.jpg)

25 Important BRS Questions For Interview Preparation

BRS questions typically involve preparing the statement from given data, updating the cash book for unrecorded items, and adjusting balances to arrive at the correct figure. These problems test understanding of reconciling items, error detection, and fraud prevention.

A Bank Reconciliation Statement (BRS) is a key financial tool in accounting that reconciles the difference between the cash balance shown in a company’s cash book and the balance as per the bank statement (passbook). It identifies timing differences and errors, such as outstanding cheques, deposits in transit, bank charges, interest credited, or direct debits/credits not yet recorded.

Common in Class 11/12 accountancy, CA Foundation, and professional exams, BRS questions emphasize practical application, accuracy in financial records, and cash flow management.

Interview Questions

- 1. What Is A Bank Reconciliation Statement (BRS)?

- 2. Why Is BRS Important?

- 3. What Are The Common Reasons For Differences Between Cash Book And Bank statement?

- 4. How Would You Treat An Outstanding Check In BRS?

- 5. How Do You Handle Bounced Checks In Reconciliation?

- 6. How Often Should BRS Be Performed?

- 7. How Do You Perform BRS In ERP Systems Like SAP Or QuickBooks?

- 8. Describe A Situation Where Balances Didn’t Reconcile And How You Resolved It.

- 9. How Do You Prevent Fraud or Manipulation In BRS?

- 10. What Reports Do You Prepare After BRS?

- 11. How Do You Handle Long-standing Unreconciled Items

- 12. What Is A ‘Deposit In Transit’?

- 13. Walk Through The Process To Reconcile A Bank Statement With The General Ledger.

- 14. How Do You Handle Discrepancies During Reconciliation?

- 15. What Steps Do You Take To Identify And Prevent Fraud in Reconciliation?

- 16. How Do You Manage Multi-Currency Bank Accounts In BRS?

- 17. What Are The Key Components To Look For When Performing A Bank Reconciliation?

- 18. How Do You Ensure Regulations In BRS?

- 19. What Is The Treatment for Bank Service Charges In BRS?

- 20. How Are Outstanding Cheques Handled In Reconciliation?

- 21. If A Check Is Recorded Incorrectly In books (e.g., Rs 76 as Rs 67), How Do You Adjust?

- 22. Prepare A BRS Where Cash Book > Bank Balance (e.g., Rs 2210 vs. Rs 2000 With Specifics Like Deposits In Transit Rs 500, Bank Charges Rs 60).

- 23. Handle A Scenario With Bank Balance > Cash Book (e.g., Rs 5000 vs. Rs 1650 With Duplicates And Unrecorded items).

- 24. How Do You Reconcile Electronic Payments Not On The Statement?

- 25. What KPIs Do You Track For BRS Performance?

- Final Takeaway

List Of BRS Questions & Answers For Interview

There are some crucial BRS questions that you need to clear for your interview process. You cannot just make your choices out of the dark. So, let’s explore those questions one after the other.

1. What Is A Bank Reconciliation Statement (BRS)?

A Bank Reconciliation Statement (BRS) is a financial document prepared by a business or individual to compare and reconcile the cash balance recorded in their own accounting records (typically the cash book or general ledger) with the balance shown on the bank’s statement (passbook) as of a specific date.

The primary purpose of a BRS is to identify and explain any differences between these two balances, which arise due to timing differences, unrecorded items, or errors. Common reconciling items include:

- Outstanding checks: Checks issued but not yet cleared by the bank.

- Deposits in transit: Deposits recorded in the books but not yet credited by the bank.

- Bank charges/fees or interest: Deducted or added by the bank but not yet entered in the books.

- Errors: Mistakes in recording transactions by either party.

Preparing a BRS ensures accurate financial records, detects fraud or errors early, improves cash flow management, and supports compliance during audits. It is one of the basic BRS questions to know.

Opt for a NAAC A + AICTE approved BBA Degree1-year paid internship + 10 Simulation Software + 4 Certifications. 90% Practical Learning. |

|

| Bachelor in Accounting and Finance |

2. Why Is BRS Important?

The Bank Reconciliation Statement (BRS) is crucial in accounting and financial management for several key reasons. It serves as a vital internal control tool to maintain the integrity of financial records.

