.jpg)

50 Important Cash Book Questions & Answers For Interview Preparation

Cash book questions can be critical during the interview process. The Cash Book is one of the most fundamental and frequently tested topics in accounting interviews, especially for roles such as junior accountant, accounts assistant, bookkeeper, audit trainee, or finance executive.

It serves as a primary book of original entry that records all cash and bank transactions chronologically while simultaneously functioning as a ledger account for cash and bank balances. Understanding the Cash Book thoroughly demonstrates a candidate’s grasp of basic accounting principles, transaction recording, internal controls, and reconciliation processes.

Interviewers often focus on the types of Cash Books (Single, Double, Triple Column, and Petty Cash), contra entries, treatment of discounts, bank reconciliation, imprest system, and practical scenarios involving cheques, overdrafts, and dishonoured instruments.

List Of Cash Book Questions & Answers For Interview Preparation

There are lots of Cash Book Questions that you need to prepare for the interview for getting selected for your dream job of your choice. So, let’s explore them one after the other to get a clear insight to it.

Interview Questions

- 1. What Is A Cash Book?

- 2. Why Is The Cash Book Maintained?

- 3. Is The Cashbook Journal Or Ledger?

- 4. What Are The Main Types Of Cashbooks?

- 5. What Is A Single Column Cash Book?

- 6. What Is Recorded In A Double Column Cash Book?

- 7. What Is A Triple Column Cash Book?

- 8. What Is A Petty Cash Book?

- 9. What Is The Imprest System In Cash Book?

- 10. What Is A Contra Entry In Cash Book?

- 11. How Is Cash Deposited Into Bank Recorded In Double Entry Cash Book?

- 12. How Is The Cash Withdrawn From The Bank Recorded?

- 13. What Side Does Cash Receipt Appear In The Cash Book?

- 14. What Side Do Cash Payments Appear On?

- 15. Does The Cash Book Balance Like Other Ledger Accounts?

- 16. What Is The Difference Between Cash Book & Cash Account?

- 17. Why Are Bank Charges Recorded In Cash Books?

- 18. What Is The Overdraft In Cash Book?

- 19. How Is Discount Allowed Recorded In Triple Column Cash Book?

- 20. How Is Discount Received Recorded?

- 21. Are Contra Entries Posted To The Ledger?

- 22. What Is The Purpose Of A Petty Cashbook?

- 23. What Happens If The Petty Cash Expenses Exceed The Imprest Amount?

- 24. How Is Reimbursement Recorded In Petty Cash Book?

- 25. What Is An Analytical Petty Cash Book?

- 26. Give An Example Of Contra Entry?

- 27. If a cheque is received and deposited on the same day, how is it recorded?

- 28. If A Cheque Is Received But Not Deposited Immediately

- 29. What Is A Bank Reconciliation Statement?

- 30. What Is The Difference Between Cash Book & Pass Book?

- 31. How Are Direct Deposits By Customers Are Recorded In Cash Book?

- 32. What Is Trade Discount Vs Cash Discount?

- 33. Is Petty Cash An Asset Or Expense?

- 34. How Often Is The Petty Cash Book Balanced?

- 35. What If The Cash Sales Are Directly Deposited Into Bank?

- 36. Explain The Ruling Of A Simple Cash Book?

- 37. Why Is No Separate Cash Account Maintained In Ledger When Cash Book Exists?

- 38. What Is A Favourable Balance In Cash Book?

- 39. What Is An Unfavourable Balance?

- 40. How Is A Dishonored Cheque Recorded In Cash Book?

- 41. What Are The Advantages Of Maintaining A Cash Book?

- 42. Can Interest Credited By Bank Be Recorded Directly In Cash Book?

- 43. What Is The Treatment Of Post Dated Cheques In Cash Book?

- 44. How Is Petty Cash Float Initially Recorded?

- 45. What Is The Role Of Vouchers In A Petty Cash Book?

- 46. If Petty Cash Is Lost, How Is It Treated?

- 47. What Is The Difference Between Cash & Bank Reconciliation?

- 48. How Are Standing Instructions Recorded in the Cash Book?

- 49. Why Is Petty Cash Not The Part Of The Main Cash Book?

- 50. In an interview, how would you explain the importance of accurate Cash Book maintenance?

- Final Takeaway

1. What Is A Cash Book?

A Cash Book is a special subsidiary book in accounting that records all cash and bank transactions in chronological order. It acts as both a book of original entry (journal) for recording transactions immediately and a ledger account for the cash/bank balance. Unlike other journals, postings to the Cash Ledger are not required separately because the Cash Book itself replaces the Cash Account in the ledger. It is one of the most vital and important Cash Book questions to know from your end.

Example: All cash sales, purchases, salaries paid in cash, bank deposits, etc., are recorded here.

2. Why Is The Cash Book Maintained?

It provides a complete, systematic, and real-time record of cash inflows and outflows. Key reasons:

- Instant availability of cash/bank balance for decision-making.

- Detection of errors or fraud (e.g., missing receipts).

- Control over cash, the most liquid and vulnerable asset.

- Basis for preparing Bank Reconciliation Statement (BRS).

- Compliance with accounting principles (accuracy and timeliness).

Opt for a NAAC A + AICTE approved BBA Degree1-year paid internship + 10 Simulation Software + 4 Certifications. 90% Practical Learning. |

|

| Bachelor in Accounting and Finance |

3. Is The Cashbook Journal Or Ledger?

The Cash Book is both a journal and a ledger – this dual nature is one of its most important and frequently tested features in accounting interviews.

- As a Journal (Book of Original/Prime Entry):

- Transactions are recorded chronologically (date-wise) as soon as they occur.

- Each entry has a narration (brief explanation).

- It follows the dual aspect (debit and credit) like a journal.

- No separate posting to a Cash Account is required because the Cash Book itself serves the purpose.

- As a Ledger:

- It has debit and credit sides with columns for amounts, similar to a T-shaped ledger account.

- The balance is calculated periodically (daily, weekly, or monthly) just like any other ledger account (Debit total – Credit total = Closing balance).

