.jpg)

One Price, One Tax? Understanding Composite Supply in GST

Have you ever wondered how GST works when you buy a laptop that comes with a charger? Or when you book a flight that includes a free meal? In the world of taxation, these aren’t just “deals.” They fall under a specific category called Composite Supply in GST.

Navigating the Goods and Services Tax (GST) can feel like a maze. However, understanding how bundled goods are taxed is crucial for business owners and consumers alike. Let’s break down the concept of composite supply under GST in simple terms.

Table of Contents

What is Supply and Its Different Types?

Before we dive deep, we must understand the “Supply” concept. Under GST, supply is the event that triggers tax. However, not all supplies are the same. They are categorized based on how they are packaged and sold.

1. Principal Supply

The principal supply is the main product or service that a customer wants. All other items in the bundle are secondary or supportive.

2. Composite Supply

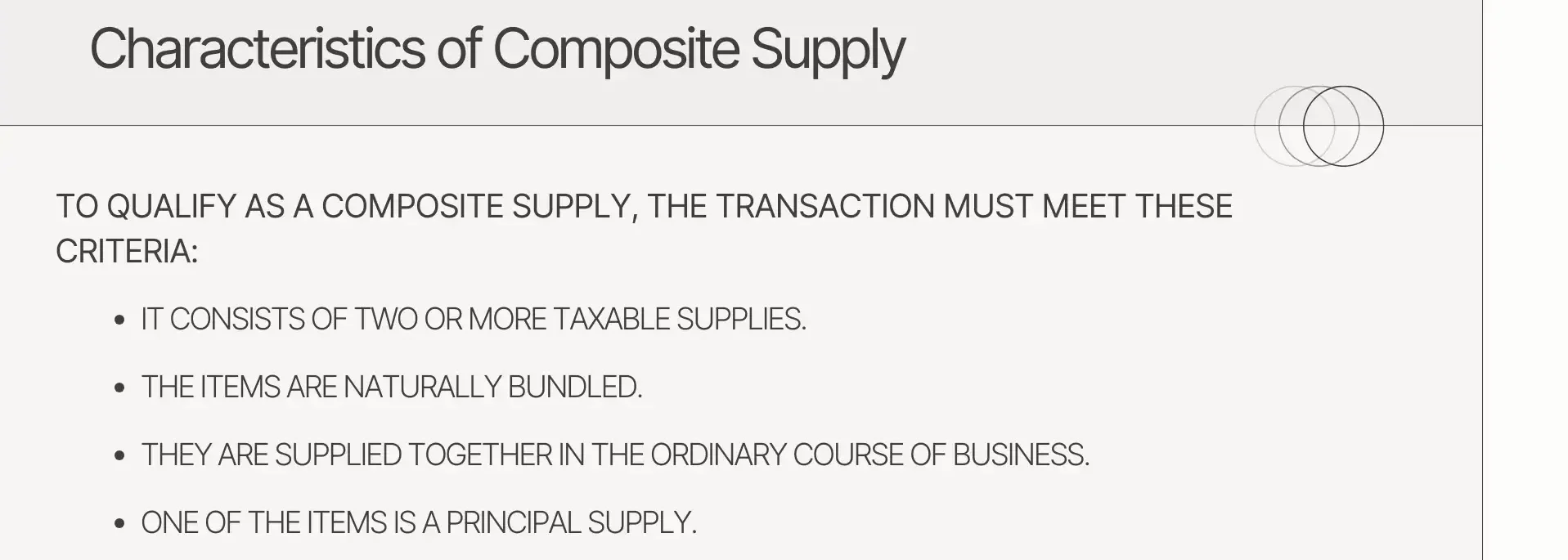

A composite supply under GST involves two or more items that are “naturally bundled.” They are sold together because they belong together in normal business practice. You cannot easily imagine one without the other.

3. Mixed Supply

Unlike composite supply, mixed supply involves items that are not naturally bundled. They are independent products sold together for a single price, usually as a promotional offer or a gift pack.

What is Composite Supply in GST?

A composite supply under GST occurs when a seller provides two or more goods or services together as a single package. These items are “naturally bundled.” This means they are usually provided together in the normal course of business.

In such a bundle, the Principal Supply dictates the tax rules. Because the items cannot be easily separated in a standard business transaction, the tax rate of the principal item applies to the entire bundle.