- Ensures Accuracy of Financial Records

BRS identifies and corrects discrepancies between the company’s cash book and bank statement, ensuring the reported cash balance is correct and reliable for financial statements.

- Detects Errors and Omissions

It uncovers recording mistakes by either the business (e.g., wrong amounts) or the bank, allowing timely corrections.

- Records Unnoted Bank Items

Captures bank charges, interest earned, direct debits/credits, or NSF checks not yet entered in the books, keeping records up-to-date.

- Improves Cash Flow Management

Provides a true picture of available cash by accounting for outstanding items, helping avoid overdrafts and plan better.

- Supports Audit and Compliance

Demonstrates strong internal controls, essential for audits, tax filings, and regulatory compliance (e.g., under GAAP/IFRS).

3. What Are The Common Reasons For Differences Between Cash Book And Bank statement?

Differences between the cash book (company’s records) and bank statement (bank’s records) are normal and usually arise from timing differences (transactions recorded by one party but not the other) or errors. These are reconciled through a Bank Reconciliation Statement (BRS).

1. Timing Differences (Most Common)

These occur due to delays in processing and do not require immediate correction beyond reconciliation.

- Outstanding Checks (Unpresented Checks): Checks issued and recorded in the cash book (deducted) but not yet presented to or cleared by the bank. Deduct from bank statement balance in BRS.

- Deposits in Transit (Uncredited Deposits): Cash/checks deposited and recorded in the cash book (added) but not yet credited by the bank (e.g., late-day deposits).

- Add to bank statement balance in BRS.

2. Items Recorded by Bank but Not Yet in Cash Book

These require journal entries in the cash book after reconciliation.

- Bank Charges/Fees/Service Charges: Deducted by the bank (e.g., monthly fees, transaction charges) but not yet recorded.

- Interest Credited/Earned: Added by the bank but unknown to the company until the statement arrives. Add to cash book balance.

- Direct Debits/Payments or Standing Orders: Automatic payments (e.g., insurance) deducted by the bank.

- Direct Credits/Collections: Amounts credited directly (e.g., dividends, collections by bank).

- Dishonored/Bounced Checks (NSF – Not Sufficient Funds): Customer checks deposited but returned unpaid; bank reverses the credit and may charge fees.

3. Errors

These are unintentional mistakes and need correction.

- Errors by the Company: Wrong amounts recorded, omissions, or duplicates in the cash book.

- Errors by the Bank: Rare, but possible (e.g., wrong crediting); adjust in BRS and notify the bank.

4. How Would You Treat An Outstanding Check In BRS?

An outstanding check (also called unpresented or uncleared check) is a check issued by the company and already recorded in the cash book (deducted from the balance) but not yet presented to or cleared by the bank by the reconciliation date.

Treatment in Bank Reconciliation Statement (BRS)

- Outstanding checks are a timing difference.

- They cause the cash book balance to be lower than the bank statement balance.

- In the BRS, deduct the total outstanding checks from the bank statement balance to arrive at the reconciled balance.

No journal entry is required for outstanding checks during reconciliation because the deduction was already recorded in the cash book when the check was issued. The item will automatically reconcile when the check clears in a future period.

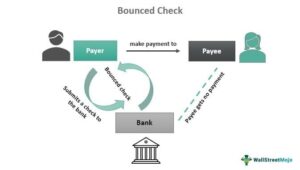

5. How Do You Handle Bounced Checks In Reconciliation?

A bounced check (also called dishonored check, returned check, or NSF – Not Sufficient Funds check) occurs when a check deposited by the company is returned unpaid by the payer’s bank due to insufficient funds or other reasons.

Steps to Handle Bounced Checks in Bank Reconciliation:

- Identify on Bank Statement The bank reverses the original credit and deducts the check amount (plus any NSF fees) from your account. This appears as a deduction on the statement.

- Update the Cash Book (Requires Journal Entry) Since the deposit was already added to the cash book earlier, reverse it now:

- Debit Accounts Receivable (reinstate the debt from the customer).

- Credit Cash/Bank (reduce the balance).

- Record any bank NSF charges separately (Debit Expense, Credit Cash).

- Treatment in BRS

- If starting from bank statement balance: Deduct the bounced check amount and fees (already handled by bank).