- The closing balance of the Cash Book is directly taken to the Trial Balance and Balance Sheet (Cash in Hand or Bank Balance/Overdraft).

4. What Are The Main Types Of Cashbooks?

The main types of Cash Books are four, classified based on business needs, transaction complexity, and volume of cash/bank/discount activities. They are subsidiary books designed to record cash and bank transactions efficiently. Here’s a detailed breakdown with features, formats, uses, examples, and journal entries:

-

Single Column

- Double Column Cash Book (Cash & Bank Cash Book)

- Triple Column Cash Book (Cash, Bank & Discount)

- Petty Cash Book

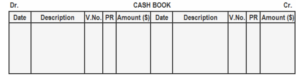

5. What Is A Single Column Cash Book?

A Single Column Cash Book (also called Simple Cash Book) is the most basic type of Cash Book in accounting. It records only cash transactions – cash receipts on the debit side and cash payments on the credit side – in a single amount column.

It is suitable for small businesses or sole proprietors that deal primarily in physical cash and have minimal or no banking transactions (no cheques, bank deposits, or transfers).

Key Features:

- One amount column on both debit and credit sides (no separate bank or discount columns).

- Acts as both a journal (chronological recording with narration) and a ledger (balance calculated like a T-account).

- No contra entries (since no bank column).

- Closing balance represents Cash in Hand.

Format Of Single Column Cash Book

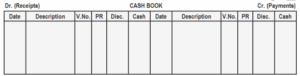

6. What Is Recorded In A Double Column Cash Book?

A Double Column Cash Book (also called Cash and Bank Cash Book) records two categories of transactions side by side using two amount columns on both debit and credit sides:

- Cash transactions (physical cash in hand)

- Bank transactions (cheques received, cheques issued, direct bank transfers, etc.)

This type is widely used in medium-sized businesses that operate both cash and current bank accounts.

What Exactly Is Recorded?

Debit Side (Receipts):

- Cash received (e.g., cash sales, cash from debtors, loans in cash).

- Cheques received and deposited (directly in the Bank column if deposited the same day, or first in Cash if kept temporarily).

- Cash deposited into the bank (contra entry – Bank column debited).

- Cash withdrawn from bank for office use (contra entry – Cash column debited).

- Direct credits by bank (e.g., interest credited, direct collection from customers).

Credit Side (Payments):

- Cash paid (e.g., cash purchases, expenses, salaries in cash).

- Cheques issued to creditors/suppliers.

- Cash withdrawn from the bank (contra – Bank column credited).

- Cash deposited into the bank (contra – Cash column credited).

- Bank charges, direct debits, or standing instructions deducted by the bank.

Format Of Double Column Cashbook

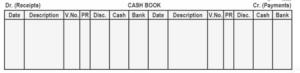

7. What Is A Triple Column Cash Book?

A Triple Column Cash Book (also known as Three Column Cash Book) is an advanced type of Cash Book that extends the Double Column Cash Book by adding two discount columns:

- Discount Allowed (on the credit side – discounts given to debtors for prompt payment).

- Discount Received (on the debit side – discounts received from creditors for early settlement).

It records Cash transactions, Bank transactions, and Cash Discounts in separate columns. This is ideal for businesses with frequent credit sales/purchases involving cash discounts.

Key Features:

- Five amount columns in total: Discount, Cash, and Bank on both debit and credit sides (Discount Received on Dr., Discount Allowed on Cr.).

- Includes contra entries (marked “C”) for transfers between Cash and Bank.

- Discount columns are totalled separately and posted to the ledger (Discount Received A/c credited, Discount Allowed A/c debited).

- No separate Cash, Bank, or Discount accounts in the General Ledger – the Cash Book replaces them.

- Balances: Separate for Cash in Hand and Bank Balance (debit = favourable, credit = overdraft).

Format Of Triple Column Cashbook

8. What Is A Petty Cash Book?

A Petty Cash Book is a separate subsidiary book maintained to record small, routine, and frequent cash payments (petty expenses) such as postage, stationery, tea/coffee, travel fares, cleaning, or minor repairs. These expenses are too numerous and insignificant to record individually in the main Cash Book.

It is managed by a petty cashier (a designated employee) and kept outside the main Cash Book to avoid cluttering the primary records with minor transactions.

Purpose:

- Efficient handling of day-to-day small expenditures.

- Better internal control over minor cash spends.

- Easy analysis and posting of expenses to ledger accounts.

- Reduces workload on the main cashier.

Types of Petty Cash Book:

- Simple Petty Cash Book: Basic format – records only total payments (like a single column book).

- Analytical (Columnar) Petty Cash Book: Most common – has multiple columns for classifying expenses (e.g., Postage, Travel, Stationery) for direct ledger posting. Usually under the Imprest System.

9. What Is The Imprest System In Cash Book?

The Imprest System (also called Fixed Float System) is the most popular and controlled method of managing the Petty Cash Book. Under this system, a fixed amount of cash (called the imprest amount or float) is advanced to the petty cashier at the beginning of a period (e.g., week or month). The petty cashier uses this to pay small expenses, and at the end of the period, the main cashier reimburses exactly the amount spent, restoring the float to its original fixed level.

The petty cashier always starts the next period with the same fixed imprest amount.

How It Works (Step-by-Step):

- Determine Imprest Amount: Based on estimated petty expenses (e.g., ₹5,000 per month).

- Initial Advance: Main cashier gives the float. Entry in Main Cash Book: Debit Petty Cash A/c | Credit Cash/Bank.

- Daily Expenses: Petty cashier pays small expenses and records them in the Petty Cash Book with vouchers (receipts).

- End of Period: Petty cashier submits the book + vouchers. Total expenses calculated (e.g., ₹4,300 spent → ₹700 left).

- Reimbursement: Main cashier pays exactly ₹4,300. Entry in Main Cash Book: Debit various Expense A/cs (from totals) | Credit Cash/Bank.

- Restoration: Float back to ₹5,000 for the next period.

