.jpg)

Rectification Of Errors In Accounting: Key Types & Methods

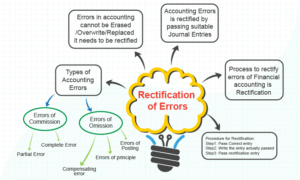

Rectification of errors in accounting is a crucial accounting process that involves identifying and correcting mistakes in financial records to ensure accuracy and reliability. Errors may arise from omissions, miscalculations, misinterpretations, or clerical oversights, impacting financial statements.

These errors can be classified as errors of omission, commission, principle, or compensating errors. Rectification involves analyzing trial balances, ledgers, and journals to pinpoint discrepancies, followed by passing corrective journal entries.

This process ensures compliance with accounting standards, maintains stakeholder trust, and supports informed decision-making. Timely rectification prevents misstatements, enhances financial transparency, and upholds the integrity of an organization’s financial reporting system.

Table of Contents

What Is Rectification Of Errors In Accounting?

Rectification of errors in accounting is the process of identifying and correcting mistakes in financial records to ensure accurate financial reporting. Errors can occur due to omissions, miscalculations, incorrect postings, or misapplication of accounting principles.

These are classified as errors of omission (transactions missed), commission (incorrect entries), principle (violating accounting rules), or compensating errors (offsetting mistakes). Rectification involves detecting errors through trial balance discrepancies or ledger reviews and correcting them by passing appropriate journal entries.

This ensures financial statements reflect true financial positions, maintain compliance with accounting standards, and support reliable decision-making while upholding transparency and trust.

Key Types Of Errors In Accounting

There are some common mistakes that accountants often make while recording the books of accounts. Some of these key errors in accounting that they make are as follows:-

- Errors of Omission: Transactions completely missed or not recorded, e.g., a sale not entered in the books.

- Commission Errors : Incorrect entries, such as wrong amounts or accounts, e.g., recording Rs 500 instead of Rs 5,000.

- Errors of Principle: Misapplication of accounting principles, like treating a capital expense as revenue, e.g., recording asset purchase as an expense.

- Compensating Errors: Errors that offset each other, e.g., overstating one account and understating another by the same amount.

- Errors of Original Entry: Incorrect original transaction amount, e.g., entering $1,000 instead of $100.

- Errors of Reversal: Recording entries in the wrong direction, e.g., debiting instead of crediting an account.

Methods Of Rectification Of Errors

There are several methods of rectification of errors in accounting that you must be well aware of while meeting your requirements with ease. In this article you will get to know about different methods for rectifying the errors.

1.Rectification Of Errors Before Preparation Of Trial Balance

Errors identified before the trial balance is prepared are corrected directly in the books of accounts. These errors typically do not affect the trial balance because they are caught early.

- Method: Direct Correction in the Ledger

- Single-Sided Errors: Errors affecting only one account (e.g., wrong amount recorded in a single ledger). Correct by making an additional entry or striking out the incorrect entry and posting the correct one.

- Example:- If a purchase of Rs 500 is in record as Rs 50 in the Purchases Account, pass a corrective entry:

Purchase A/c ——————— Dr Rs 450

To Cash / Bank A/c ———————————- Cr Rs 450

Two-Sided Errors: Errors affecting both debit and credit sides (e.g., posting to the wrong account). Reverse the incorrect entry and post the correct one.

- Example:- If a payment of Rs 200 to a creditor is in record of debit to the Sales Account instead of the Creditor’s Account, pass:

Creditors A/c ———————————– Dr Rs 200

To Sales A/c————————————————————-Cr Rs 200

Steps:

- Identify the error in the ledger or subsidiary books.

- Determine the correct account and amount.

- Pass a corrective journal entry or adjust the ledger directly.

Get a BBA Degree with Paid Intership1-year paid internship + 10 Simulation Software + 4 Certifications to land high-paying roles |

|

| BBA in accounting and finance |

2. Rectification Of Errors After Preparation Of Trial Balance

Errors discovered after preparing the trial balance may or may not affect the trial balance. These corrections you can do using specific methods depending on the nature of the error.

a) Errors Not Affecting The Trial Balance

These errors do not cause a mismatch in the trial balance because both debit and credit sides are equally affected. Examples include errors of omission, commission, principle, or compensating errors.

Method Of Journal Entry Correction

Pass a corrective journal entry to nullify the effect of the error and record the correct transaction.