- If starting from cash book balance (before updating): Deduct the amount and fees to reflect the reversal.

6. How Often Should BRS Be Performed?

The frequency of preparing a Bank Reconciliation Statement (BRS) depends on the business volume, transaction complexity, industry regulations, and risk profile. However, monthly reconciliation is the standard best practice for most organizations, aligning with bank statement cycles and month-end closes.

Recommended Frequencies by Business Type:

- Small Businesses/Low Transaction Volume (e.g., retail shops, freelancers): Monthly – Sufficient to catch errors without overburdening resources.

- Medium Businesses/Moderate Volume (e.g., services, e-commerce): Weekly or Bi-weekly – Monitors cash flow closely, especially with digital payments.

- High-Volume/Large Enterprises (e.g., corporations, banks, retail chains): Daily or Real-Time – Essential for high cash turnover to prevent overdrafts, fraud, and liquidity issues. Use automated tools.

- Regulated Industries (e.g., banking, nonprofits, public companies): Daily/Weekly + Monthly – Mandated by SOX, GAAP/IFRS, or internal audits for compliance.

7. How Do You Perform BRS In ERP Systems Like SAP Or QuickBooks?

Bank Reconciliation Statement (BRS) in ERP systems is largely automated compared to manual processes, reducing errors and time. Systems like SAP (enterprise-level) and QuickBooks (SMB-focused) handle imports, auto-matching, and postings differently.

Bank Reconciliation in QuickBooks (Primarily QuickBooks Online – QBO)

QuickBooks excels in user-friendly, automated reconciliation, especially with bank feeds.

Step-by-Step Process:

- Connect Bank Account: Link your bank via bank feeds for automatic transaction downloads.

- Go to Reconcile: Gear icon > Tools > Reconcile (or Accounting > Reconcile).

- Select Account: Choose the bank/credit card account.

- Enter Statement Details: Input Ending Balance and Ending Date from your bank statement.

- Match Transactions: Review downloaded transactions; check off matches. Use filters/rules for efficiency.

- Resolve Differences: Investigate discrepancies (e.g., missing transactions, duplicates).

- Finish: When Difference = $0, click Finish Now. View/print reconciliation report.

8. Describe A Situation Where Balances Didn’t Reconcile And How You Resolved It.

Example: Mismatch due to wrong opening balance; recheck prior reconciliations, correct with journal entry. Tip: Use STAR method (Situation, Task, Action, Result)

9. How Do You Prevent Fraud or Manipulation In BRS?

Key Measures to Prevent Fraud or Manipulation in BRS

- Access Controls & Authentication

- Role-based access ensures only authorized personnel can input or modify data.

- Multi-factor authentication reduces the risk of unauthorized logins.

- Audit Trails

- Every transaction or change is logged with timestamps, user IDs, and details.

- Immutable logs make it easier to detect suspicious activity or unauthorized edits.

- Data Validation & Integrity Checks

- Automated checks flag inconsistencies, duplicate entries, or unusual patterns.

- Cross-verification with external data sources ensures accuracy.

- Segregation of Duties

- Splitting responsibilities (e.g., data entry vs. approval) prevents one person from manipulating the system unchecked.

- Critical processes require dual authorization.

- Encryption & Secure Communication

- Encrypting data both at rest and in transit prevents tampering or interception.

- Secure APIs and protocols ensure safe integration with other systems.

- Regular Monitoring & Analytics

- Continuous monitoring with anomaly detection tools highlights irregular reporting patterns.

- AI-driven fraud detection can identify manipulation attempts in real time.

- Independent Reviews & Audits

- Periodic internal and external audits validate the integrity of reports.

- Surprise checks discourage fraudulent behavior.

10. What Reports Do You Prepare After BRS?

Reconciliation Report

- Summarizes differences between the bank statement and company’s cash book.

- Lists outstanding checks, deposits in transit, and bank charges not yet recorded.

Exception/Discrepancy Report

- Highlights unusual items such as unauthorized withdrawals, duplicate entries, or errors.

- Useful for fraud detection and corrective action.

Adjustment Entries Report

- Details journal entries made to correct errors or record missing transactions.

- Ensures the company’s books align with the reconciled balance.

Cash Flow Report

- Updated cash flow statement reflecting reconciled balances.

