.jpg)

50 Important Depreciation Questions & Answers For Interview

Depreciation is a fundamental concept in accounting and finance, representing the systematic allocation of a tangible fixed asset’s cost over its useful life. Depreciation questions are important for you to understand about the useful life of an asset. It reflects the gradual decline in an asset’s value due to wear and tear, obsolescence, usage, or time passage.

Understanding depreciation is crucial for interviews in roles like financial accounting, auditing, taxation, and management accounting, as it tests knowledge of the matching principle, financial statement impacts, and compliance with standards like IFRS (IAS 16) and GAAP.

Interview questions on depreciation typically cover definitions, causes, methods (e.g., Straight-Line, Diminishing Balance, Units of Production), journal entries, tax vs. book differences, impairment, revaluation, and practical scenarios like asset disposal or life revisions. Mastery demonstrates analytical skills, as depreciation affects profitability, cash flows, balance sheet accuracy, and tax planning.

Preparing these questions helps articulate how depreciation ensures true and fair financial reporting while providing tax shields. Strong answers, backed by examples and formulas, can set you apart in competitive interviews.

Table of Contents

- List Of Important Depreciation Questions & Answers For Interview

- 1. What Is Depreciation?

- 2. What Are The Main Causes Of Depreciation?

- 3. Why Is Depreciation Chargeable Even If The Asset Is Not In Use?

- 4. Is Depreciation A Cash Expense?

- 5. What Is The Purpose Of Charging Depreciation?

- 6. Name The Common Methods Of Depreciation?

- 7. Explain The Straightline Method Of Calculation For Depreciation?

- 8. What Are The Advantages Of The Straight Line Method?

- 9. What Are The Disadvantages Of A Straightline Method?

- 10. Explain Diminishing Balance Method?

- 11. Why Is The Diminishing Balance Method Called The Accelerated Depreciation?

- 12. What Is The Formula Of Double Declining Balance Method?

- 13. When Is The Units Of Production Method Most Suitable?

- 14. Explain The Units Of Production Method?

- 15. What Is The Salvage Value Or Scrap Value?

- 16. What Is The Useful Life Of An Asset?

- 17. What Is Accumulated Depreciation?

- 18. How Is Depreciation Recorded In Journal Entry

- 19. Where Does Depreciation Appear In Financial Statements?

- 20. Does Depreciation Affect Cash Flow?

- 21. How Does A Rs10 Increase In Depreciation Affect The Three Financial Statements (Assume 30% Tax Rate)?

- 22. Why Is Land Not Depreciated?

- 23. What Is The Difference Between Depreciation & Amortization?

- 24. What Is Depletion?

- 25. Can Depreciation Methods Be Changed?

- 26. What Is Impairment Of Assets??

- 27. What Is A Fully Depreciated Asset?

- 28. How Do You Account For Disposal Of A Depreciated Asset?

- 29. If An Asset Is Sold For More Than Book Value Then What Is It?

- 30. How Does Impairment Differ From Depreciation?

- 31. What Is Provision For Depreciation?

- 32. Why Provide Depreciation On Assets?

- 33. Is Depreciation Mandatory For Accounting Standards?

- 34. What Are Revaluation Models For Assets?

- 35. Does Revaluation Affects Depreciation

- 36. What Is Component Depreciation?

- 37. When Is Component Depreciation Required?

- 38. What Is Bonus Depreciation?

- 39. Why Tax Depreciation Differs From Book Depreciation?

- 40. What Is Matching Principal In Relation To Depreciation?

- 41. How Do You Calculate Depreciation If An Asset Purchased In Mid Year?

- 42. What Is The Sum Of Years Digit Method?

- 43. Why Use Accelerated Depreciation Method?

- 44. What Happens To Depreciation If Useful Life Is Revised?

- 45. Can Depreciation Be Negative?<

- 46. How Is Depreciation Treated In Cash Flow Statement?

- 47. What Is A Fixed Asset Register?

- 48. Why Do You Need To Reconcile Fixed Assets Periodically?

- 49. What Is Capitalized Interest In Relation To Assets?

- 50. Explain The Cost Principal In Asset Depreciation

- Final Takeaway

List Of Important Depreciation Questions & Answers For Interview

There are several important depreciation questions and answers for the interview that you must be well aware of. Some of the key factors that you should be well aware off from your end are as follows:-

1. What Is Depreciation?

Depreciation is the systematic and rational allocation of the depreciable cost (original cost minus salvage value) of a tangible fixed asset over its estimated useful life. It reflects the asset’s consumption due to wear and tear, obsolescence, or usage.

Example: A machine costing Rs 100,000 with a 10-year life and Rs 10,000 salvage value depreciates Rs 9,000 annually under straight-line method.

It follows the matching principle: expense the asset cost against revenues it helps generate. It is one of the crucial depreciation questions to remember from your end.

2. What Are The Main Causes Of Depreciation?

- Physical deterioration: Wear and tear from usage (e.g., machinery rusting).

- Obsolescence: Asset becomes outdated due to technology/market changes (e.g., old computers).

- Effluxion of time: Passage of time for time-bound assets (e.g., leases, patents).

- Depletion: Exhaustion of natural resources (separate but related concept). Even idle assets may depreciate due to time-based factors.

Opt for a NAAC A + AICTE approved BBA Degree1-year paid internship + 10 Simulation Software + 4 Certifications. 90% Practical Learning. |

|

| Bachelor in Accounting and Finance |

3. Why Is Depreciation Chargeable Even If The Asset Is Not In Use?

Assets like leases or patents lose value over time regardless of usage (effluxion of time). Obsolescence can occur due to external advancements. Accounting standards (e.g., IAS 16) require allocation over useful life, not just usage.

4. Is Depreciation A Cash Expense?

No. It’s a non-cash expense—it reduces reported profit but no cash outflows. Funds “saved” (not distributed as dividends) can be used for replacement. Depreciation questions can help your business to grow at a faster pace.

Impact: Reduces taxable income (tax shield), improving cash flow indirectly.

5. What Is The Purpose Of Charging Depreciation?

It is one of the most crucial Depreciation questions that you must go through from your end.

- Match asset cost with revenues (matching principle).

- Show true asset value on the balance sheet.

- Comply with prudence (not overstate profits/assets).

- Retain cash for future replacement.

- Tax benefits.

6. Name The Common Methods Of Depreciation?

- Straight-Line Method (SLM).

- Written Down Value/Diminishing Balance Method.

- Units of Production Method.

