal: Loss by Fire A/c Dr. (cost) To Purchases/Stock A/c; Insurance Co. A/c Dr. (claim), P&L A/c Dr. (excess) To Loss by Fire A/c.

Example: Stock ₹20,000 destroyed, claim ₹15,000 admitted → P&L debit ₹5,000, Asset ₹15,000. If fully insured, no P&L impact. Pitfall: Waiting for settlement; accrue based on admission.

15. What Is The Difference Between Provision And Reserve?

Provision is for known liabilities/expected losses (charge against profit); Reserve is appropriation of profit for future needs.

Detailed Explanation: Provision (e.g., RDD) reduces profit, shown as liability/contra-asset. Reserve (e.g., General Reserve) from profit, under Reserves & Surplus.

Journal for Provision: P&L Dr. To Provision; for Reserve: P&L Appropriation Dr. To Reserve. Example: Provision for Tax ₹10,000 (liability); Revenue Reserve ₹20,000 (strengthens equity). Pitfall: Using reserves for known losses.

16. Can Gross Loss Occur? Give An Example.

Yes, when COGS exceeds Net Sales, e.g., due to falling prices or high costs.

Gross Loss = COGS – Net Sales. Transfer: Trading A/c Dr. To Gross Loss A/c.

Example: Sales ₹80,000, COGS ₹1,00,000 (high purchases) → Gross Loss ₹20,000.

Causes: Obsolescence, discounts. Still, prepare P&L for the net result.

Pitfall: Assuming always profit.

17. Prepaid Expenses Appear In Trial Balance. How Will You Treat Them?

Deduct from the expense in P&L and show as Current Asset in Balance Sheet.

Prepaid is payment for future periods. If in Trial Balance (debit), it’s the prepaid amount. Example: Insurance ₹12,000 in TB, ₹4,000 prepaid → P&L debit ₹8,000, Asset ₹4,000.

Journal not needed as adjusted. Pitfall: Adding to expense.

18. Why Is Depreciation Charged Even When The Business Is Incurring Losses?

Depreciation allocates fixed asset cost over useful life (matching principle), independent of profits.It’s a non-cash expense for wear/tear.

Methods: Straight-line (fixed amount), WDV (on book value).

Example: Machine ₹1,00,000, 10% SLM → ₹10,000 yearly, even in loss. Enhances true profit reporting.

Pitfall: Skipping in losses; violates accrual.

19. What Is The Treatment Of “Dividend Received” In Final Accounts?

Credited to P&L as “Other Income” if from investments.

Non-operating income.

Journal: Bank Dr. To Dividend Income; Dividend Income Dr. To P&L.

Example: ₹5,000 dividend → P&L credit. If interim, accrue if declared.

Pitfall: Adding to sales.

20. Where Do You Charge “Preliminary Expenses”?

Written off to P&L or shown as “Miscellaneous Expenditure” under Other Assets, amortized over 3-5 years.

Incorporation costs like legal fees. AS-26 requires write-off.

Journal: P&L Dr. To Preliminary Expenses.

Example: ₹50,000 over 5 years = ₹10,000 p.a.

Pitfall: Capitalizing fully.

21. How Is “Proposed Dividend” Shown In The Balance Sheet?

As Current Liability under “Other Current Liabilities” or Provisions.

Declared but unpaid.

Journal: P&L Appropriation Dr. To Proposed Dividend.

Example: ₹20,000 proposed → Liability. Paid next year.

Pitfall: Deducting from reserves directly.

22. Where is “Unclaimed Dividend” shown?

Under “Other Current Liabilities.”

Dividend declared but not claimed. After 7 years, to IEPF (India).

Journal: Bank Dr. To Unclaimed Dividend (when paid). Remains liability.

Example: ₹10,000 unclaimed → Liability. Pitfall: Writing back to profit prematurely.

Few related topics for your knowledge

- How To Prepare Year-End Adjustments In Accounting: Step-By-Step Tutorial

- Inventory Valuation Process In Accounting: Importance, Methods, & Examples

- Depreciation Entry In Accounting: Meaning, Examples, How To Calculate It/a>

- Chart Of Accounts In Tally Prime: A Definitive Guide For Beginners

- Learn From The Best Advanced Excel Courses Online

- Rectification Of Errors In Accounting: Key Types & Methods

23. What Is “Deferred Revenue Expenditure”? Give Two Examples.

Heavy expenditure benefiting multiple years, written off gradually.

Examples: Heavy advertising, R&D costs.

Not capital but deferred.

Journal: Deferred Exp. Dr. To Bank; annual: P&L Dr. To Deferred Exp.

Example: ₹1,00,000 ad campaign over 5 years = ₹20,000 p.a. Pitfall: Full write-off in one year.

24. How Do You Treat “Fictitious Assets”?

Shown under “Other Non-Current Assets,” amortized to P&L.

No real value, e.g., preliminary expenses, debit P&L balance. Gradually eliminated. Example: Accumulated losses ₹50,000 → Amortize. Pitfall: Treating as real assets.

25. Difference between Outstanding Expenses And Prepaid Expenses.

There are several points of differences between Outstanding expenses and prepaid expenses. Some of the key facts to know about it are as follows:-

| Basis Of Difference | Outstanding Expense | Prepaid Expense |

|---|---|---|

| Meaning | Expense incurred but not yet paid by the end of the accounting period | Expense paid in advance but not yet incurred or consumed by the end of the period |

| Nature | Expense belongs to current year but payment is pending | Payment made in current year but expense belongs to next year |

| Example | Salary payable, Rent outstanding, Interest payable, Electricity bill due | Prepaid insurance, Prepaid rent, Advance salary, Insurance paid in advance |

| Type | Liability (Current Liability) | Asset (Current Asset) |

| Effect on Profit & Loss A/c | Added to the concerned expense (increases expense) | Deducted from the concerned expense (decreases expense) |

| Effect on Balance Sheet | Shown on Liabilities side as “Outstanding [Expense]” | Shown on Assets side as “Prepaid [Expense]” or “Advance [Expense]” |

| Journal Entry (at year-end) | Concerned Expense A/c Dr.