- Helps management assess liquidity and plan for upcoming obligations.

Compliance & Audit Report

- Prepared for internal/external auditors to demonstrate adherence to accounting standards.

- Includes supporting documents and reconciliation evidence.

Management Summary Report

- A concise overview for senior management.

- Focuses on reconciled balance, key variances, and recommendations.

Few related topics for your knowledge

- Job Guarantee Vs Job Assistance: Core Points Of Differences Between The Two

- 10 Life Changing Simulation Softwares To Learn In Upcoming Years

- Top 20 Journal Entries Questions And Answers For Interview

- 50 Important Cash Book Questions & Answers For Interview Preparation

- 25 Important BRS Questions For Interview Preparation

11. How Do You Handle Long-standing Unreconciled Items?

Long-standing unreconciled items in a Bank Reconciliation Statement (BRS) can be tricky, and if not addressed properly, they may signal errors, fraud, or inefficiencies. Here’s how they are typically handled:

Steps to Handle Long-Standing Unreconciled Items

- Investigate the Cause

- Check whether the item is due to timing differences (e.g., deposits in transit, outstanding checks).

- Verify if it’s an error in recording, duplication, or omission.

- Communicate with the Bank

- Contact the bank to confirm whether the transaction actually occurred.

- Request supporting documents (e.g., copies of checks, deposit slips).

- Correct Errors Promptly

- If the issue is on the company’s side (wrong entry, missed posting), pass adjustment entries in the cash book.

- If the error is on the bank’s side, request corrections through the bank.

- Escalate Persistent Items

- Items that remain unreconciled for several months should be escalated to management or auditors.

- This ensures accountability and prevents concealment of fraud.

- Write-Off or Adjust (if justified)

- If after thorough investigation the item cannot be resolved (e.g., very old outstanding checks unlikely to be presented), management may approve a write-off or reversal.

- Must comply with accounting standards and company policy.

- Strengthen Controls

- Review internal processes to prevent recurrence.

- Implement stricter cut-off procedures, better documentation, and more frequent reconciliations.

12. What Is A ‘Deposit In Transit’?

A deposit in transit (also known as an outstanding deposit) is cash or checks that a company has received, recorded in its accounting records, and sent to the bank, but which the bank has not yet processed or credited to the account by the date of the bank statement.

This creates a temporary timing difference: the company’s books show a higher cash balance than the bank’s statement.

Common Causes

- Deposits made late in the day, after banking hours, on weekends, or holidays.

- Mailed deposits with processing delays.

- End-of-month deposits that fall just outside the bank’s cutoff.

13. Walk Through The Process To Reconcile A Bank Statement With The General Ledger.

Bank reconciliation is the process of matching the cash balance in your company’s general ledger (book balance) with the balance shown on the bank statement. This identifies and explains any differences due to timing or errors, ensuring accurate financial records.

Step 1: Gather Necessary Documents

- Obtain the bank statement for the period (typically month-end).

- Have your company’s general ledger cash account (or cash book) detail for the same period.

- Collect supporting records: deposit receipts, canceled checks, prior reconciliation (for any outstanding items).

Step 2: Compare Beginning Balances

- Note the ending balance from the prior month’s bank reconciliation (this should match both the prior bank statement and your adjusted book balance).

- Verify it aligns with the beginning balance on the current bank statement and in your ledger.

Step 3: Update the Book Balance for Bank-Related Items (Items the Bank Knows but You May Not)

Start with the cash balance per general ledger (books).

Add or subtract items discovered from the bank statement:

- Add:

- Interest earned (bank credits interest you haven’t recorded yet).

- Collections made by the bank (e.g., notes receivable collected on your behalf).

- Any other credits on the bank statement not yet recorded in your books.

- Subtract:

- Bank service charges or fees.

- NSF (non-sufficient funds) checks (customer checks that bounced).

- Automatic withdrawals or payments the bank processed.

- Any other debits on the bank statement not yet recorded.

→ Make journal entries in your general ledger for these items (e.g., debit Cash for interest, credit Cash for fees).

This gives you the adjusted book balance.

Step 4: Update the Bank Balance for Company-Related Items (Timing Differences)

Start with the ending balance per bank statement.