Examples

- Errors of omission

A transaction omitted entirely (e.g., a sale of Rs 1,000 not recorded). Correct by:

Cash / Debtors A/c ——————— Dr Rs 1000

To Sales A/c ——————————————— Cr Rs 1000

- Errors Of Commission

Wrong account or amount recorded (e.g., payment to Supplier A recorded as payment to Supplier B). Correct by:

Supplier A A/c ———————- Dr Rs 500

To Supplier B A/c ————————————- Cr Rs 500

- Errors Of Principal

Recording a transaction against accounting principles (e.g., treating capital expenditure as revenue expenditure). Correct by:

Asset A/c ————————— Dr Rs 5000

To Expense A/c —————————– Cr Rs 5000

- Compensating Errors

Errors that offset each other (e.g., overstating sales by Rs 100 and understating purchases by Rs 100). Correct both entries individually.

b) Errors That Affects The Trial Balance

These errors cause a mismatch in the trial balance (e.g., one-sided errors like posting only the debit or credit side of a transaction). The correction is done using a Suspense Account.

3. Rectification Through Adjusting Entries

Some errors are corrected by making adjusting entries at the end of the accounting period, especially when preparing final accounts.

- Method: Adjusting Entries in Final Accounts

- Errors affecting nominal accounts (e.g., revenue or expenses) may impact the profit and loss account or balance sheet. These corrections are by adjusting the final accounts.

- Example: If depreciation of Rs 500 was not recorded, adjust by

Depreciation Expense A/c ——————————————– Dr Rs 500

Accumulated Depreciation A/c ———————————————————— Cr Rs 500

All these adjustments reflect in the profit and loss account or balance sheet.

4. Rectification Through Subsequent Accounting Periods

Errors discovered in the next accounting period (after final accounts are prepared) are corrected through the profit and loss adjustment account or directly in the affected accounts.

- Method: Profit and Loss Adjustment Account

- Create a profit and loss adjustment account to record corrections for errors affecting nominal accounts (e.g., revenue or expenses) from the prior period.

- Transfer the net effect to the capital account or retained earnings.

- Example: If sales of Rs 1,000 were overstated in the previous year, correct by:

Sales A/c ——————————– Dr Rs 1000

To Profit & Loss A/c ——————————- Cr Rs 1000

5. Rectification Through Reversal & Restatement

For significant errors affecting prior period financial statements, rectification may involve reversing incorrect entries and restating the financial statements.

- Method: Reversal Entries and Restatement

- Reverse the incorrect entry by passing a journal entry to nullify its effect.

- Record the correct entry.

- If the error is material, restate the prior period’s financial statements to reflect the correction.

- Example: If an asset was overstated by Rs 10,000 due to a recording error, reverse it:

Asset A/c ————————– Dr Rs 10,000

To Retained Earnings A/c —————————– Cr Rs 10000

Importance Of Rectification Of Errors

There are several Importance of rectification of errors in accounting that you must be well aware of. So, let’s explore the importance of the the rectification of the errors that you should be well accustomed with are as follows:-

1. Ensures Accuracy Of Financial Records

Correcting errors ensures that the books of accounts reflect the true and fair financial position of the business. Accurate records are essential for reliable financial reporting and compliance with accounting standards.

2. Facilitates The Correct Results

Financial statements guide management, investors, and creditors in making informed decisions. Errors in accounts can lead to wrong conclusions about profitability, liquidity, or solvency, potentially resulting in poor strategic choices. Rectification ensures decisions are based on accurate data.

3. Maintains Compliance With Legal & Regulatory Requirements

Businesses are required to adhere to accounting standards (e.g., GAAP, IFRS) and legal regulations. Uncorrected errors can lead to non-compliance, penalties, or legal issues. Rectification ensures alignment with regulatory frameworks.

4. Prevents Financial Misstatements

Errors can misstate profits, losses, assets, or liabilities, misleading stakeholders about the company’s performance. Rectifying errors prevents financial misstatements and maintains the integrity of financial reports.

5. Builds Trust With Stakeholders

Accurate financial statements enhance the confidence of investors, creditors, auditors, and other stakeholders. Timely rectification of errors demonstrates transparency and accountability, fostering trust in the business.

6. Avoids Cumulative Impacts Of Errors

Small errors, if not corrected, can accumulate over time, leading to significant discrepancies in future financial periods. Early rectification prevents compounding issues and simplifies future accounting processes.