10. What Is A Contra Entry In Cash Book?

A Contra Entry is a special type of entry in the Double Column or Triple Column Cash Book where a transaction affects both the Cash column and the Bank column on opposite sides. It represents an internal transfer of funds between cash and bank (or vice versa) within the same business.

The term “contra” means “opposite” – the amount is recorded on one side in one column and on the opposite side in the other column. These entries are marked with “C” (for Contra) in the Ledger Folio (L.F.) column to indicate they are internal and not posted to any ledger account (as they cancel each other out).

Contra entries appear only in Cash Books with bank columns (Double or Triple Column). They do not appear in Single Column or Petty Cash Books.

Common Examples of Contra Entries:

- Cash deposited into bank: Debit Bank column | Credit Cash column.

- Cash withdrawn from bank for office use: Debit Cash column | Credit Bank column.

- Cheque received but later deposited (rarely contra if direct).

11. How Is Cash Deposited Into Bank Recorded In Double Entry Cash Book?

When cash is deposited into the bank in a Double Column Cash Book, it is recorded as a contra entry. This is because the transaction involves an internal transfer: cash decreases (goes out) while bank balance increases (comes in).

Recording Rule:

- Debit the Bank column (increase in bank balance).

- Credit the Cash column (decrease in cash in hand).

- Write “C” (for Contra) in the L.F. (Ledger Folio) column on both sides.

- Narration: Usually “Cash deposited into bank” or simply “By/To Cash/Bank”.

- No posting to ledger: Since it’s internal, contra entries are not transferred to any ledger account.

12. How Is The Cash Withdrawn From The Bank Recorded?

Cash withdrawn from the bank (usually for office expenses, petty cash, or business use) is recorded as a contra entry in the Double Column or Triple Column Cash Book. This is the reverse of cash deposited into the bank.

Recording Rule:

- Debit the Cash column (cash in hand increases).

- Credit the Bank column (bank balance decreases).

- Mark “C” (for Contra) in the L.F. (Ledger Folio) column on both sides.

- Particulars/Narration: Cross-referenced as “To Bank (C)” on debit side and “By Cash (C)” on credit side, or “Cash withdrawn from bank for office use”.

- No posting to ledger: Contra entries are internal transfers and cancel each other out.

13. What Side Does Cash Receipt Appear In The Cash Book?

Cash receipts always appear on the Debit side (left side) of the Cash Book.

Reason (Based on Accounting Rules):

- Cash is an asset.

- When cash is received (inflow), the asset increases.

- According to the golden rule for asset accounts: Increase on Debit side, Decrease on Credit side.

- Therefore, all cash receipts (e.g., cash sales, cash from debtors, capital introduced, loans received in cash) are recorded on the Debit side.

In Different Types of Cash Books:

- Single Column Cash Book: Debit side → Cash column.

- Double/Triple Column Cash Book:

- If physical cash received → Debit Cash column.

- In case of a cheque received and deposited the same day → Debit Bank column directly.

- If cheque received but kept as cash → Debit Cash column (later contra when deposited).

14. What Side Do Cash Payments Appear On?

Cash payments always appear on the Credit side (right side) of the Cash Book.

Reason (Based on Accounting Rules):

- Cash is an asset.

- When cash is paid (outflow), the asset decreases.

- According to the golden rule for asset accounts: Decrease on Credit side, Increase on Debit side.

- Therefore, all cash payments (e.g., cash purchases, expenses, salaries, creditors paid in cash) are recorded on the Credit side.

In Different Types of Cash Books:

- Single Column Cash Book: Credit side → Cash column.

- Double/Triple Column Cash Book:

- If physical cash paid → Credit Cash column.

- In case of the Issue of the Cheque → Credit Bank column.

- If cash is deposited into the bank (contra) → Credit Cash column.

- If cash is withdrawn from the bank (contra) → Credit Bank column.

15. Does The Cash Book Balance Like Other Ledger Accounts?

Yes, the Cash Book balances exactly like other ledger accounts. This is because of its dual nature – it functions as a ledger account (for cash/bank) while also being a book of original entry.

How Balancing Works (Same as Ledger):

- Totalling: Add up the Debit side and Credit side separately.

- Difference: If Debit total > Credit total → Debit balance (Cash in Hand/Bank favourable – brought down to Debit side as “Balance c/d”).

- If Credit total > Debit total → Credit balance (Bank Overdraft – brought down to Credit side).

- Equalise totals: The balance is added to the shorter side to make both sides equal.

- Next period: The closing balance becomes “Balance b/d” (brought down) as opening.

16. What Is The Difference Between Cash Book & Cash Account?

The Cash Book and Cash Account both deal with cash transactions, but they differ significantly in nature, purpose, maintenance, and role in the accounting system. The key distinction arises because the Cash Book has a dual function (journal + ledger), while the Cash Account is purely a ledger.

| Aspect | Cash Book | Cash Account |

|---|---|---|

| Nature | Subsidiary book – Book of Original Entry (Journal) and Ledger. | Final Account – Only a Ledger Account (T-shaped). |

| Functions | Acts as both journal (chronological recording) and ledger (balance calculation). | Only ledger – receives postings from journal/Cash Book. |

| When Maintained | Always maintained for cash/bank transactions. | Maintained only if no Cash Book is kept (rare in practice). When Cash Book exists, no separate Cash Account is opened. |

| Recording | Transactions recorded immediately with narration, debit/credit sides, and columns (single/double/triple). | Transactions posted from journal (summary or individual) – no narration or chronology. |

| Balance | Real-time balance available daily/periodically. Directly used in Trial Balance. | Balance available only after postings – delayed. |

| Posting Ledger | Other sides posted to respective ledgers; Cash Book itself replaces Cash/Bank ledger. Contra entries not posted. | All entries come from journal – both sides affect other accounts. |

| Types / columns | Single, Double, Triple Column, Petty Cash – flexible. | Simple T-account – no columns. |

17. Why Are Bank Charges Recorded In Cash Books?

Bank charges (e.g., service fees, transaction fees, overdraft interest, cheque book charges) are recorded in the Cash Book (specifically in the Bank column on the Credit side) because they are deducted directly by the bank from the account holder’s balance. These charges appear first in the Bank Statement (Pass Book), but the business may not be aware of them immediately.