Add or subtract timing differences:

- Add:

- Deposits in transit (outstanding deposits): Deposits you recorded but the bank hasn’t credited yet (e.g., late-day or mailed deposits).

- Subtract:

- Outstanding checks: Checks you issued and recorded but haven’t cleared the bank yet.

(No adjustments needed for errors yet—handle those separately.)

This gives you the adjusted bank balance.

Step 5: Compare Adjusted Balances

- The adjusted book balance should now equal the adjusted bank balance.

- If they match → Reconciliation is complete.

- If they don’t match → Investigate differences

14. How Do You Handle Discrepancies During Reconciliation?

Discrepancies occur when the adjusted bank balance and adjusted book balance do not match after accounting for normal timing differences (deposits in transit, outstanding checks) and bank-initiated items (interest, fees, NSF checks).

Follow this systematic approach to identify and resolve them:

- Re-check Basic Arithmetic

- Compare Transactions Item by Item

- Investigate Timing Differences More Closely

- Look for Unrecorded or Misrecorded Items

- Search for Fraud or Unauthorized Transactions

- Use Supporting Tools and Reports

- Resolve the Discrepancy

- Document Everything

15. What Steps Do You Take To Identify And Prevent Fraud in Reconciliation?

Bank reconciliation is a powerful detective control that helps uncover fraudulent activity by highlighting unauthorized or manipulated transactions. Follow these steps to actively identify fraud:

- Perform Reconciliations Frequently Conduct reconciliations monthly at minimum, or more often (weekly/daily) for high-volume or high-risk accounts. Frequent reviews catch issues early, before losses grow.

- Look for Unusual or Unauthorized Transactions Scrutinize the bank statement for:

- Unexpected withdrawals, wires, ACH transfers, or ATM activity.

- Checks with altered amounts, payees, or endorsements.

- Duplicate payments or fictitious vendors.

- Transactions on weekends/holidays or round amounts that seem suspicious.

- Review Cleared Checks Thoroughly If available (via online images), examine check images for altered payees, forged signatures, or improper endorsements (e.g., checks made to “cash” or redirected).

- Track Outstanding Items Closely Monitor old outstanding checks or deposits in transit that don’t clear promptly—these can hide “lapping” schemes (delaying deposits to cover theft) or stale checks used for fraud.

- Flag and Investigate Discrepancies Any unexplained differences (after timing adjustments) could indicate manipulation, such as hidden thefts or falsified records. Use anomaly detection for patterns like repeated small amounts.

- Compare to Supporting Documentation Trace transactions back to invoices, receipts, or approvals to verify legitimacy.

- Leverage Automation for Alerts Use software with AI-powered anomaly detection to automatically flag unusual patterns, reducing manual oversight risks.

16. How Do You Manage Multi-Currency Bank Accounts In BRS?

Bank Reconciliation Statement (BRS) for multi-currency accounts adds complexity due to exchange rate fluctuations, timing differences in conversions, bank fees in foreign currencies, and the need to align the bank’s statement (typically in the account’s currency) with your general ledger (GL), which may be in the base/reporting currency.

Step-by-Step Process for Multi-Currency BRS

- Set Up Separate Bank Accounts per Currency

Create a dedicated GL account for each foreign currency bank (e.g., USD Bank Account, EUR Bank Account). This allows tracking balances and transactions in the native currency.

Best practice: Do not mix currencies in one account—foreign currency accounts should only handle transactions in their own currency.

- Import or Enter the Bank Statement in Native Currency

Obtain the bank statement in the account’s currency (e.g., EUR statement for EUR account).

Do not convert the entire statement to base currency upfront—this introduces errors.

- Reconcile in the Bank Account’s Native Currency

- Start with balance per bank statement (native currency).

- Start with balance per books/GL converted to native currency (if GL is in base) or directly if tracked natively.

- Add/subtract standard items:

- Deposits in transit (in native currency).

- Outstanding checks (in native currency).

- Bank fees, interest, or NSF items (as shown on statement).

- Match transactions line-by-line in native currency.

- Any discrepancies due to exchange rates (e.g., bank used different rate) are recorded as realized foreign exchange gain/loss.

- Handle Exchange Rate Differences

- Realized gains/losses: Arise when settling transactions (e.g., payment cleared at different rate than recorded). Post to FX gain/loss account.