To Outstanding Expense A/c |

Prepaid Expense A/c Dr.

To Concerned Expense A/c |

| Adjustment Entry Example | Salary paid ₹50,000 + Outstanding ₹5,000 → Total Salary in P&L = ₹55,000 | Rent paid ₹60,000 out of which ₹10,000 is prepaid → Rent in P&L = ₹50,000 |

| Impact on Net Profit | Decreases profit (higher expense) | Increases profit (lower expense in current year) |

| Accrual vs Cash Basis | Reflects accrual concept (expense recognized when incurred) | Reflects Matching & Accrual Concept (expense matched with benefit period. ) |

26. Why is “Drawings” Deducted From Capital In The Balance Sheet?

Drawings are owner’s withdrawals, reducing equity. Personal use of business funds.

Journal: Drawings Dr. To Cash. Balance Sheet: Capital – Drawings + Net Profit.

Example: Capital ₹2,00,000, Drawings ₹30,000 → Net ₹1,70,000. Pitfall: Treating as an expense.

27. What Is “Contingent Liability”? Give examples.

Possible obligation from past events, depending on future. Not recorded but footnoted. If probable, provide. Example: Lawsuit ₹1,00,000 potential – disclose.

Pitfall: Recording as actual liability.

Examples: Pending lawsuits, discounted bills.

28. Where Is The “Share Forfeiture Account” Shown After Reissue Of Shares?

Transferred to Capital Reserve under Reserves & Surplus. Forfeited shares’ paid-up amount. On reissue: Bank Dr., Forfeited Shares Dr. To Share Capital; excess to Capital Reserve.

Example: Forfeited ₹5,000, reissued at premium → Reserve.

Pitfall: Crediting to P&L.

29. How Is “Interest On Capital” Treated In Final Accounts Of A Company?

Not allowed; Companies Act prohibits unless articles permit for specific cases.

Equity holders get dividends, not interest. In partnerships, yes.

Example: No entry for companies.

Pitfall: Allowing like partnerships.

30. A machine purchased on 1st Oct 2024 for ₹2,00,000. Rate of depreciation 10% p.a. on straight-line basis. What is the depreciation for the year ending 31st March 2025?

₹10,000 (pro-rated for 6 months).

SLM: Annual Dep. = Cost × Rate. Pro-rate: ₹2,00,000 × 10% × 6/12 = ₹10,000.

Journal: Dep. Exp. Dr. To Accum. Dep. Balance Sheet: Machine ₹2,00,000 – ₹10,000.

Pitfall: Full-year charge.

Bonus Questions For Final Accounts

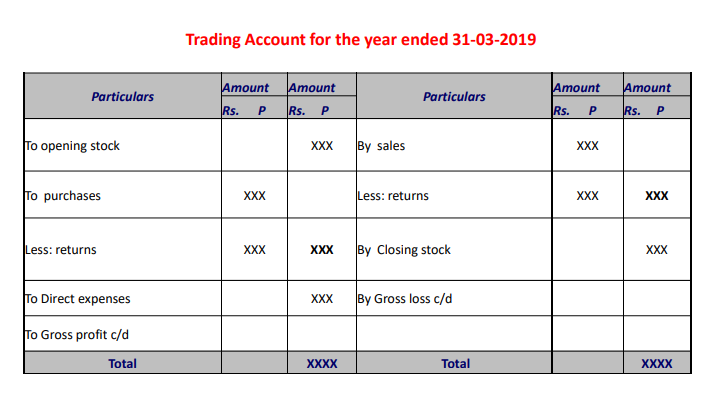

What Is The Format Of Trading A/c?

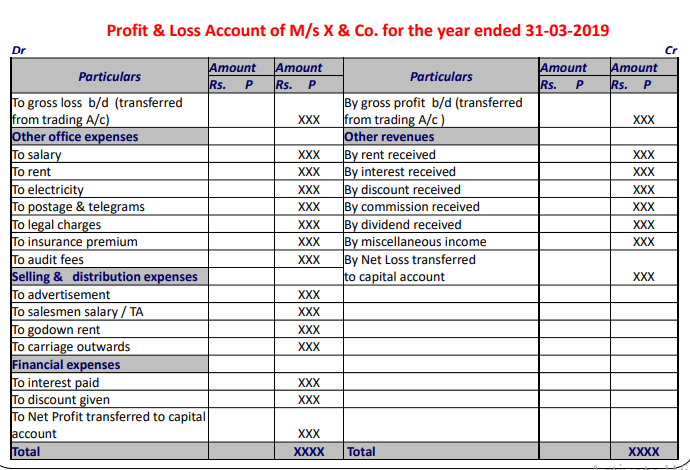

What Is The Format Of Profit & Loss Account?

What Is The Format Of Balance Sheets?

Final Takeaway

Hence, these are some of the crucial Final Accounts questions that you must be well aware off. You cannot just make your choices in the dark. Here, proper planning holds the key. Try to develop a better plan that can make things work perfectly well in your way.

You can share your opinion in our comment box. This will assist us in making the correct decision from our end without any issue.