- Sum-of-the-Years’-Digits (SYD).

- Double Declining Balance (DDB).

- Annuity Method, Sinking Fund Method (less common).

7. Explain The Straightline Method Of Calculation For Depreciation?

Formula: Annual Depreciation = (Cost – Salvage Value) / Useful Life.

Example: Asset Rs 100,000, salvage Rs 10,000, life 10 years → Rs 9,000/year.

Journal: Dr. Depreciation Expense Rs 9,000; Cr. Accumulated Depreciation Rs 9,000.

Even charge each year; simple and widely used.

8. What Are The Advantages Of The Straight Line Method?

- Easy calculation and understanding.

- Uniform expense allocation.

- Suitable for assets with constant utility (e.g., buildings).

- Accepted for financial reporting.

9. What Are The Disadvantages Of A Straightline Method?

- Ignores higher efficiency in early years or increasing repair costs later.

- Overstates asset productivity in later years.

10. Explain Diminishing Balance Method?

The Diminishing Balance Method (also known as the Declining Balance Method, Reducing Balance Method, or Written Down Value Method) is an accelerated depreciation technique in accounting. It allocates a higher amount of depreciation expense in the early years of an asset’s useful life and progressively lower amounts in later years. This reflects the reality that many assets (like machinery, vehicles, or technology) lose value more rapidly initially due to higher usage, obsolescence, or wear and tear.

Formula

The standard formula for depreciation expense each year is:

Depreciation Expense = Book Value at the Beginning of the Year × Depreciation Rate

Where:

- Book Value = Original Cost – Accumulated Depreciation (from previous years)

- Depreciation Rate = A fixed percentage (e.g., 20% or 30%)

A common variant is the Double Declining Balance (DDB) Method, where the rate is twice the straight-line rate (e.g., if straight-line is 20% over 5 years, DDB uses 40%).

To calculate the rate when salvage value and useful life are in knowledge:

Rate (r) = 1 – \sqrt[n]{(Salvage Value / Original Cost)}

(where n = useful life in years).

Example:-

Assume an asset costs Rs 10,000 with no salvage value and a 40% depreciation rate (e.g., double declining for a 5-year life).

| Year | Beginning Book Value | Depreciation Expense (40%) | Accumulated Depreciation | Ending Book Value |

|---|---|---|---|---|

| 1 | Rs 10,000 | Rs 4,000 | Rs 4,000 | Rs 6,000 |

| 2 | Rs 6,000 | Rs 2,400 | Rs 6,400 | Rs 3,600 |

| 3 | Rs 3,600 | Rs 1,440 | Rs 7,840 | Rs 2,160 |

| 4 | Rs 2,160 | Rs 864 | Rs 8,704 | Rs 1,296 |

| 5 | Rs 1,296 | Rs 518 | Rs 9,222 | Rs 778 |

11. Why Is The Diminishing Balance Method Called The Accelerated Depreciation?

The Diminishing Balance Method (also known as the Declining Balance Method or Reducing Balance Method) is called an accelerated depreciation method because it allocates a larger portion of an asset’s cost as depreciation expense in the early years of its useful life, with the expense decreasing over time.

Why Is It Accelerated?

- In contrast to the straight-line method, which spreads depreciation evenly across the asset’s life (e.g., the same amount each year), the diminishing balance method applies a fixed percentage rate to the asset’s depreciating book value (original cost minus accumulated depreciation) at the beginning of each period.

- This results in higher depreciation charges initially (when the book value is highest) and progressively lower charges later, effectively “accelerating” the recognition of the asset’s cost comparing to even allocation.

- Common variants, like the double-declining balance (using twice the straight-line rate), amplify this effect even more.

Simple Example

Assume an asset costs Rs 10,000, has no salvage value, a 5-year useful life, and uses a 40% diminishing balance rate:

- Year 1: Depreciation = 40% × Rs 10,000 = Rs 4,000 (book value ends at Rs 6,000)

- 2nd Year: 40% × Rs 6,000 = Rs 2,400 (book value ends at Rs 3,600)

- Year 3: 40% × Rs 3,600 = Rs 1,440

- And so on—decreasing each year.

Under straight-line, it would be Rs 2,000 evenly each year. The diminishing method “front-loads” the expense, making it accelerated.

This approach better matches the actual pattern of value loss for assets that obsolesce quickly (e.g., technology or vehicles), where productivity and value decline faster early on. It also provides tax benefits by reducing taxable income more in initial years.

12. What Is The Formula Of Double Declining Balance Method?

The Double Declining Balance Method is an accelerated depreciation technique that applies twice the straight-line depreciation rate to the asset’s book value at the beginning of each period.

Key Steps and Formula

- Calculate the straight-line depreciation rate:

Double it to get the DDB rate:

Depreciation expense for each year:

![]()

Where:

Book value = Original cost − Accumulated depreciation up to the prior year

- Note: Unlike the general diminishing balance method, DDB typically does not consider salvage value in the rate calculation. However, depreciation stops when the book value reaches the estimated salvage (residual) value—meaning you don’t depreciate below salvage.

Example

Asset cost: Rs 10,000

Salvage value: Rs 1,000

Useful life: 5 years

- Straight-line rate = 1/5 = 20%

- DDB rate = 2 × 20% = 40%

The Double Declining Balance Method is an accelerated depreciation technique that applies twice the straight-line depreciation rate to the asset’s book value at the beginning of each period.

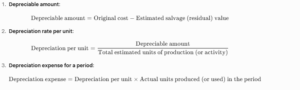

13. When Is The Units Of Production Method Most Suitable?

The Units of Production Method (also known as the Units of Activity or Output Method) is a depreciation technique that allocates an asset’s cost based on its actual usage or output rather than time. It is most suitable in the following situations:

1. When asset wear and tear is more closely related to usage than to the passage of time

- The economic benefit and value loss of the asset depend primarily on how much it is used (e.g., miles driven, hours operated, units manufactured) rather than aging uniformly over years.

- This makes depreciation expense better match the revenue generated by the asset in each period (aligning with the matching principle in accounting).

2. Common asset types and industries

- Vehicles (e.g., trucks, delivery vans, taxis) – depreciated based on kilometers or miles driven.

- Machinery and equipment in manufacturing – based on machine hours or number of units produced.

- Natural resource extraction (e.g., mines, oil wells, timber tracts) – based on tons extracted, barrels produced, or cubic meters removed (often called depletion in this context, but uses the same method).

- Aircraft – based on flight hours.

- Printing presses – based on number of impressions or pages printed.