- Unrealized gains/losses: At period-end, revalue the bank balance to base currency using closing rate—post adjustment to unrealized FX account.

- In reconciliation: These are not “discrepancies” to force zero; they are normal and explained separately.

- Prepare the BRS: Format similar to single-currency, but specify currency:

17. What Are The Key Components To Look For When Performing A Bank Reconciliation?

Bank reconciliation involves comparing the company’s cash records (general ledger or “books”) with the bank’s records (bank statement) and identifying/explaining differences. The key components to examine and verify fall into three main categories: starting balances, transactions, and adjusting items.

1. Starting Balances

- Ending balance from the prior reconciliation – This should match the beginning balance on the current bank statement and in your books.

- Beginning balance per bank statement – The opening balance shown by the bank.

- Beginning balance per books – The opening cash balance in your general ledger.

2. Transactions on the Bank Statement

Carefully review all items that appear on the bank statement:

- Deposits and credits:

- Customer payments, wire receipts, interest earned, bank collections (e.g., notes receivable).

- Withdrawals and debits:

- Cleared checks, ACH payments, wire transfers, bank fees/service charges, NSF (bounced) checks, automatic deductions.

- Other bank-initiated items:

- Interest income, service charges, corrections or adjustments made by the bank.

3. Transactions in Your Books

Compare against your internal records:

- Recorded deposits – All receipts entered in the cash book or GL.

- Issued checks and payments – All disbursements (checks, wires, ACH) recorded in your system.

- Journal entries affecting cash – Any manual adjustments to the cash account.

4. Timing Differences (Normal Reconciling Items)

These are legitimate differences due to timing:

- Deposits in transit (outstanding deposits) – Deposits recorded in your books but not yet credited by the bank (e.g., late-day or mailed deposits).

- Outstanding checks – Checks issued and recorded in your books but not yet cleared/presented to the bank.

5. Book Adjustments (Items the Bank Knows but You May Not Yet)

- Unrecorded interest earned.

- Unrecorded bank fees or service charges.

- NSF checks or returned deposits.

- Automatic payments or collections processed by the bank.

18. How Do You Ensure Regulations In BRS?

Bank reconciliation is a critical internal control that helps organizations comply with financial reporting standards, anti-fraud regulations, and audit requirements. Compliance is achieved through proper process design, documentation, segregation of duties, and adherence to relevant frameworks.

Key Regulations and Standards Impacting BRS

- Sarbanes-Oxley Act (SOX) – Section 404 requires effective internal controls over financial reporting (ICFR), including cash and bank reconciliations.

- IFRS / IAS 7 and GAAP (ASC 230) – Require accurate cash flow reporting and disclosure of cash balances.

- Anti-Money Laundering (AML) / Know Your Customer (KYC) – Reconciliation helps detect unusual transactions.

- PCI DSS (if handling card payments) – Controls around cash equivalents.

- Local regulations – e.g., Companies Act requirements in many jurisdictions for timely and accurate accounts.

- Audit standards (PCAOB, ISA 265) – Require evidence of effective reconciling controls.

19. What Is The Treatment for Bank Service Charges In BRS?

Bank service charges (also called bank fees) are fees deducted by the bank for account maintenance, transaction processing, wire fees, overdraft charges, etc. These typically appear as debits on the bank statement but are often not known or recorded in the company’s books until the statement is received.

- Identification

Review the bank statement for any debit entries labeled as service charges, monthly fees, analysis charges, etc.

- Classification as a Reconciling Item

Bank service charges are items known to the bank but not yet recorded in the company’s books.

They cause the book balance to be higher than the actual available cash.

- Adjustment in the Reconciliation

In the BRS, service charges are subtracted from the cash balance per books (general ledger) to arrive at the adjusted book balance.

- Journal Entry in the Books: After the reconciliation, record the service charges in the general ledger with a journal entry (typically at month-end):

20. How Are Outstanding Cheques Handled In Reconciliation?

Outstanding checks (also called unpresented or uncleared checks) are checks that a company has issued and recorded as payments in its general ledger (books), but which have not yet cleared or been deducted by the bank as of the bank statement date.

Key Ways To Handle Outstanding Cheques in BRS

- Identification

Compare the list of issued checks (from your check register or disbursements journal) against cleared checks on the bank statement.