Reasons for Recording in Cash Book:

- Timing Difference: Bank debits charges automatically (e.g., monthly fees), but the business learns about them only when receiving the bank statement. To update the books accurately, charges are entered when discovered.

- Reconciliation Requirement: Recording ensures the Cash Book bank balance matches the Bank Statement balance after adjustments in the Bank Reconciliation Statement (BRS).

- Accuracy of Records: Bank charges are an expense (reduce bank balance). Not recording them would overstate the bank balance in the books.

- Compliance with Double-Entry: Debit Bank Charges Expense A/c (or directly to P&L) | Credit Bank column in Cash Book.

- Control and Audit: Proper recording prevents discrepancies and aids in expense tracking.

Few related topics for your knowledge

- Job Guarantee Vs Job Assistance: Core Points Of Differences Between The Two

- 10 Life Changing Simulation Softwares To Learn In Upcoming Years

- Top 20 Journal Entries Questions And Answers For Interview

- 15 Essential Inventory Valuation Questions & Answers For Interview

- 25 Important BRS Questions For Interview Preparation

18. What Is The Overdraft In Cash Book?

An Overdraft in the Cash Book occurs when the **Bank column shows a Credit balance at the end of a period. This means the business has withdrawn more money from the bank than it had deposited, resulting in the bank allowing a temporary negative balance (i.e., the business owes money to the bank).

In simple terms:

Bank Overdraft = Payments via bank > Receipts in bank → Bank balance becomes negative.

Key Features:

- Appears in Double Column or Triple Column Cash Book (in the Bank column only).

- Shown as a Credit balance after balancing the Bank column.

- Treated as a short-term liability in the Balance Sheet (under Current Liabilities).

- Banks usually charge interest on overdraft, which is recorded separately (Credit Bank column when known).

19. How Is Discount Allowed Recorded In Triple Column Cash Book?

Discount Allowed (cash discount given to debtors/customers for prompt or early payment) is recorded in the Triple Column Cash Book on the Credit side in the dedicated Discount Allowed column.

Reason:

- Discount Allowed is an expense for the business (loss of revenue).

- When a debtor pays less than the full amount due to discount, the discount portion is credited in the Discount column.

- The actual cash/cheque received is recorded in the Cash or Bank column on the Debit side.

- This follows double-entry: Full amount credited to Debtor’s A/c in ledger, but only net received in Cash/Bank + Discount Allowed.

Recording Rule:

- Debit side (Receipts): Record the net amount received in Cash or Bank column + Discount Received (if any) in its column.

- Credit side (Payments): Not directly; but when paying creditors and receiving discount → Debit side Discount Received.

- For Discount Allowed: Always on the Credit side Discount column (when receiving payment from debtors).

- Totals: Discount Allowed column totalled at end → Posted to Debit of Discount Allowed A/c in ledger (as expense).

20. How Is Discount Received Recorded?

Discount Received (cash discount obtained from creditors/suppliers for making prompt or early payment) is recorded in the Triple Column Cash Book on the Debit side in the dedicated Discount Received column.

Reason:

- Discount Received is an income (or gain) for the business (reduces the cost of purchases).

- When paying a creditor less than the full amount due to discount, the discount portion is debited in the Discount column.

- The actual cash/cheque paid is recorded in the Cash or Bank column on the Credit side.

- This follows double-entry: Full amount debited to Creditor’s A/c in ledger, but only net paid in Cash/Bank + Discount Received.

Recording Rule:

- Debit side (Receipts): Discount Received column (when paying creditors and receiving discount).

- Credit side (Payments): Record the net amount paid in Cash or Bank column + Discount Allowed (if any) in its column.

- Totals: Discount Received column totalled at end → Posted to Credit of Discount Received A/c in ledger (as income).

21. Are Contra Entries Posted To The Ledger?

No, contra entries are NOT posted to the ledger.

Reason:

Contra entries represent internal transfers between Cash and Bank columns within the same business (e.g., cash deposited into bank or cash withdrawn from bank). Since the transaction affects two parts of the same asset (Cash + Bank = Total Liquid Funds), there is no change in the overall financial position and no external party is involved.

Posting them to the ledger would result in unnecessary duplication:

- Debiting one (e.g., Bank A/c) and crediting the other (Cash A/c) would cancel out.

- But since the Cash Book itself serves as the ledger for Cash and Bank, separate ledger accounts are not maintained.

Thus, contra entries complete the double-entry within the Cash Book itself.

22. What Is The Purpose Of A Petty Cashbook?

The Petty Cash Book is maintained for the following key purposes:

- To record small, frequent, and routine expenses efficiently: Businesses incur numerous minor expenditures daily (e.g., postage stamps, tea/coffee, stationery, travel fares, cleaning supplies). Recording each individually in the main Cash Book would make it cluttered and time-consuming.

- To avoid overloading the main Cash Book: By handling petty transactions separately, the primary Cash Book remains clean and focused on significant cash/bank transactions.

- Delegate responsibility with control: A petty cashier is appointed to manage small payments, reducing the burden on the main cashier while maintaining accountability (especially under the Imprest System).

- To provide better control and prevent misuse: Fixed float (imprest), voucher requirements, and periodic reimbursement ensure expenses are authorised, supported, and verified.

- Facilitate easy classification and posting: An analytical format with expense columns (e.g., Postage, Conveyance) allows for direct totaling and posting to respective ledger accounts.

- To enable quick reimbursement and audit: Supports timely restoration of float and easy checking with vouchers/receipts.

23. What Happens If The Petty Cash Expenses Exceed The Imprest Amount?

In the Imprest System, the petty cashier is given a fixed float (imprest amount, e.g., ₹5,000). The system is designed so that expenses should not normally exceed the imprest amount before reimbursement. However, if petty cash expenses do exceed the imprest amount, the following happens:

Practical Situation:

- The petty cashier continues to make payments even after the float is exhausted (e.g., imprest ₹5,000, but expenses reach ₹5,800).