- Construction equipment (e.g., bulldozers, excavators) – based on operating hours.

3. When usage varies significantly from year to year

- If an asset is in heavy use for some years and lightly in others, this method prevents over- or under-depreciating in low/high-usage periods in comparison to straight-line (which assumes constant usage).

Formula:-

![]()

14. Explain The Units Of Production Method?

The Units of Production Method (also called the Units of Activity Method or Output Method) is a depreciation technique that allocates the cost of a tangible asset based on its actual usage, activity, or output rather than the passage of time. It is also one of the crucial depreciation questions to remember before the interview.

It is particularly useful because it aligns depreciation expense with the actual consumption of the asset’s economic benefits, adhering closely to the matching principle in accounting (expenses matched to the revenues they help generate).

Key Features

- Activity-based: Depreciation is proportional to usage in each period.

- Variable expense: Higher usage → higher depreciation; lower usage → lower depreciation.

- Not time-based: Unlike straight-line or declining balance methods, it ignores calendar time.

Formula:-

15. What Is The Salvage Value Or Scrap Value?

Salvage Value (also known as Scrap Value, Residual Value, or Disposal Value) is the estimated amount that an asset is expected to be worth at the end of its useful life to the business. It represents the net amount the company expects to recover when the asset is disposed of—either by selling it, trading it in, or scrapping it for parts/materials—after deducting any disposal costs.

Key Points

- It is an estimate made at the time of asset acquisition.

- It is used in depreciation calculations to determine the depreciable amount (the portion of the cost that will be expensed over the asset’s life).

- Salvage value can be zero if the asset is expected to have no recoverable value at the end (common for many assets), or it can be positive (e.g., vehicles or machinery that retain resale value).

Formula in Depreciation

Depreciation methods (straight-line, diminishing balance, units of production, etc.) allocate this depreciable amount over the asset’s useful life. The book value at the end of the useful life should equal the salvage value.

16. What Is The Useful Life Of An Asset?

Useful Life (also called Service Life or Economic Life) is the estimated period during which a tangible fixed asset is expected to be usable and productive for the business that owns it. It represents the length of time the asset is anticipated to contribute to generating revenue or providing economic benefits before it becomes obsolete, worn out, or uneconomical to continue using.

Key Characteristics

- It is an estimate made by management at the time the asset is in acquisition (or when depreciation begins).

- Useful life is expressed in time units (e.g., years, months) or activity units (e.g., machine hours, miles driven, units produced), depending on the depreciation method.

- It is specific to the company using the asset—not necessarily the physical life. An asset might still function physically but be considered at the end of its useful life due to obsolescence, inefficiency, or changes in technology/business needs.

Factors Considered in Estimating Useful Life

- Physical deterioration: Wear and tear from normal use. Depreciation questions are useful for your life.

- Obsolescence: Technological advancements making the asset outdated (e.g., older computers).

- Legal or regulatory limits: Licenses, leases, or contracts that restrict usage period.

- Company policy: Planned replacement cycles or usage intensity.

- Historical experience: Data from similar assets previously used by the company.

- Manufacturer guidelines: Expected durability or warranty periods.

17. What Is Accumulated Depreciation?

Accumulated Depreciation is a contra-asset account on the balance sheet that represents the total amount of depreciation expense that has been recorded (or “accumulated”) for a tangible fixed asset (or group of assets) from the time it was acquired and placed in service up to the current reporting date.

Key Features

- It is not a cash account—it does not represent money set aside; it’s simply a cumulative record of the portion of the asset’s cost that has been allocated as an expense over time.

- It has a credit balance (normal for contra-assets).

- Accumulated Depreciation increases each period with the depreciation expense recorded for that period.

- It is subtracted from the asset’s original cost to arrive at the asset’s net book value (or carrying amount).

| Asset Description | Cost | Accumulated Depreciation | Net Book Value |

|---|---|---|---|

| Machinery | Rs 100000 | Rs 40000 | Rs 60000 |

| Vehicles | Rs 50000 | Rs 20000 | Rs 30000 |

18. How Is Depreciation Recorded In Journal Entry?

Depreciation is in periodic records (monthly, quarterly, or annually) to allocate the cost of a tangible fixed asset over its useful life. It is a non-cash expense, so it reduces net income but does not involve cash outflow.

| Date | Account Titles & Explanation | Debit | Credit |

|---|---|---|---|

| Date | Depreciation Expense | XXX | |

| Accumulated Depreciation | XXX |

19. Where Does Depreciation Appear In Financial Statements?

Depreciation impacts three main financial statements (Income Statement, Balance Sheet, and Cash Flow Statement), but it appears directly in only two. Here’s a clear breakdown:

1. Income Statement (Statement of Profit or Loss)

- Depreciation Expense is shown as an operating expense (non-cash).

- Location:

- Often listed separately as “Depreciation and Amortization” under operating expenses.

- Sometimes grouped under “Administrative Expenses” or “Selling, General & Administrative Expenses” (SG&A).

- It reduces operating profit (EBIT) and ultimately net profit.

2. Balance Sheet (Statement of Financial Position)

- Depreciation does not appear as a separate line item by name.

- Instead, its cumulative effect is shown as Accumulated Depreciation (a contra-asset account).

- Location:

- Under Non-Current Assets (or Property, Plant & Equipment section).

- Subtracted from the original cost of fixed assets to show Net Book Value (Carrying Amount).

- Cash Flow Statement

- Depreciation does not appear as a cash outflow (since it’s non-cash).

- It is added back to net profit in the operating activities section (indirect method).

- Reason: Net profit has already been reduced by depreciation expense, so we add it back to arrive at cash generated from operations.

Few related topics for your knowledge

- How To Prepare Year-End Adjustments In Accounting: Step-By-Step Tutorial

- Inventory Valuation Process In Accounting: Importance, Methods, & Examples

- Depreciation Entry In Accounting: Meaning, Examples, How To Calculate It/a>

- Chart Of Accounts In Tally Prime: A Definitive Guide For Beginners

- Learn From The Best Advanced Excel Courses Online

- 30 Essential Final Accounts Questions & Answers

20. Does Depreciation Affect Cash Flow?

Depreciation is a non-cash expense. It reduces reported net profit on the income statement but does not involve any actual outflow of cash. No money leaves the company’s bank account when depreciation is recorded.

Indirectly: Yes (through taxes and cash flow statements).

While depreciation itself doesn’t use cash, it has important effects on cash flow:

1. Positive Impact on Operating Cash Flow (via Tax Shield)

- Depreciation reduces taxable income (profit before tax).