7. Supports Accurate Tax Reporting

Errors in recording income, expenses, or other transactions can lead to incorrect tax calculations, resulting in overpayment or underpayment of taxes. Rectification ensures accurate tax filings, avoiding penalties or audits from tax authorities.

Few related topics for your knowledge

- How To Prepare Year-End Adjustments In Accounting: Step-By-Step Tutorial

- Inventory Valuation Process In Accounting: Importance, Methods, & Examples

- Depreciation Entry In Accounting: Meaning, Examples, How To Calculate It/a>

- Chart Of Accounts In Tally Prime: A Definitive Guide For Beginners

- Learn From The Best Advanced Excel Courses Online

- Flash Fill In Excel: What Is it & Step By Step Tutorial

Examples Of Rectification Of Errors

According to different errors you need to make the rectifications accordingly. With the help of following examples things will become clearer to you.

a) Errors Of Omission

- Example:- A cash sale of Rs 1,000 to a customer was completely omitted from the books.

- Impact:- Sales and Cash/Debtors accounts are understated, but the trial balance still tallies as neither side was recorded.

- Rectification:-

Suspense A/c ———————- Dr Rs 300

Purchase A/c ————————————–Cr Rs 300

(To correct overstatement of sales and understatement of purchases)

b) Error Of Commission

- Example: A payment of Rs500 to Supplier A was mistakenly recorded as a payment to Supplier B.

- Impact: Supplier A’s account is overstated, and Supplier B’s account is understated, but the trial balance is unaffected as the debit and credit entries balance.

- Rectification:

Supplier A A/c —————————— Dr Rs 500

To Supplier B A/c ————————————-Cr Rs 500

(To correct payment wrongly recorded to Supplier B instead of Supplier A)

c) Errors Of Principal

- Example: A purchase of machinery worth Rs 2,000 was incorrectly recorded as a repair expense.

- Impact: The Machinery (asset) account is understated, and the Repair Expense account is overstated, affecting the balance sheet and profit calculation, but the trial balance tallies.

- Rectification:

Machinery A/c —————————— Dr Rs 2000

To Repair & Maintenance A/c —————————- Cr Rs 2000

(To correct capital expenditure wrongly recorded as revenue expenditure)

d) Compensating Error

- Example: Sales were overstated by Rs 300, and Purchases were understated by Rs 300 in the same period.

- Impact: The errors offset each other, so the trial balance balances, but both accounts misstate the financial position.

- Rectification:

Sales A/c ———————————– Dr Rs 300

To Purchase A/c ————————————– Crs Rs 300

(To correct the overstatement of sales and the understatement of purchases)

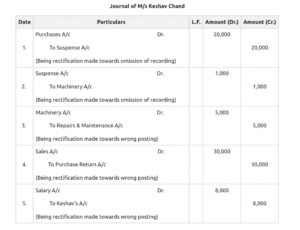

Format Of Rectification Of Errors

How Rectification Of Errors Influences The Trial Balance

There are several ways rectification of errors influences the Trial balance. Some of the key ways to know about it are as follows:-

1. Restores Balance

For errors affecting the trial balance, rectification eliminates discrepancies by correcting one-sided errors and clearing the Suspense Account, ensuring debit equals credit.

2. Ensures Accuracy

For errors not affecting the trial balance, rectification corrects individual account balances, making the trial balance a true reflection of the financial position.

3. Prevents Misstatements

Rectification ensures the trial balance provides accurate data for preparing financial statements, avoiding errors in profit, assets, or liabilities.

4. Supports Audit & Compliance

A corrected trial balance aligns with accounting standards and facilitates smooth audits by eliminating discrepancies or misstatements.

5. Maintains Integrity

By correcting errors, the trial balance reflects reliable data, supporting stakeholder trust and informed decision-making.

Final Takeaway

Hence, these are some of the common rectifications of errors in accounting that you need to address from your end. If you can go through this article in detail, then you will understand how it impacts the Trial Balance and Final Accounts.

You can share your views and comments in our comment box. This will help us to know your understanding in this regard. Here, you need to plan things accordingly to meet your goals with complete ease.

- You’re Smart Enough, But English Is Holding You Back. A Fluent English Speaking Course Can Fix That - July 3, 2026

- Movement Types in SAP MM: What They Are, Why They Matter, and How to Master Them - June 26, 2026

- No Experience? No Problem. Here’s How Freshers Are Landing SAP FICO Jobs in India Right Now - June 19, 2026