.jpg)

AI in Accounting: Will Automation Kill Finance Jobs?

Imagine this: You spend years learning accounting, only to have an AI bot finish in 3 minutes what took you 3 days. Scary? Exciting? Maybe both. The truth is, AI in accounting isn’t coming tomorrow—it’s already here

The finance and accounting industry is standing at a crossroads. For decades, accountants were seen as paper-pushers, calculators in hand, managing endless invoices and ledgers.

Today, artificial intelligence (AI) and automation are rewriting that story at lightning speed. From invoice processing that takes seconds to fraud detection that outsmarts human auditors, AI in finance is not just a trend — it’s a revolution.

But here’s the billion-dollar question: Will AI replace finance jobs, or will it create smarter, more rewarding careers?

Let’s dive in.

Table of Contents

- Widespread AI Adoption: The Inevitable Shift

- Applications & Use Cases of AI in Accounting

- Benefits of AI in Accounting

- Efficiency & Accuracy: Why Firms Can’t Resist AI

- Challenges in Accounting (Without AI) and How AI Overcomes Them

- How to Get Started With Accounting Intelligence

- Jobs at Risk vs. Jobs on the Rise

- Will AI Replace Accountants?

- Work-Life Balance & Human Value

- Global Perspective: India Leading the Charge

- The Skills That Will Define the Future

- Examples of AI Tools in Accounting

- AI In Accounting And Auditing

- Frequently Asked Questions

- Key Takeaways for Accounting Professionals

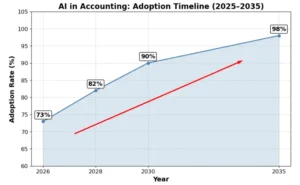

Widespread AI Adoption: The Inevitable Shift

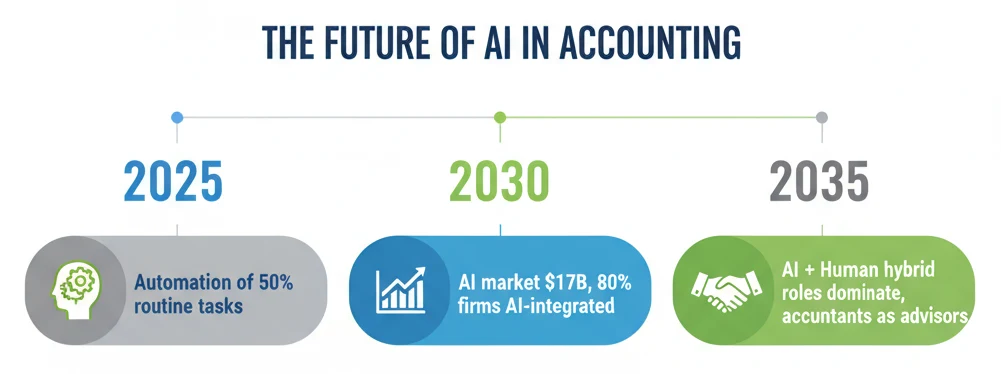

Just a few years ago, AI in accounting sounded like science fiction. Fast-forward to 2025, and it’s the new normal.

- 73–83% of firms now automate routine accounting tasks like data entry, invoice approvals, and reconciliation.

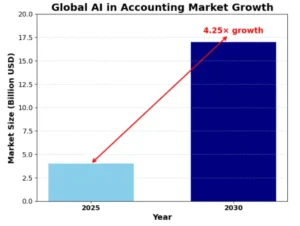

- The global AI-in-accounting market is expected to surge from $4 billion in 2025 to $17 billion by 2030.

- 82% of finance professionals already say AI will be essential to their workflow.

What this means is simple: ignoring AI in finance is no longer an option.

But adoption numbers only tell half the story. Let’s break down exactly how AI is being used in accounting firms today — and which tools are leading the charge.