- Lower taxable income → lower income taxes paid → more cash retained by the company.

- This is called the depreciation tax shield.

Example:-

- Profit before depreciation and tax: Rs 100,000

- Depreciation expense: Rs 20,000

- Taxable income: Rs 80,000

- Tax rate: 30%

- Tax paid: Rs 24,000 (instead of Rs 30,000 without depreciation)

- Cash saved due to depreciation: Rs 6,000

2. How It Appears in the Cash Flow Statement

Using the indirect method (most common):

- Net profit is lower because of depreciation.

- But we add back the full depreciation amount because it didn’t use cash.

- Result: Operating cash flow is higher than net profit, reflecting that depreciation preserved cash.

21. How Does A Rs10 Increase In Depreciation Affect The Three Financial Statements (Assume 30% Tax Rate)?

An increase of Rs10 in depreciation expense is a non-cash expense. It reduces profit but does not involve cash outflow. The effects flow through the financial statements as follows (assuming a corporate tax rate of 30%):

1. Income Statement (Profit & Loss Statement)

- Depreciation Expense increases by Rs10.

- This reduces Profit Before Tax by Rs10.

- Tax Expense decreases by 30% × Rs 10 = Rs 3 (tax shield).

- Net Profit decreases by Rs 10 − Rs 3 = Rs 7.

2. Balance Sheet

- Assets side:

- Accumulated Depreciation increases by Rs10 → Net Fixed Assets decrease by Rs10.

- Liabilities & Equity side:

- Retained Earnings decrease by Rs7 (due to lower Net Profit).

- Current Tax Liability (or Deferred Tax, depending on timing) decreases by Rs3 (lower taxes payable).

- The balance sheet remains balanced: Total decrease on left = Rs10; total decrease on right = Rs7 + Rs3 = Rs10.

3. Cash Flow Statement (Indirect Method)

- Starts with Net Profit (−Rs7 from above).

- Add back Depreciation Expense +Rs10 (non-cash).

- Subtract lower Tax Paid −Rs3 (actual cash savings on taxes).

- Net effect on Cash Flow from Operating Activities: +Rs10 − Rs3 = +Rs3.

22. Why Is Land Not Depreciated?

Land is not depreciated in accounting because it is considered to have an unlimited useful life and does not wear out, become obsolete, or get “used up” through normal business operations.

Key Reasons

- Indefinite (Unlimited) Useful Life

- Unlike other fixed assets (e.g., buildings, machinery, vehicles), land does not deteriorate over time due to usage, weather, or passage of time.

- Its economic usefulness to the business is assumed to last indefinitely, as long as the company owns it.

- Accounting standards (e.g., IAS 16, US GAAP) require depreciation only for assets with a finite (limited) useful life.

- No Systematic Allocation Needed

- Depreciation is the systematic allocation of an asset’s cost over its useful life to match expenses with revenues (matching principle).

- Since land’s value is not consumed over time, there is no cost to allocate periodically.

- Potential for Appreciation

- Land often increases in value over time due to location, development, inflation, or market demand.

- Depreciating it would understate its value on the balance sheet, which contradicts the historical cost principle (though revaluation is allowed in some standards like IFRS).

23. What Is The Difference Between Depreciation & Amortization?

Depreciation and Amortization are both non-cash expenses used to systematically allocate the cost of an asset over its useful life, following the matching principle (matching expense to the periods benefited). However, they apply to different types of assets.

| Aspect | Depreciation | Amortization |

| Types Of Asset | Tangible (physical) fixed assets

e.g., buildings, machinery, vehicles, furniture, equipment |

Intangible (non-physical) assets

e.g., patents, copyrights, trademarks, goodwill, software, licenses, franchises |

| Nature Of Asset | Assets that physically exist and can wear out or deteriorate | Assets without physical substance, often acquired through purchase or legal rights |

| Useful Life | Finite due to wear/tear, obsolescence, or usage | Finite (for most intangibles) or indefinite (e.g., some trademarks) |

| Methods Commonly Used | – Straight-line

– Diminishing balance (accelerated) – Units of production – Double-declining balance |

Almost always straight-line (even allocation over useful life) |

| Salvage Value | Often considered (residual value at end of life) | Usually zero (intangibles rarely have resale value) |

| Accounting Standards Reference | IAS 16 / AS 10 (Property, Plant & Equipment) | IAS 38 / AS 26 (Intangible Assets) |

| Examples | – Depreciating a delivery truck over 5 years

– Factory machine over 10 years |

– Amortizing a patent over its 20-year legal life

– Goodwill over its estimated useful life (or impairment-tested if indefinite) |

24. What Is Depletion?

Depletion is the systematic allocation of the cost of natural resources (also called wasting assets) over the period they are extracted or consumed. It is the equivalent of depreciation but specifically applied to exhaustible natural resources such as minerals, oil, gas, timber, coal, gravel, or quarries.

The purpose of depletion is to match the cost of acquiring and developing the resource with the revenue generated from selling the extracted material, adhering to the matching principle in accounting.

Key Features

- Applies to non-renewable natural resources that are physically removed and sold.

- The resource base is finite, so the cost is allocated based on the amount extracted relative to the total estimated reserves.

- It is a non-cash expense, similar to depreciation.

Assets Typically Subject to Depletion

- Oil and gas reserves

- Mineral deposits (e.g., gold, copper, iron ore)

- Timber tracts (forests)

- Coal mines

- Stone quarries

- Gravel pits

25. Can Depreciation Methods Be Changed?

Yes, depreciation methods can be changed, but it is not done arbitrarily. Accounting standards (e.g., IAS 16 under IFRS, Ind AS 10 in India, or US GAAP) allow changes only under specific conditions to ensure financial statements remain accurate and relevant.

When Can the Method Be Changed?

- Change in Circumstances: If the new method better reflects the pattern of consumption of the asset’s economic benefits.

- Examples:

- Switching from straight-line to diminishing balance if an asset is now expected to lose value faster (e.g., due to increased usage or technological obsolescence).

- From diminishing balance to straight-line for assets that wear out more evenly over time.

- Examples:

- Not Allowed: Changes purely for tax benefits, profit manipulation, or cosmetic reasons.

How Is the Change Applied?

- Prospective Application Only: The change is applied from the date of change onward.

- Do not restate prior years’ financial statements.

- Recalculate remaining depreciation based on the current book value (cost minus accumulated depreciation up to the change date) and the remaining useful life.