How to determine whether the goods or services are naturally bundled?

- The concept of natural bundling is the heart of composite supply under GST. Generally, if a buyer expects certain goods or services to be provided as a package, it is considered naturally bundled.

- If there is a main good or service and others are ancillary (supporting) items, the package becomes a bundled service.

Indications of bundling of goods or services in the ordinary course of business:

How can you tell if a bundle is “ordinary”? Here are the primary indicators:

- Single Price: There is a single price for the package, even if the value of individual components is known.

- Advertised as a Package: The components are normally marketed together rather than as standalone items.

- Availability: The different components provided with the main product are often not available for purchase separately.

Composite Supply Under GST Example

To make things clearer, let’s look at a common composite supply under the GST example.

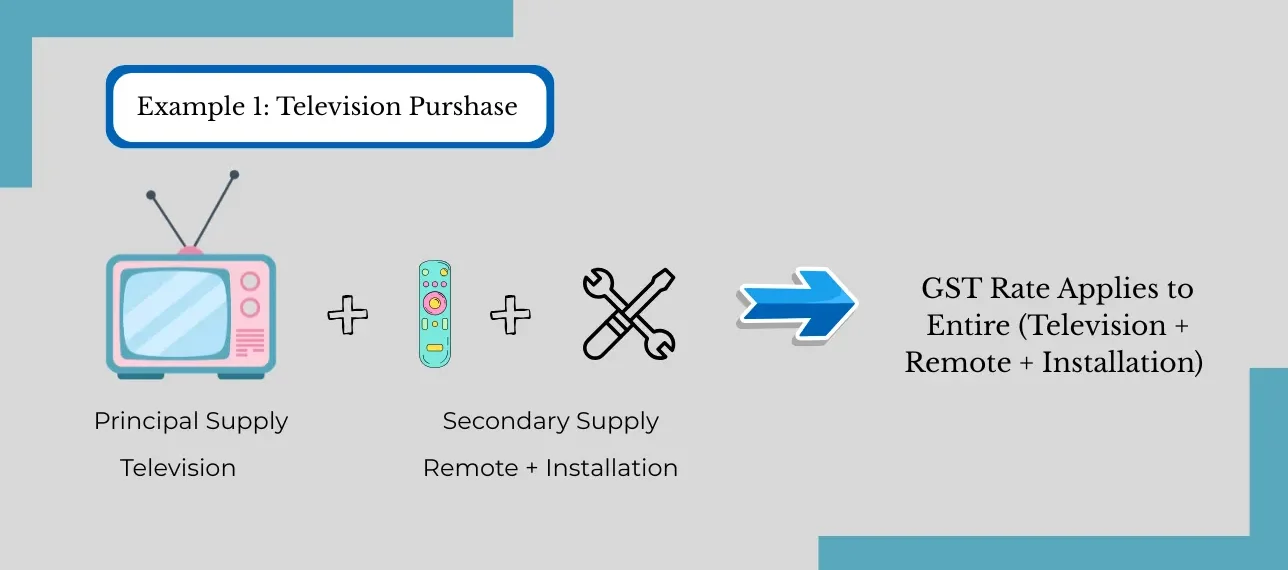

Example 1: Imagine you buy a brand-new television. The shop provides the TV along with a remote, a power cable, and an installation service. Here, the TV is the principal supply. The remote and installation are ancillary (secondary). Therefore, the GST rate applicable to the TV will apply to the whole invoice value, even for the installation service.

Example 2: Amount of air ticket includes cost of the meal to be provided during travel. The rate of tax to be charged on composite supply will be the rate on the principal supply which is transportation of passengers.

Other common examples include:

- Hotel Stay: A hotel stay with breakfast is a composite supply where the room stay is the principal supply.

- Shipping: When goods are packed and transported with insurance, the goods are the principal supply.