Applications & Use Cases of AI in Accounting

| AI in Action | Smart Tools & Benefits |

|---|---|

| Automated Data Entry & Bookkeeping | Botkeeper, DataSnipper – Extract data from invoices, receipts, and bank statements. No manual typing, fewer errors. |

| Accounts Payable & Receivable Automation | Vic.ai, TaxDome – Automate invoice processing, payment scheduling, and reconciliation. Smooth cash flow, stress-free management. |

| Enhanced Auditing | MindBridge – Analyze 100% of transactions in real time, detecting anomalies and fraud beyond traditional sampling. |

| Financial Reporting & Forecasting | PwC Predictive Analytics, Zeni – Generate budgets and forecasts combining live + historical data. Smarter, data-driven decisions. |

| Fraud Detection & Compliance | MindBridge, QuickBooks AI – Flag suspicious patterns quickly and keep audit trails airtight. |

| Tax Compliance & Preparation | TaxDome – Automates tax calculations, suggests deductions, and adapts to changing laws. |

| Expense Management | Scribe, Zeni – Auto-verify expenses against policy for effortless compliance and accountability. |

“Each of these isn’t sci-fi—it’s happening in firms right now, and fast.”

Get a BBA Degree with Paid Intership1-year paid internship + 10 Simulation Software + 4 Certifications to land high-paying roles |

|

| BBA in accounting and finance |

Benefits of AI in Accounting

| Benefit | Example Tool/Use Case | Data/Impact Reported |

|---|---|---|

| Efficiency & Productivity | Vic.ai / Botkeeper | 80% faster invoice processing; 2,000+ hours saved yearly |

| Improved Accuracy | MindBridge | 90% higher fraud/anomaly detection vs. traditional audits |

| Deeper Insights | PwC Predictive Analytics | 35% more accurate financial forecasting |

| Enhanced Scalability | Zeni (for startups) | Handles 10x more transactions per accountant |

| Real-Time Reporting | QuickBooks AI Dashboard | Instant P&L and cash-flow updates |

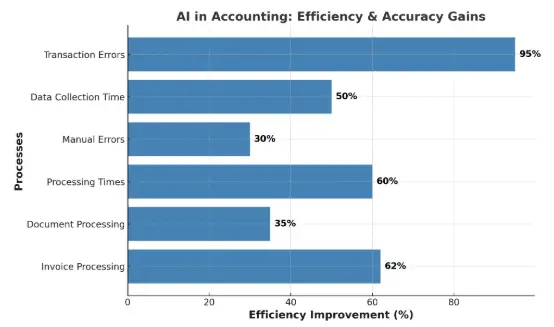

Efficiency & Accuracy: Why Firms Can’t Resist AI

AI’s biggest selling point? It saves time and eliminates errors.

- Processing times drop by up to 60%.

- Manual errors shrink by 30%.

- Invoice processing alone is cut by 60–62%, while document processing speeds up by 35%.

- Real-time AI forecasting is already used by 68% of CFOs, enhancing financial predictions.

And fraud detection? Between 2020 and 2022, AI-based fraud detection rose 40%, flagging $2+ billion in fake transactions. That’s not just efficiency; it’s survival.

Challenges in Accounting (Without AI) and How AI Overcomes Them

1. Repetitive Data Entry

The Problem:

Accountants spend a huge chunk of their day punching in invoices, receipts, and transactions. It’s boring, error-prone, and time-draining. For example, a mid-sized firm handling 5,000 invoices/month can lose 200+ hours to manual entry.

Example:

- A PwC study found data entry & reconciliation consume 40% of an accountant’s time.

- Manual invoice processing costs $12–$15 per invoice, while automated systems cut this to $2–$3.

Source: runeleven.com

How AI Solves It:

- OCR + AI bots read and extract invoice data with 97–99% accuracy.

- RPA (Robotic Process Automation) auto-matches invoices with payments in seconds.

- Firms report a 70% drop in processing time after AI adoption.

Table: Before vs After AI in Data Entry

| Metric | Manual Process | With AI Automation |

|---|---|---|

| Avg. Time per Invoice | 12–15 minutes | 2–3 minutes |

| Cost per Invoice Processed | $12–$15 | $2–$3 |

| Error Rate | 3–5% | <1% |

2. Human Errors in Accounting

The Problem:

Even the best accountants make mistakes. Typos, wrong entries, or missed reconciliation lead to compliance risks, penalties, and reputational damage.

Example:

- In 2020, a manual accounting error at Citigroup led to an accidental transfer of $900 million.

- A survey by BlackLine revealed 55% of CFOs don’t fully trust their company’s financial data due to manual errors.

Source: The Economic Times

How AI Solves It:

- Error Prevention at Entry: AI-driven data entry tools flag inconsistencies (e.g., if an invoice amount doesn’t match the purchase order) before it’s posted to the ledger.