- Disclosure Required: In financial statement notes, explain:

- Reason for the change.

- Nature of the change.

- Impact on current and future periods (e.g., increase/decrease in depreciation expense).

26. What Is Impairment Of Assets?

Impairment of Assets occurs when the carrying amount (book value) of an asset on the balance sheet exceeds its recoverable amount. In simple terms, it means the asset is overvalued because its future economic benefits have permanently declined, and the company must write down its value to reflect this loss.

Impairment ensures that assets are not carried at more than what they can realistically recover through use or sale, adhering to the prudence (conservatism) principle in accounting.

- Carrying Amount: Original cost minus accumulated depreciation/amortization and any previous impairments.

- Recoverable Amount: The higher of:

- Fair Value Less Costs of Disposal (what you could sell it for, net of selling costs).

- Value in Use (present value of future cash flows expected from continuing to use the asset).

If Carrying Amount > Recoverable Amount → Impairment Loss.

When Does Impairment Occur?

Impairment is tested when there are indicators of impairment (internal or external triggers):

| External Indicators | Internal Indicators |

|---|---|

| Significant decline in market value | Physical damage to the asset |

| Adverse changes in technology/market | Asset underperforming (lower output) |

| Increases in interest rates | Changes in how the asset is used |

| Market capitalization < net assets | Evidence of obsolescence |

| Economic/legal environment changes | Plans To Dispose/ Restructure |

27. What Is A Fully Depreciated Asset?

A fully depreciated asset is a tangible fixed asset whose entire depreciable amount has been allocated as depreciation expense over its useful life. At this point:

- The asset’s net book value (carrying amount) equals its estimated salvage value (or zero if no salvage was assumed).

- Accumulated depreciation equals the original cost minus salvage value.

The asset has been “fully expensed” for accounting purposes, but it may still be physically in use and providing economic benefits.

Key Characteristics

- Depreciation stops: No further depreciation expense is recorded, even if the asset continues to be used.

- Still on the books: The asset remains on the balance sheet at its residual (salvage) value until it is retired, sold, or disposed.

- Not necessarily worthless: The asset might still be functional and valuable in operations (or even have a higher market value than book value).

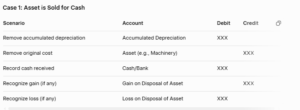

28. How Do You Account For Disposal Of A Depreciated Asset?

The disposal of a depreciated asset occurs when a tangible fixed asset is sold, scrapped, traded in, or otherwise retired from use. Accounting for disposal involves removing the asset’s cost and its accumulated depreciation from the books and recognizing any gain or loss based on the proceeds received compared to the asset’s net book value (carrying amount) at the date of disposal.

Steps in Accounting for Disposal

- Update depreciation up to the date of disposal: Record depreciation expense for the portion of the year the asset was used before disposal (prorated if necessary).

- Calculate the net book value (NBV) at disposal:

![]()

3. Determine gain or loss on disposal:

4. Record the journal entry to remove the asset and recognize the gain/loss.

<h3id=”29″>29. If An Asset Is Sold For More Than Book Value Then What Is It?

When a depreciated fixed asset (e.g., machinery, vehicle, building) is sold for more than its net book value (also called carrying amount), it results in a gain on disposal (or profit on sale of the asset).

Key Terms Recap

- Net Book Value (NBV) = Original cost − Accumulated depreciation (up to date of sale).

- Proceeds = Amount received from the sale (cash or equivalent).

If Proceeds > NBV → Gain on Disposal.

This gain represents the excess recovery over the asset’s remaining undepreciated cost.

Accounting Treatment

The gain is recognized in the Income Statement as:

- Other Income or

- Gain on Disposal/Sale of Fixed Asset (often shown separately for transparency).

It is not part of operating profit but increases overall net profit.

Journal Entry:-

| Date | Account | Debit | Credit |

|---|---|---|---|

| Cash Account | 40000 | ||

| Accumulated Depreciation | 70000 | ||

| Machinery | 100000 | ||

| Gain On Disposal Of Asset | 10000 |

30. How Does Impairment Differ From Depreciation?

Both impairment and depreciation reduce the carrying amount (book value) of an asset on the balance sheet and recognize a expense in the income statement. However, they serve different purposes, occur under different circumstances, and are applied differently.

| Aspect | Depreciation | Impairment |

|---|---|---|

| Purpose | Systematic allocation of an asset’s cost over its useful life (matching principle: match cost to periods benefited). | One-time (or periodic) write-down to reflect a permanent decline in the asset’s recoverable value below its carrying amount. |

| Nature | Planned and predictable – ongoing, regular process based on estimates of useful life and usage. | Unplanned and event-driven – triggered by specific indicators of value loss (e.g., damage, obsolescence, market decline). |

| Timing | Periodic – recorded every accounting period (monthly, quarterly, annually) throughout the asset’s useful life. | As needed – tested when impairment indicators exist; mandatory annually for goodwill and indefinite-life intangibles. |

| Calculation Basis | Based on original cost, useful life, salvage value, and chosen method (straight-line, diminishing balance, units of production). | Based on comparison of carrying amount vs. recoverable amount (higher of fair value less costs to sell or value in use). |

| Amount | Gradual and spread over time (e.g., fixed annual amount in straight-line). | Sudden and potentially large one-time loss (difference between carrying amount and recoverable amount). |

| Reversibility | Not reversible – accumulated depreciation cannot be reversed (except on disposal). | Reversible for most assets (except goodwill) if conditions improve later – reversal credited to income (up to original cost). |

| Impact On Future Depreciation | Continues based on original estimates (or revised prospectively). | Reduces carrying amount → future depreciation is calculated on the new lower book value. |

| Assets Affected | Primarily tangible assets with finite lives (PPE); also some intangibles. Land not depreciated. | Tangible assets, finite/intangible assets, goodwill, and cash-generating units (CGUs). |

31. What Is Provision For Depreciation?

Provision for Depreciation (also commonly called Accumulated Depreciation in modern accounting terminology) is the cumulative amount of depreciation expense that has been charged against a fixed asset (or group of assets) from the date of acquisition up to the current reporting date.

It is a contra-asset account (negative asset) on the balance sheet that reduces the original cost of the asset to arrive at its net book value (carrying amount).

Purpose

- To show how much of the asset’s cost has been “used up” or allocated as an expense over time.

- Ensures the balance sheet reflects the remaining undepreciated value of the asset.

- Avoids directly reducing the historical cost of the asset (which remains unchanged for record-keeping).