Any checks issued before the statement date but not appearing as debits are outstanding.

- Classification as a Reconciling Item

Outstanding checks are items recorded in the books but not yet known/reflected by the bank.

They are subtracted from the bank statement balance to arrive at the true available cash.

- Adjustment in the Reconciliation

In the BRS, outstanding checks are deducted from the balance per bank.

21. If A Check Is Recorded Incorrectly In books (e.g., Rs 76 as Rs 67), How Do You Adjust?

If a check was recorded incorrectly in the company’s books (general ledger), for example, recorded as Rs 67 when the actual check issued and cleared by the bank was Rs 76, this is a book error (not a timing difference). The company’s cash balance per books is understated by the difference (Rs 9 in this case).

Impact

- Book cash balance: Too low by Rs 9 (because a larger amount was actually paid).

- When the check clears the bank for Rs 76, the bank correctly deducts Rs 76.

- This creates a discrepancy in the reconciliation: the adjusted balances won’t match until corrected.

Treatment in Bank Reconciliation

Identify the Error

- During reconciliation, when matching cleared checks:

- Bank statement shows a debit of Rs 76 (cleared check amount).

- Books show a payment of only Rs 67. → Difference of Rs 9 flags the error.

Adjust on the Book Side

- In the Bank Reconciliation Statement (BRS), the correction is reflected by subtracting the error amount from the balance per books (since cash was under-deducted).

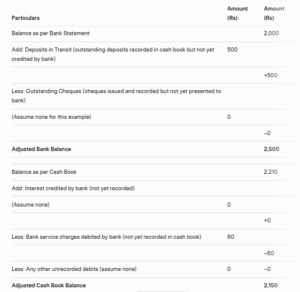

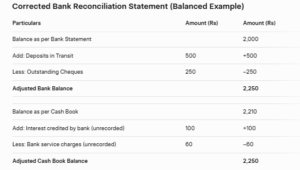

22. Prepare A BRS Where Cash Book > Bank Balance (e.g., Rs 2210 vs. Rs 2000 With Specifics Like Deposits In Transit Rs 500, Bank Charges Rs 60).

Note: In this example, the original difference between cash book (Rs 2,210) and bank statement (Rs 2,000) is Rs 210 (cash book higher).

The reconciling items are:

- Deposits in transit Rs 500 → added to bank balance

- Bank charges Rs 60 → subtracted from cash book

However, to make the reconciliation fully balance with realistic items, we need additional reconciling items that net to the remaining difference. Here is a corrected and balanced version with typical additional items:

Both adjusted balances now equal Rs 2,250, showing the true available cash position.

Explanation of Items (Typical when Cash Book > Bank Balance)

- Deposits in transit and interest credited by bank → increase the bank balance (added on bank side or book side).

- Outstanding cheques → decrease the bank balance (subtracted on bank side).

- Bank charges → decrease the cash book balance (subtracted on book side).

After posting the unrecorded items (interest and bank charges) as journal entries, the cash book will be updated and future reconciliations will start from the correct balance.

This format ensures accuracy and provides a clear audit trail.

23. Handle A Scenario With Bank Balance > Cash Book (e.g., Rs 5000 vs. Rs 1650 With Duplicates And Unrecorded items).

In bank reconciliation, when the bank statement balance is higher than the cash book (books/general ledger) balance, it typically indicates:

- Unrecorded credits in the books (e.g., interest earned, direct collections by the bank, or refunds credited by the bank but not yet entered in the company’s records). These are added to the cash book balance during reconciliation.

- Errors in the books, such as duplicate recordings of payments (debits), which overstate outflows and understate the cash book balance. These require adjustments to correct the book balance upward.

- Other possibilities include outstanding checks (subtracted from bank) or deposits in transit (added to bank), but these are timing differences that may or may not apply.

The goal is to adjust both sides so the adjusted bank balance equals the adjusted cash book balance, reflecting the true cash position. After reconciliation, post journal entries for unrecorded items and corrections to update the books.