- This results in a negative balance or shortage in the Petty Cash Book (cash in hand becomes negative, which is practically not possible with physical cash, but recorded to reflect reality).

Treatment and Consequences:

- Immediate Action:

- The petty cashier cannot make further payments without additional cash.

- He/she must immediately inform the main cashier and request advance reimbursement or extra funds.

- Reimbursement Process:

- Reimbursement is still made only for the actual expenses incurred (supported by vouchers), not exceeding the spent amount.

- Example: Imprest ₹5,000 | Expenses ₹5,800 → Reimbursed ₹5,800 → Float restored to ₹5,000 (excess ₹800 effectively settled).

- No extra amount is given just because expenses exceeded; the imprest remains fixed.

- Accounting Entries:

- Main Cash Book: Debit various Expense A/cs ₹5,800 | Credit Bank/Cash ₹5,800.

- Petty Cash Book: Updated with reimbursement; balance back to ₹5,000.

- Management Review:

- Exceeding the imprest is a red flag indicating the float is inadequate for current needs.

- Management may increase the imprest amount permanently (e.g., from ₹5,000 to ₹7,000) after review.

- If frequent, it suggests poor estimation or uncontrolled spending → investigation needed.

- If Due to Error or Misuse:

- Shortage may be treated as loss or recovered from the petty cashier.

24. How Is Reimbursement Recorded In Petty Cash Book?

In the Petty Cash Book (under the Imprest System), reimbursement itself is not recorded in the Petty Cash Book. Instead, it is recorded in the Main Cash Book (or General Journal) because the reimbursement involves transferring funds from the main cashier/bank to the petty cashier.

The Petty Cash Book only records the expenses paid and the remaining balance. The reimbursement simply restores the imprest float and is noted indirectly by increasing the cash in hand back to the original amount.

Step-by-Step Process:

- At the end of the period (week/month):

- Petty cashier totals the expenses in the Petty Cash Book.

- Calculates amount spent (e.g., ₹4,500 out of ₹5,000 imprest → ₹500 left).

- Submits book + vouchers to main cashier.

- Reimbursement Amount: Exactly the amount spent (₹4,500 in example) – to restore imprest to ₹5,000.

- Recording:

- In Main Cash Book (or Cash/Bank Column):

- Debit various Expense Accounts (from analytical column totals: e.g., Postage ₹800, Stationery ₹1,200, Travel ₹2,500).

- Credit Cash/Bank (source of reimbursement).

- In Petty Cash Book:

- No direct entry for reimbursement.

- The petty cashier simply receives the cash/cheque and the balance is restored (noted as cash received, but usually just updated in the “Receipts” column on the left side).

- In Main Cash Book (or Cash/Bank Column):

25. What Is An Analytical Petty Cash Book?

An Analytical Petty Cash Book (also called Columnar Petty Cash Book) is the most commonly used format of Petty Cash Book under the Imprest System. It has multiple analysis columns on the payment (credit) side for classifying different types of petty expenses (e.g., Postage, Stationery, Travel, Cleaning, Conveyance). This allows easy totalling of each expense head for direct posting to the respective ledger accounts.

Unlike a Simple Petty Cash Book (which has only one total payment column), the analytical version provides detailed classification without needing a separate subsidiary book.

Key Features:

- Left Side (Debit/Receipts): Records cash received (initial imprest + reimbursements).

- Right Side (Credit/Payments): Columns for Date, Particulars, Voucher No., Total Payments, and separate columns for expense categories.

- Each payment is entered in the Total column and also in the relevant expense column.

- At period end: Horizontal totals for each expense → Posted to ledger.

- Supports vouchers for every payment.

26. Give An Example Of Contra Entry?

A contra entry is an internal transfer between Cash and Bank columns in a Double Column or Triple Column Cash Book. It appears on opposite sides and is marked “C” in the L.F. column (no ledger posting).

Common Examples:

- Cash deposited into bank

- Cash withdrawn from bank for office use

Detailed Example : Cash Deposited into Bank

On January 10, 2026, ₹25,000 cash was deposited into the bank.

- Effect: Cash decreases ₹25,000 | Bank increases ₹25,000.

- Marked “C” → No posting to ledger.

27. If a cheque is received and deposited on the same day, how is it recorded?

If a cheque is received from a customer/debtor and deposited into the bank on the same day, it is recorded directly in the Bank column on the Debit side of the Double Column or Triple Column Cash Book.

Reason:

- The cheque never becomes cash in hand – it goes straight to the bank.

- No physical cash is handled, so no entry in the Cash column.

- This avoids unnecessary steps (no contra entry needed).

Recording Rule:

- Debit side → Bank column with the full amount.

- Particulars: “To Debtor’s A/c” or “To [Party Name]”.

- Posting: The debtor’s account in the ledger is credited with the full amount.

- If discount is involved (in Triple Column), net amount in Bank + discount in relevant column.

28. If A Cheque Is Received But Not Deposited Immediately?

If a cheque is received from a customer/debtor but not deposited into the bank immediately (i.e., kept as cash for some time), it is initially treated as cash in hand. Therefore, it is recorded in two steps in the Double Column or Triple Column Cash Book.

Step-by-Step Recording:

- On the date of receipt:

- Record the cheque as a cash receipt.

- Debit the Cash column (since the cheque is physically held like cash).

- No entry in Bank column yet.

- On the date of deposit (later date):

- When the cheque is finally deposited into the bank, make a contra entry:

- Debit Bank column.

- Credit Cash column.

- Mark “C” in L.F. column on both sides.

- When the cheque is finally deposited into the bank, make a contra entry:

This accurately reflects that the funds were temporarily in hand before moving to the bank.

29. What Is A Bank Reconciliation Statement?

A Bank Reconciliation Statement (BRS) is a financial statement prepared periodically (usually monthly) to reconcile (match and explain differences between) the bank balance as per the Cash Book (business records) and the bank balance as per the Bank Statement (Pass Book provided by the bank).