Key Features

- Credit balance account (increases with credits from depreciation entries).

- Non-cash: Represents past depreciation expenses, not a cash reserve or fund.

- Presented as a deduction from the related asset class on the balance sheet.

32. Why Provide Depreciation On Assets?

Depreciation is the systematic allocation of the cost of a tangible fixed asset (e.g., machinery, vehicles, buildings) over its useful life. Providing (recording) depreciation is essential in accounting for several key reasons:

1. Matching Principle (Accurate Profit Measurement)

- Businesses incur the cost of an asset upfront, but the asset provides economic benefits (helps generate revenue) over multiple years.

- Depreciation spreads this cost across the periods benefited, matching expenses with related revenues.

- Without depreciation, profits would be overstated in early years (low expenses) and understated later (when replacement costs hit).

2. True and Fair View of Financial Position

- Assets lose value over time due to wear and tear, obsolescence, or usage.

- Recording depreciation reduces the asset’s book value to reflect its remaining economic usefulness.

- This prevents overstatement of assets on the balance sheet and shows a realistic net worth.

3. Compliance with Accounting Standards

- Mandatory under major frameworks:

- IFRS/IAS 16: Property, Plant & Equipment must be depreciated.

- Ind AS 16 (India), US GAAP, etc., require systematic allocation.

- Failure to depreciate violates prudence and accrual concepts.

4. Tax Benefits (Tax Shield)

- Depreciation is a non-cash expense deductible for tax purposes in most jurisdictions.

- Reduces taxable income → lower taxes paid → improves cash flow.

- Governments encourage investment by allowing accelerated methods (e.g., double-declining balance).

5. Decision-Making and Performance Evaluation

- Helps management assess:

- True cost of using assets (e.g., cost per unit produced).

- When to replace assets (comparing book value vs. replacement cost).

- Operational efficiency across periods.

- Investors/analysts use depreciated figures for ratios like Return on Assets (ROA).

33. Is Depreciation Mandatory For Accounting Standards?

Yes, depreciation is mandatory under major accounting standards for most depreciable assets (tangible fixed assets with finite useful lives, such as machinery, buildings, vehicles, and equipment).

Why It’s Mandatory

- Depreciation systematically allocates the cost of an asset over its useful life, aligning with the matching principle (expenses matched to the revenues they help generate) and accrual basis of accounting.

- It ensures assets are not overstated on the balance sheet and profits are accurately reflected.

- Standards explicitly require it for assets with limited useful lives.

34. What Are Revaluation Models For Assets?

The revaluation model is an accounting method used for the subsequent measurement of certain non-current assets, primarily property, plant, and equipment (PPE) under International Financial Reporting Standards (IFRS), specifically IAS 16 Property, Plant and Equipment. It allows companies to carry these assets at their fair value (current market value) rather than historical cost.

Key Features

- After initial recognition at cost, the asset is carried at its revalued amount, which is fair value at the date of revaluation minus any succeeding accumulated depreciation as well as impairment losses.

- Revaluations must be performed regularly (e.g., annually for volatile assets like real estate, or every 3–5 years for stable ones) to ensure the carrying amount does not materially differ from fair value at the reporting date.

- The model must be applied consistently to an entire class of assets (e.g., all buildings or all machinery in the company).

- Fair value is typically determined by professional appraisers or market evidence.

Accounting Treatment For Revaluation Changes

- Upward revaluation (increase in value): Credited to other comprehensive income (OCI) and accumulated in equity as revaluation surplus (not through profit or loss, except to reverse a prior downward adjustment).

- Downward revaluation (decrease in value): Debited to profit or loss (expense), but first offset against any existing revaluation surplus for that asset.

- Depreciation is recalculated based on the new revalued amount.

35. Does Revaluation Affects Depreciation

Yes, under Indian Accounting Standards (Ind AS), revaluation of assets under the revaluation model (Ind AS 16 Property, Plant and Equipment) directly affects subsequent depreciation. Ind AS 16 is converged with IAS 16 (IFRS) and applies to companies following Ind AS in India (e.g., listed companies and large unlisted entities as per the Companies Act, 2013). For smaller companies using Indian GAAP (AS 10 Accounting for Fixed Assets and AS 6 Depreciation Accounting), the effect is similar but with some differences in treatment of surplus.

Key Provisions Under Ind AS 16

- Revaluation Model Overview: After initial recognition at cost, assets are carried at fair value at the revaluation date, less any subsequent accumulated depreciation and impairment losses. Revaluations must be regular (e.g., every 3–5 years) and applied to entire asset classes.

- Impact on Depreciation:

- The depreciable amount is recalculated based on the revalued carrying amount (fair value minus residual value) over the asset’s remaining useful life.

- This is applied prospectively from the revaluation date.

- Upward revaluations typically increase future depreciation expenses, while downward ones may decrease them.

- Treatment of Excess Depreciation: The difference between depreciation on the revalued amount and original cost can be transferred annually from revaluation surplus (in equity) to retained earnings (not through profit or loss). This does not alter the depreciation expense itself but adjusts equity.

- Deferred Tax: Revaluation creates temporary differences, so deferred tax is recognized under Ind AS 12 Income Taxes.

36. What Is Component Depreciation?

Component depreciation (also known as the component approach or component accounting) is an accounting method for depreciating property, plant, and equipment (PPE) where a complex asset is broken down into its significant individual parts (components), and each significant component is depreciated separately over its own useful life.

This approach ensures that depreciation more accurately reflects the actual consumption of economic benefits from each part of the asset, rather than treating the entire asset as a single unit.

Key Requirements (Under IFRS/Ind AS 16)

- As per IAS 16/Ind AS 16 Property, Plant and Equipment, each part of an item of PPE with a cost that is significant in relation to the total cost of the item must be depreciated separately if it has a different useful life or pattern of consumption.

- Components are identified at acquisition or construction.

- When a component is replaced, the old component’s carrying amount is derecognized (removed from books), and the new one is capitalized and depreciated over its useful life.

- This is mandatory under IFRS/Ind AS for significant components; minor parts can be grouped with the main asset.

37. When Is Component Depreciation Required?

Component depreciation (or the component approach) is required under IFRS (IAS 16 Property, Plant and Equipment) and its Indian converged standard Ind AS 16 when an item of PPE has significant parts with different useful lives or patterns of consumption of economic benefits.

Specific Conditions for Requirement (Ind AS 16, Paragraph 43-45)

- For Ind AS-applicable companies (e.g., listed companies, large unlisted entities with net worth thresholds as per MCA roadmap): Fully mandatory under Ind AS 16.