Example Scenario

- Balance per bank statement: Rs 5,000

- Balance per cash book: Rs 1,650

- Difference: Rs 3,350 (bank higher)

- Specifics:

- Unrecorded interest credited by bank: Rs 300 (unrecorded credit → add to cash book)

- Unrecorded collection by bank (e.g., customer payment directly to bank): Rs 1,500 (unrecorded credit → add to cash book)

- Duplicate payment recorded in cash book (e.g., a Rs 1,550 check recorded twice, overstating debits → add back Rs 1,550 to cash book to correct)

- For complexity, include timing items:

- Deposits in transit: Rs 400 (add to bank)

- Outstanding checks: Rs 400 (subtract from bank) → These net to zero for simplicity.

24. How Do You Reconcile Electronic Payments Not On The Statement?

Electronic payments (ACH transfers, wire transfers, EFTs, card payments, bill pay, or payroll direct deposits) often have processing delays similar to checks or deposits.

When they have been recorded in your books but do not yet appear on the current bank statement, they are treated as outstanding (uncleared) electronic payments – essentially the equivalent of outstanding checks.

- Verify the Payment Was Properly Recorded in Your Books

Confirm the electronic payment was entered in the general ledger on the correct date and for the correct amount (including any fees).

Supporting evidence: Payment confirmation from your bank portal, ACH batch report, wire reference number, or payroll processor acknowledgment.

- Confirm the Payment Has Been Sent/Initiated

Electronic payments are not truly “outstanding” if they are still in draft or pending approval.

Check your online banking or payment platform:

Status shows “Processed,” “Sent,” or “Completed” (not “Pending” or “Scheduled for future date”).

You have a traceable reference number (e.g., ACH trace ID, Fedwire IMAD/OMAD).

- Determine Why It’s Not on the Statement

Common reasons:

1.Processing delay: ACH payments can take 1–3 business days (or longer for international wires).

2.Cutoff timing: Payment initiated after the bank’s daily cutoff or on a non-business day.

3.Batch processing: Payroll or vendor batches may post the next business day or later.

- Treat as an Outstanding Item on the Reconciliation

In the bank reconciliation:

Start with the bank statement balance.

Subtract the electronic payment amount (just like an outstanding check). This reduces the bank balance to reflect cash that has left your books but not yet hit the bank.

25. What KPIs Do You Track For BRS Performance?

Organizations track specific KPIs to evaluate the efficiency, accuracy, timeliness, and overall effectiveness of the bank reconciliation process. These metrics help identify bottlenecks, improve controls, reduce errors, support faster financial closes, and minimize risks like fraud or cash mismatches.

Here are the most commonly tracked KPIs, along with their purpose and typical targets:

- On-Time Reconciliation Completion Rate Measures the percentage of bank reconciliations completed by the scheduled deadline (e.g., within 5–10 business days after month-end). High rates indicate reliable processes and support timely financial reporting. Typical target: >95%.

- Reconciliation Cycle Time Average number of days (or hours) taken to complete a reconciliation from receipt of the bank statement to final approval. Shorter cycle times reflect efficient processes and better resource utilization. Typical target: 3–7 business days per account.

- Automation Rate / Auto-Match Rate Percentage of transactions automatically matched by reconciliation software without manual intervention. Higher rates reduce manual effort, lower error risk, and speed up the process. Typical target: >85–90%.

- Exception Rate Percentage of transactions that require manual review or intervention (unmatched items). Low rates signal good data quality and effective automation. Typical target: <5–10%.

- Number of Aged/Unreconciled Items Count of outstanding items (e.g., deposits in transit or outstanding checks) older than a certain threshold (30, 60, or 90 days). Minimizing aged items prevents persistent discrepancies and reduces fraud risk. Typical target: Zero items over 30–60 days.

Final Takeaway

Hence, these are some crucial BRS questions for interview preparation that you must not ignore from your end. Ensure that you follow the correct solution from your counterpart. This will help us to know your take on this matter.

You can share your views and comments in our comment box. This will assist us to know your take on this case. The more you share your response with us the better we will get the idea about your understanding on this matter.

- You’re Smart Enough, But English Is Holding You Back. A Fluent English Speaking Course Can Fix That - July 3, 2026

- Movement Types in SAP MM: What They Are, Why They Matter, and How to Master Them - June 26, 2026

- No Experience? No Problem. Here’s How Freshers Are Landing SAP FICO Jobs in India Right Now - June 19, 2026