It is not a ledger account or part of double-entry – it is a working statement to identify and rectify discrepancies, ensuring the accuracy of the bank’s records in the books.

Purpose of BRS:

- Detect errors (in Cash Book or bank statement).

- Identify timing differences (items recorded in one but not the other).

- Uncover fraud or omissions.

- Update the Cash Book for unrecorded items (e.g., bank charges).

- Ensure true bank position for financial reporting.

30. What Is The Difference Between Cash Book & Pass Book?

The Cash Book and Pass Book (Bank Statement) both record bank transactions, but from different perspectives. The Cash Book is maintained by the business/account holder, while the Pass Book/Bank Statement is maintained by the bank. Differences arise due to timing, recording practices, and purpose.

| Aspect | Cash Book | Pass book |

|---|---|---|

| Maintained By | Business / Account holder | Bank |

| Perspective | Records transactions from business viewpoint | Records transactions from bank viewpoint |

| Nature | Part of double-entry system (subsidiary book) | Independent record issued by bank |

| Recording Timing

Cheques Issued |

Transactions recorded on the date they are entered in books (e.g., cheque issued date) | Transactions recorded on the date they are cleared/processed by bank |

| Cheques Deposited | Credited on date of issue | Credited only when presented and cleared |

31. How Are Direct Deposits By Customers Are Recorded In Cash Book?

Direct deposits by customers (also called direct bank credits or electronic transfers) occur when a customer/debtor transfers money directly into the business’s bank account (e.g., via NEFT, RTGS, UPI, or online payment) without issuing a cheque to the business.

These are not known to the business immediately – they are first recorded by the bank in the Bank Statement. When the business receives the bank statement (or alert), the amount is recorded in the Cash Book.

Recording Rule:

- Debit the Bank column (increase in bank balance) on the Debit side.

- Particulars: “To [Customer’s Name] A/c” or “To Sundries (as per bank statement)” or “To Direct Deposit by Customer”.

- No entry in Cash column (since no physical cash handled).

- Posting: Credit the Customer’s/Debtor’s A/c in the ledger with the amount (reducing receivable).

- This is similar to other unrecorded bank items (e.g., interest credited).

32. What Is Trade Discount Vs Cash Discount?

Trade discounts and cash discounts are both reductions offered by sellers to buyers, but they serve different purposes, are applied at different stages, and are treated differently in accounting.

| Key Aspects | Trade Discount | Cash Discount |

|---|---|---|

| Purpose | To encourage bulk purchases, large orders, or sales to resellers/wholesalers. | To encourage prompt or early payment of invoices (improves seller’s cash flow). |

| Timing | Applied at the time of sale/purchase (deducted from list/catalog price). | Applied at the time of payment (if paid within specified early period). |

| Calculation Base | On the list price or catalog price. | On the invoice price (after any trade discount). |

| Accounting Treatment | Not recorded separately; only the net amount (after discount) is entered in books. | Recorded separately as an expense (for seller) or income (for buyer). |

| Typical Recipients | Often wholesalers, retailers, or bulk buyers in B2B transactions. | Any buyer (retail or wholesale) who pays early. |

| Common Terms | Percentage off list price (e.g., 20% for bulk orders). | Terms like “2/10 net 30” (2% off if paid in 10 days, full amount due in 30 days). |

33. Is Petty Cash An Asset Or Expense?

Petty Cash is an Asset, not an expense.

- Nature and Classification:

- Petty cash refers to a small amount of cash (e.g., Rs100–Rs500) kept on hand by a business to cover minor, incidental expenses like office supplies, postage, or small repairs. These are transactions too small for checks or digital payments.

- In accounting (under double-entry systems like GAAP or IFRS), the petty cash fund—the imprest amount set aside—is recorded as a current asset on the balance sheet. Specifically, it’s classified under “Cash and Cash Equivalents” because it’s highly liquid and intended for short-term use.

- It is not an expense. The fund itself is a fixed pool of money replenished periodically to its original amount.

- Why Not an Expense?

- Expenses arise from replenishing the petty cash when actual expenditures are vouched (e.g., receipts submitted). At replenishment:

- Cash is debited to expense accounts (e.g., “Office Supplies Expense,” “Postage Expense”).

- The petty cash account remains unchanged (back to imprest balance).

- Expenses arise from replenishing the petty cash when actual expenditures are vouched (e.g., receipts submitted). At replenishment:

34. How Often Is The Petty Cash Book Balanced?

The petty cash book is typically balanced (reconciled) monthly under the imprest system, which is the most common method for managing petty cash.

Key Details on Frequency

- Standard Best Practice: Reconciliation occurs at least monthly. This involves:

- Counting the remaining cash on hand.

- Adding up supported vouchers/receipts.

- Ensuring the total equals the fixed imprest amount (e.g., ₹5,000).

- Replenishing the fund to its original level if low, while recording expenses in the main ledger.

- Why Monthly?

- Prevents discrepancies, errors, or fraud from accumulating.

- Aligns with monthly financial closing and reporting cycles.

- Supported by accounting standards (GAAP, IFRS, Ind AS) and institutional guidelines (e.g., universities, government bodies require “at least monthly”).

35. What If The Cash Sales Are Directly Deposited Into Bank?

When cash sales (sales made for immediate cash payment) are directly deposited into the bank (instead of first bringing cash to the office and then depositing), it changes the accounting treatment slightly. The key principle: Cash sales are still recorded as sales, but the cash skips the “Cash in Hand” stage and goes straight to the “Bank” account.

36. Explain The Ruling Of A Simple Cash Book?

A Simple Cash Book is the simplest form of cash book that records only cash transactions (receipts and payments). It does not have a bank column or discount columns. This functions like a Cash Account in the ledger but is maintained in a book format with separate columns for dates, details, and amounts.

It is typically used by very small businesses, sole proprietors, or organisations where most transactions are in cash and banking is minimal.