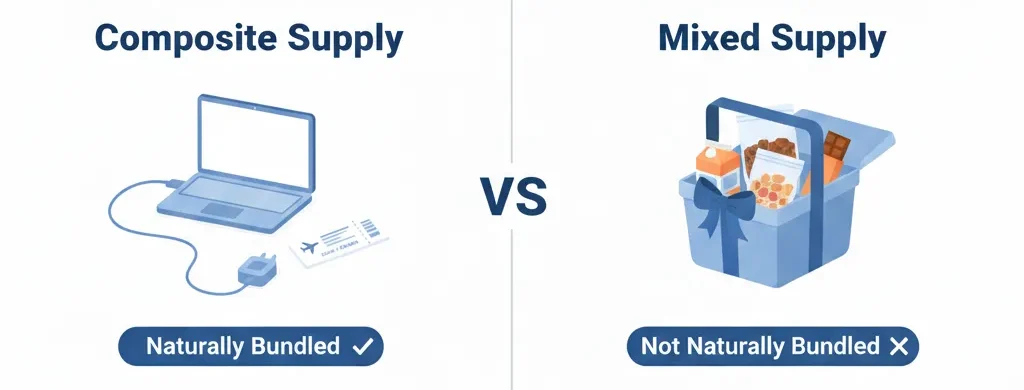

Difference Between Mixed Supply and Composite Supply in GST

It is very easy to confuse composite supply with “mixed supply.” However, the tax implications are very different. While composite supplies are naturally bundled, mixed supplies are independent items sold together for a single price.

Here is a quick comparison table to help you spot the difference between mixed supply and composite supply in GST:

| Feature | Composite Supply | Mixed Supply |

|---|---|---|

| Nature of Bundle | Naturally bundled together. | Not naturally bundled; sold by choice. |

| Principal Supply | One item is clearly the main item. | No single principal supply exists. |

| Example | Laptop with a charger. | A gift hamper with dry fruits and juices. |

| Tax Rate | Tax rate of the principal supply. | The highest tax rate among all items. |

| Business Course | Ordinary course of business. | Not necessarily the ordinary course. |

Case Study: Duronto Express Tickets

Question: If you book a Duronto Express ticket and are provided a meal during the journey, is it a composite or mixed supply?

Answer: This is a composite supply. The primary intent of the passenger is to travel from one destination to another. Therefore, train transportation is the principal supply. The meal provided is secondary and naturally bundled with the journey. As a result, the GST rate for rail travel applies to the entire ticket price.

Why Does “Natural Bundling” Matter?

Determining what is composite supply in GST often depends on the “natural bundle” aspect. If a bundle is not natural, the tax authorities might treat it as a mixed supply. This could lead to a higher tax liability.

To decide if a bundle is natural, one should look at industry practices. If most service providers in the industry offer these items together, it is likely a composite supply.

Few GST related topics for your knowledge

- Place Of Supply In GST: Importance, Meaning & Types

- 10 Essential Topics Covered In GST Courses

- How To File GSTR 1: Process, Deadlines & Penalties Explained

- GST Registration Process: Steps, Requirements, Status Checks, Benefits

- Structure of GST in India: Types, Rates, 4-Tiers Tax

- Top 50 GST Interview Questions & Answers

Conclusion

Understanding Composite Supply in GST helps businesses stay compliant and helps consumers understand their bills. By identifying the principal supply, you can easily determine the correct tax rate. Remember, if the items are inseparable in a standard business sense, it’s composite; if they are just bundled for a promotion, it’s likely mixed.

Frequently Asked Questions

1. What is the tax rate for a composite supply under GST?

The tax rate for a composite supply is the same as the tax rate applicable to the principal supply in the bundle.

2. How do I identify a principal supply in a composite supply under GST?

The principal supply is the predominant element of the transaction. It is the main good or service that the customer primarily intends to buy.

3. Can a restaurant service be considered a composite supply?

Yes. A restaurant provides food (goods) along with service. Since these are naturally bundled in the ordinary course of business, it is a composite supply of service.

4. What is the main difference between mixed supply and composite supply in GST?

The main difference is “natural bundling.” Composite supplies are items that naturally go together (like a phone and its battery), while mixed supplies are independent items bundled for a single price (like a combo pack of a shirt and a watch).

5. If I sell a car with an extended warranty, is it a composite supply?

Yes, selling a car with a warranty is a classic composite supply under GST example. The car is the principal supply, and the warranty is ancillary.

- Movement Types in SAP MM: What They Are, Why They Matter, and How to Master Them - June 26, 2026

- No Experience? No Problem. Here’s How Freshers Are Landing SAP FICO Jobs in India Right Now - June 19, 2026

- Stop Wasting Hours on Spreadsheets: The Ultimate Guide to Excel Training for Beginners (And How It Lands Jobs) - June 12, 2026