- For other companies (following Indian GAAP/AS 10 and Companies Act, 2013): Schedule II of the Companies Act, 2013 encourages and effectively requires component accounting where a part’s cost is significant and its useful life differs from the main asset. Notes to Schedule II explicitly state: “Where cost of a part of the asset is significant to total cost… and useful life of that part is different…, depreciate separately.”

- Transition: Made mandatory from FY 2015-16 onward for corporate depreciation calculations.

38. What Is Bonus Depreciation?

India offers an additional depreciation allowance as an incentive for manufacturing and power sectors, but it is more limited:

- Rate: 20% of the actual cost (in addition to normal depreciation).

- Eligibility:

- New machinery or plant (excluding ships, aircraft, office appliances, road vehicles not plying for hire, or second-hand assets).

- Acquired and installed after March 31, 2005.

- Used in the business of manufacture/production of any article/thing or generation/transmission/distribution of power.

- Conditions:

- If the asset is put to use for less than 180 days in the year of acquisition, only 10% (half) is allowed that year; the balance 10% in the next year.

- Not available for assets used outside India before installation or installed in office/residential premises.

- Higher Rate in Special Cases: Up to 35% for setups in notified backward areas (between April 1, 2015, and March 31, 2020).

39. Why Tax Depreciation Differs From Book Depreciation?

There are several points of differences between Tax Depreciation Vs Book Depreciation that you need to be well aware of. Some of the key factors to consider here are as follows:-

| Reasons Why They Differ | Book Depreciation | Tax Depreciation |

|---|---|---|

| Purpose | Show true & fair profit to shareholders, banks, investors | Reduce taxable income quickly → pay less tax this year |

| Governing law | Companies Act 2013 + Ind AS 16 (or AS 10 for smaller companies) | Income Tax Act 1961 – Section 32 |

| Method used | Usually Straight-Line (very even every year) or Units-of-Production | Always Written Down Value (WDV) on “Block of Assets” |

| Useful life / rates | Based on actual estimated useful life (management’s judgment) | Fixed rates set by government (e.g. 15 % machinery, 40 % computers) |

| Component accounting | Mandatory for significant parts (different lives) | Not required – everything goes into one block |

| Revaluation / additional depreciation | Allowed (fair value + optional excess transfer) | Not allowed (except 20 % extra for manufacturing/power only) |

| Result on profit | Profit looks more stable and realistic | Profit looks lower → tax saving (especially early years) |

40. What Is Matching Principal In Relation To Depreciation?

The matching principle is one of the fundamental accounting concepts (under both IFRS/Ind AS and Indian GAAP). It states:

Expenses should be recognised in the same accounting period as the revenues they help generate.

Depreciation is the direct application of the matching principle to non-current (fixed) assets.

Why Depreciation Exists Because of Matching

- When you buy a fixed asset (e.g., machine ₹10 lakh with 10-year life), the cash goes out in Year 1.

- But the machine helps earn revenue for the next 10 years.

- If you expense the full ₹10 lakh in Year 1 → profit in Year 1 crashes, and later years show unrealistically high profits.

- This violates matching: the cost is not matched to the revenues it produces.

41. How Do You Calculate Depreciation If An Asset Purchased In Mid Year?

When an asset is bought mid-year, you don’t charge full-year depreciation in the year of purchase (or sale).

Instead, you charge pro-rated (partial-year) depreciation based on how many months/days the asset was actually used.

This applies the matching principle properly — you only expense the portion for the period the asset helped generate revenue.

1. In Financial Books (Ind AS 16 / Companies Act, 2013)

- No strict rule on exact method — management policy decides.

- Most common practice in India:

- If asset is put to use for ≥180 days in the year → charge full year depreciation.

- If <180 days → charge half year depreciation.

- Some companies use monthly pro-rata (more accurate, especially listed companies).

- Straight-Line Method is most common in books.

2. For Income Tax Purposes (Income Tax Act, 1961)

- Very clear rule (same 180-day rule):

- Asset put to use for ≥180 days → full normal rate on the block.

- <180 days → only half the normal rate that year (balance in next year).

- Always Written Down Value (WDV) on block of assets.

- Additional depreciation (20%) also halved if <180 days.

Tax Example (New machinery ₹10 lakh, block rate 15%, eligible for 20% additional dep.)

42. What Is The Sum Of Years Digit Method?

The Sum-of-the-Years’-Digits (SYD) method is an accelerated depreciation technique.

It charges higher depreciation expense in the early years of an asset’s life and lower amounts later — exactly the opposite of straight-line.

This matches reality for many assets: they lose value (or productivity) faster when new (e.g., vehicles, computers, machinery).

It is allowed under:

- Ind AS 16 / IAS 16 (as long as it reflects the pattern of consumption)

- Companies Act, 2013 (Schedule II permits any systematic basis)

- Income Tax Act → Not allowed (tax uses only WDV on block)

How It Works – Step by Step

- Estimate useful life in years (say n years).

- Calculate the sum of digits: 1 + 2 + 3 + … + n Formula = n(n + 1)/2

- Each year, depreciation = (Remaining useful life / Sum of digits) × Depreciable amount (Depreciable amount = Cost – Salvage/Residual value)

43. Why Use Accelerated Depreciation Method?

Accelerated depreciation methods (e.g., Double Declining Balance, Sum-of-the-Years’-Digits (SYD), or Written Down Value in India) charge higher depreciation expenses in the early years of an asset’s life and lower amounts later. This contrasts with straight-line, which spreads costs evenly.

Companies and tax laws favor them for these key reasons:

1. Better Matching Of Expenses With Revenue

Many assets (e.g., machinery, vehicles, computers) are most productive and efficient when new → generate higher revenues early on.

Higher depreciation early matches higher costs to higher benefits → more accurate profit picture.

2. Tax Benefits & Cash Flow Advantage

Higher early deductions → lower taxable income now → pay less tax today (defer tax to future).

Due to time value of money, a rupee saved today is worth more than later (can be reinvested).

Improves early cash flow — crucial for growing businesses or big investments.

In India:

- Tax law uses WDV (accelerated) by default on blocks → automatic tax deferral.

- Additional depreciation (20% extra for manufacturing) acts like bonus acceleration.

- Special 40% rate for solar → huge incentive for renewables.

3. Reflects Real Economic Wear & Tear

Assets often lose value faster early (obsolescence, heavy initial use, higher repairs later).