Standard Ruling (Format) of a Simple Cash Book

The Simple Cash Book is ruled with two sides (like a T-account):

- Left Side (Debit Side) → Records Cash Receipts (money coming in)

- Right Side (Credit Side) → Records Cash Payments (money going out)

37. Why Is No Separate Cash Account Maintained In Ledger When Cash Book Exists?

In the double-entry bookkeeping system, every transaction affects two accounts, and normally, a Cash Account is maintained in the general ledger to record all cash receipts and payments.

However, when a Cash Book (Simple, Double-Column, or Triple-Column) is maintained, no separate Cash Account is opened in the ledger.

Reason: The Cash Book Itself Serves as the Cash Account

- The Cash Book is a book of original entry (subsidiary book) as well as a ledger account.

- It follows the exact same double-entry principle as a ledger account:

- Debit side records cash receipts (increases in cash).

- Credit side records cash payments (decreases in cash).

- Therefore, the Cash Book replaces the need for a separate Cash Account in the main ledger.

- Posting cash transactions twice (once in Cash Book and again in a ledger Cash A/c) would result in duplication and violate double-entry rules.

38. What Is A Favourable Balance In Cash Book?

A favourable balance in the Cash Book means a positive cash balance – i.e., the business has cash in hand (or in bank, depending on the type of Cash Book) at the end of the period.

In simple terms:

- Cash receipts (debit side) exceed cash payments (credit side).

- The closing balance appears on the debit side of the Cash Book.

39. What Is An Unfavourable Balance?

An unfavourable balance in the Cash Book means a negative cash position – i.e., cash payments exceed cash receipts during the period.

In simple terms:

- More money has gone out than come in.

- The closing balance appears on the credit side of the Cash Book.

40. How Is A Dishonored Cheque Recorded In Cash Book?

A dishonoured cheque (also called a bounced cheque) occurs when a cheque previously received from a customer (debtor) and deposited into the bank is returned unpaid by the bank (e.g., due to insufficient funds, stop payment, etc.).

In accounting, the original entry treated the cheque as cash received, but upon dishonour, we must reverse that receipt. This is one of the crucial cash book questions.

The recording depends on who issued the cheque and which type of Cash Book is used.

41. What Are The Advantages Of Maintaining A Cash Book?

- Maintaining a Cash Book provides numerous benefits to businesses, especially in ensuring accurate tracking and control of cash transactions. Below is a clear explanation of the key advantages:

- Complete and Chronological Record: The Cash Book records all cash receipts and payments in one place in the order they occur. This gives a full, systematic history of cash movements, making it easy to trace any transaction.

- Daily Cash Position Visibility: By balancing the Cash Book regularly (daily or periodically), the business owner or accountant can know the exact cash in hand or bank balance at any time. This helps in monitoring liquidity instantly.

- Prevention of Fraud and Errors: Regular entry and balancing act as an internal control mechanism. Discrepancies can be spotted quickly, reducing the chances of theft, misappropriation, or mistakes by employees handling cash.

- Saving of Time and Effort: Since the Cash Book itself serves as the Cash Account in the ledger, there is no need to maintain a separate Cash Account in the general ledger. This avoids duplication of work and reduces clerical effort.

- Quick Detection of Mistakes: Errors in recording receipts or payments are identified early during balancing, allowing prompt correction before they affect final accounts.

- Better Cash Management: It helps in planning cash flows, avoiding unnecessary overdrafts, and ensuring funds are available for day-to-day expenses, investments, or emergencies.

42. Can Interest Credited By Bank Be Recorded Directly In Cash Book?

Yes, interest credited by the bank can and should be recorded directly in the Cash Book (specifically in the bank column of a Two-Column or Three-Column Cash Book).

Reason

- Interest credited by the bank increases the bank’s balance in our account.

- This information usually comes from the bank statement or passbook, not from an immediate intimation.

- Since the Cash Book maintains the bank balance from the business’s perspective, adjustments like bank interest (which we did not record earlier) are entered directly into the Cash Book during bank reconciliation or when updating the Cash Book from the passbook.

How It Is Recorded

- Entered on the Debit side in the Bank column.

- Particulars: “To Interest A/c” or “To Bank Interest A/c”.

43. What Is The Treatment Of Post Dated Cheques In Cash Book?

Post-dated cheques (PDCs) are cheques dated in the future (e.g., cheque dated 15 Feb 2026 received on 4 Jan 2026). They are not yet encashable by the bank on the date of receipt.

Key Principle

- Not recorded in Cash Book (neither Cash nor Bank column) on the date of receipt.

- Reason: No immediate cash/bank impact. Cash Book records actual cash receipts/payments or bankable transactions only.

- Treated as a conditional asset/receivable until the date arrives.

44. How Is Petty Cash Float Initially Recorded?

The petty cash float (also called the imprest amount) is the fixed sum of cash set aside for small, day-to-day expenses. It is established using the imprest system, where a specific amount is given to the petty cashier, and the fund is replenished only for the amount spent.

Key Points

- Petty Cash A/c is a Current Asset account in the ledger (grouped under “Cash and Cash Equivalents”).

- Payment is usually made by cheque (from Bank A/c) for better control, but can be from Cash A/c if physical cash is handed over.

- The amount (e.g., ₹5,000) becomes the fixed float/imprest level.

45. What Is The Role Of Vouchers In A Petty Cash Book?

Vouchers are the supporting documents (receipts, bills, invoices, slips, or memos) that provide evidence for every petty cash payment. They play a critical and indispensable role in the Petty Cash Book under the imprest system.

Key Roles of Vouchers

- Proof of Payment Vouchers serve as documentary evidence that the expense was actually incurred and cash was paid for a legitimate business purpose. Without a voucher, no payment should be recorded.

- Basis for Recording Entries Each payment entry in the Petty Cash Book is made only against a voucher. The petty cashier records:

- Date

- Voucher number

- Particulars (nature of expense)

- Amount

- Expense head (e.g., stationery, postage, tea/coffee)

- Facilitates Classification of Expenses Vouchers help analyse and distribute expenses to correct heads (e.g., Travel, Printing, Repairs) when preparing the summary for replenishment.

- Internal Control and Fraud Prevention Requiring vouchers prevents misuse of petty cash. The petty cashier must obtain a signed voucher or receipt from the recipient or attach external bills. Surprise checks compare vouchers with recorded entries.

- Essential for Replenishment When the petty cash float is replenished:

- All vouchers are totalled.

- Expenses are posted to respective ledger accounts.

- Replenishment cheque is drawn for the exact amount spent (supported by vouchers).

- Audit Trail and Compliance Vouchers provide a clear audit trail. Auditors verify entries by examining attached vouchers. They are mandatory for tax audits (Income Tax, GST in India) and compliance under Companies Act.

46. If Petty Cash Is Lost, How Is It Treated?

If petty cash (cash from the imprest fund) is lost (e.g., due to theft, misplacement, or any reason without supporting vouchers), it is treated as a loss to the business. The imprest balance must still be maintained, but the missing amount is written off as an expense.

47. What Is The Difference Between Cash & Bank Reconciliation?

| Aspect | Cash Reconciliation (Cash in Hand) | Bank Reconciliation (Bank Balance) |

|---|---|---|

| What It Reconciles | Balance in Cash Book (Cash column) vs. Physical cash on hand | Balance in Cash Book (Bank column) vs. Bank Statement/Passbook |

| Purpose | Verify no shortage/theft/misplacement of physical currency/notes/coins | Identify timing differences, errors, or unrecorded items between business books and bank records |

| Frequency | Often daily or weekly (especially in cash-heavy businesses like retail shops) | Usually monthly (when bank statement arrives) |

| Common Causes of Differences | – Counting errors – Theft or loss – Unrecorded petty expenses – Over/short in collections | – Cheques issued but not presented – Cheques deposited but not cleared – Bank charges/interest not recorded – Direct credits/debits by bank – Errors by bank or business |

| Document Used | Physical count sheet + Petty Cash Book (if separate) | Bank Statement or Passbook |

| Who Performs It | Petty cashier or owner (surprise checks recommended) | Accountant (using Cash Book bank column) |

48. How Are Standing Instructions Recorded in the Cash Book?

Standing instructions (also called standing orders) are automatic payment authorizations given to the bank (e.g., regular monthly rent, insurance premium, loan EMI, subscription fees). The bank debits the business’s account periodically without further intimation each time.

These are not initiated by the business on the specific date, so they are usually not known in advance when updating the Cash Book daily. They are discovered when the bank statement or passbook is received.

Treatment in Cash Book

- No entry on the date of instruction setup (just noted for reference).

- Recorded only when discovered (typically during bank reconciliation or passbook update).

- Entered directly in the Cash Book on the credit side of the bank column (as it reduces bank balance).

49. Why Is Petty Cash Not The Part Of The Main Cash Book?

Petty cash is managed separately from the main Cash Book due to differences in transaction nature, control needs, and efficiency. Here’s a detailed explanation:

- Different Nature of Transactions: The main Cash Book records significant cash receipts and payments, such as sales collections, major purchases, salaries, or capital introductions. Petty cash handles numerous small, frequent, and miscellaneous expenses like stationery, postage, tea for staff, or minor repairs. Including every tiny petty transaction in the main Cash Book would make it excessively bulky, cluttered, and difficult to manage.

- Imprest System Requirement: Petty cash operates under the imprest system, where a fixed float (e.g., ₹5,000) is advanced to a petty cashier. Daily expenses are recorded only in a separate Petty Cash Book with analytical columns (e.g., for postage, travel, stationery). The main Cash Book only reflects the initial advance and periodic lump-sum replenishments, not individual items. Mixing them would disrupt this fixed-float mechanism.

- Better Internal Control and Accountability: Petty cash is entrusted to a dedicated petty cashier, who maintains the separate Petty Cash Book with vouchers for every payment. This segregation of duties prevents fraud, enables surprise physical checks, and assigns clear responsibility. Combining it with the main Cash Book (handled by a different person) would weaken these controls.

- Simplifies Balancing and Reconciliation: The main Cash Book is balanced daily or frequently to track overall cash position. Petty Cash Book is reconciled periodically (e.g., monthly) against vouchers. Separation avoids constant minor adjustments in the main book, keeping it focused on high-value items and easier to reconcile with bank deposits.

50. In an interview, how would you explain the importance of accurate Cash Book maintenance?

The Cash Book is one of the most fundamental books in accounting because it records all cash and bank transactions — both receipts and payments — on a day-to-day basis. Maintaining it accurately is extremely important for several reasons:

- Reflects True Liquidity Position: The Cash Book shows the exact cash in hand and bank balance at any point in time. Accurate maintenance ensures management knows the real available funds for meeting daily obligations, avoiding overdrafts, or making timely decisions.

- Enables Effective Cash Management: Businesses, especially small and medium ones, rely heavily on cash flow. An accurate Cash Book helps in planning payments, controlling unnecessary expenses, and preventing cash shortages or idle funds.

- Internal Control and Fraud Prevention: Regular and accurate recording, along with daily or periodic balancing, acts as a strong internal check. It reduces the risk of misappropriation, theft, or errors by employees handling cash. Discrepancies can be detected early.

- Facilitates Bank Reconciliation: The bank column in the Cash Book is directly used to prepare the Bank Reconciliation Statement. If the Cash Book is inaccurate, reconciliation becomes difficult, and differences (like unpresented cheques, bank charges, or direct credits) may go unnoticed. It is a crucial cash book questions to remember.

Final Takeaway

Hence, these are some of the crucial Cash book questions that you must be well aware off. You cannot just make your choices in the dark. Here, you need to identify the correct solution that can assist you in meeting your goals with complete ease.

You can share your views and opinions in our comment box this will help us to know your take on this matter. Here application of correct strategy can make things easier for you to crack the interview with ease.

- You’re Smart Enough, But English Is Holding You Back. A Fluent English Speaking Course Can Fix That - July 3, 2026

- Movement Types in SAP MM: What They Are, Why They Matter, and How to Master Them - June 26, 2026

- No Experience? No Problem. Here’s How Freshers Are Landing SAP FICO Jobs in India Right Now - June 19, 2026