Accelerated methods give a more realistic balance sheet → asset book value drops quicker initially.

44. What Happens To Depreciation If Useful Life Is Revised?

Under Ind AS 16 / IAS 16 (and Schedule II of Companies Act, 2013 in India), a change in estimated useful life is treated as a change in accounting estimate — not a change in policy or error.

Key Rule: The revision is applied prospectively (from the date of change onward).

No retrospective adjustment — you do not go back and change past depreciation.

How to Calculate Revised Depreciation

- At the revision date: Take the asset’s current carrying amount (cost – accumulated depreciation till date).

- Subtract revised residual value (if changed).

- Divide by the new remaining useful life.

- This gives the new annual depreciation going forward.

No impact on prior years’ profits.

45. Can Depreciation Be Negative?

No — depreciation cannot be negative.

Depreciation expense is always zero or positive (or exactly zero when an asset is fully depreciated).

Here’s why, broken down simply:

What Depreciation Actually Is

- Depreciation = systematic allocation of an asset’s cost over its useful life.

- It is an expense → reduces profit and reduces the asset’s carrying amount on the balance sheet.

- By definition, an expense cannot be negative (a negative expense would mean income, which depreciation never is).

46. How Is Depreciation Treated In Cash Flow Statement?

Depreciation is a non-cash expense. It reduces profit in the Income Statement but does NOT involve any cash outflow.

That’s why in the Cash Flow Statement, depreciation is added back to profit when calculating cash flow from operating activities.

Where Exactly It Appears (Ind AS 7 / AS 3)

Most companies in India (and worldwide) use the Indirect Method for Cash Flow from Operating Activities.

Format Of Depreciation

47. What Is A Fixed Asset Register?

A Fixed Asset Register (FAR) is a detailed, comprehensive record (usually a spreadsheet or database in accounting software) that lists all the tangible fixed assets owned by a company.

It tracks every asset from purchase to disposal, ensuring accurate depreciation, compliance, and control over valuable items like machinery, vehicles, buildings, furniture, and equipment.

It is not part of the general ledger but a supporting schedule that reconciles to the PPE (Property, Plant & Equipment) balance in financial statements.

Why Maintain a Fixed Asset Register?

- Accurate depreciation calculation (straight-line, WDV, etc.).

- Physical verification — easy to check if assets actually exist (mandatory for auditors).

- Tax compliance — matches book vs. tax depreciation (India-specific differences).

- Insurance & risk management — know what to insure and values.

- Internal control — prevents theft/loss; tracks location and custodian.

- Statutory requirement — Companies Act, 2013 (India) indirectly requires it via proper records for PPE; auditors always ask for it.

48. Why Do You Need To Reconcile Fixed Assets Periodically?

Fixed asset reconciliation compares the Fixed Asset Register (FAR) with the General Ledger (GL), physical assets on-site, and other records. You perform it periodically (monthly/quarterly for large companies, at least annually) to ensure accuracy, compliance, and control.

Here are the main reasons it’s essential:

1. Ensure Accuracy of Financial Statements

- The FAR must match the GL PPE balance. Discrepancies (e.g., missed additions/disposals) lead to overstated/understated assets, wrong depreciation, and incorrect profits.

2. Detect Errors, Fraud, or Theft Early

- Periodic checks catch unrecorded sales, misplaced assets, ghost entries, or fraudulent additions.

3. Physical Verification and Existence Confirmation

- Companies conduct physical counts (tagging/barcoding) and reconcile to the register to confirm assets exist, are in good condition, and are correctly located.

4. Proper Depreciation and Tax Compliance

- Ensures correct accumulated depreciation → accurate net book value. In India, it helps manage book vs. tax differences (deferred tax under Ind AS 12).

5. Statutory and Audit Requirements

- Companies Act, 2013 (India) requires proper records of fixed assets. Auditors always demand reconciliation and physical verification reports. Ind AS 16 mandates reviews for impairment/revisions.

6. Better Asset Management and Decision-Making

- Identifies under-utilised/obsolete assets, supports insurance claims, and aids budgeting for replacements.

49. What Is Capitalized Interest In Relation To Assets?

Capitalized interest (also called capitalized borrowing costs) is the interest on borrowed funds that is added to the cost of a long-term asset instead of being expensed immediately in the profit and loss statement.

This happens when the borrowing is used to finance the acquisition, construction, or production of a qualifying asset — one that takes a substantial period of time (usually more than 12 months) to get ready for its intended use or sale.

The rule comes from Ind AS 23 Borrowing Costs (converged with IAS 23), mandatory for companies following Ind AS in India.

Why Capitalize Interest?

- It follows the matching principle: The interest cost is part of bringing the asset to working condition → match it with future revenues the asset will generate.

- Without capitalization → profits too low during construction → too high later.

- With capitalization → asset cost higher → higher future depreciation → smoother profits.

50. Explain The Cost Principal In Asset Depreciation

The cost principle (also known as the historical cost principle) is a fundamental accounting concept that requires assets to be recorded and maintained at their original purchase cost (historical cost) on the balance sheet, rather than their current market value or replacement cost.

In relation to depreciation, this means:

- Depreciation is calculated based on the historical cost of the asset (minus any residual value).

- The asset’s carrying amount decreases systematically over its useful life, but always starts from and references the original cost.

- No upward adjustments for increases in market value are allowed under this principle (downward for impairments only).

This is the default model (called the cost model) under Ind AS 16 / IAS 16 Property, Plant and Equipment and most accounting frameworks worldwide.

Key Features of the Cost Principle for Assets

- Historical cost includes: Purchase price + directly attributable costs (e.g., freight, installation, taxes, capitalized interest).

- Depreciation base: Historical cost – residual value, allocated over useful life.

- No revaluation upward: Assets stay at cost less accumulated depreciation and impairment.

Final Takeaway

Hence, these are some of the crucial depreciation questions that you must be well aware off. Some of the key factors to remember in this case are mentioned above. However, you should not make your choices on the wrong end.

You can share your views and comments in our comment box. This will help us to know your take on this matter. Here, proper planning holds the key. Ensure that you follow the correct solution from your end.

- No Experience? No Problem. Here’s How Freshers Are Landing SAP FICO Jobs in India Right Now - June 19, 2026

- Stop Wasting Hours on Spreadsheets: The Ultimate Guide to Excel Training for Beginners (And How It Lands Jobs) - June 12, 2026

- The Laptop Lifestyle: How to Pivot to a High-Paying Data Career in 2026 - June 6, 2026