- Duplicate Detection: Machine learning models scan entries in real time and flag potential duplicates — for instance, two identical vendor payments.

- Automated Reconciliation: AI compares bank feeds against books instantly, spotting mismatches that a human might overlook in hours of manual checking.

- Regulatory Accuracy: AI compliance engines automatically update to reflect changes in tax laws, reducing the risk of reporting errors.

Table: Impact of Human Error vs AI-Assisted Accounting

| Factor | Manual Accounting | AI-Enhanced Accounting |

|---|---|---|

| Avg. Error Rate | 2–5% of entries | <0.5% of entries |

| Fraud Detection | Weeks to months | Instant (real-time) |

| Compliance Penalty | High Risk | Significantly Reduced |

How to Get Started With Accounting Intelligence

Introducing AI into accounting doesn’t mean ripping out everything you currently do. Instead, it’s about taking small, practical steps that allow firms to test, learn, and gradually scale. Here’s a straightforward approach:

- Begin With Small, High-Impact Tasks

Start by automating repetitive processes like data entry or invoice scanning. Tools powered by OCR (Optical Character Recognition) can quickly pull details from receipts, invoices, and bank statements, saving hours of manual work.

Example: Platforms like DataSnipper and Botkeeper are ideal for entry-level automation.

- Pick Scalable, Subscription-Based Tools

Instead of investing heavily in enterprise solutions, explore SaaS-based AI tools. These come with lower upfront costs and can grow with your firm’s needs.

Example: Vic.ai offers accounts payable automation that small firms can adopt without huge IT investments.

- Train Your Team Early

AI is only effective if your people know how to use it. Encourage your staff to upskill with short courses in AI, data analytics, or finance tech. This reduces resistance and helps them shift from routine tasks to more strategic roles.

- Keep Humans in Control

Think of AI as a co-pilot — it can speed up processes, but final judgment should remain with accountants. Always maintain human review in sensitive areas like auditing, fraud detection, and compliance.

- Expand Into Advanced Insights

Once your team is comfortable, move towards AI-powered forecasting, fraud detection, and real-time dashboards. These tools provide the kind of insights that help businesses make data-driven, future-ready decisions.

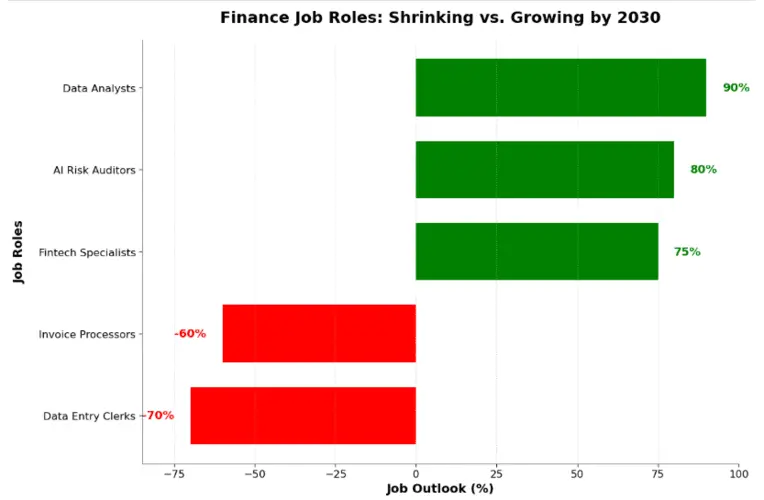

Jobs at Risk vs. Jobs on the Rise

By 2030, 75–90% of repetitive tasks like data entry and invoice processing may be fully automated. But higher-level roles — advisory, auditing, strategic budgeting — remain firmly human-led.

In fact, AI is creating new opportunities:

- AI risk auditors to oversee algorithmic decision-making.

- Data analysts to interpret AI-driven insights.

- Strategic finance advisors who use AI forecasts to guide big decisions.

Even the Big Four are betting on this shift. EY has pledged $1 billion to integrate AI, aiming to grow its human workforce to 500,000 — supported by 200,000 AI agents. That’s not replacement, that’s augmentation.

Few related topics for your knowledge

- How To Prepare Year-End Adjustments In Accounting: Step-By-Step Tutorial

- Inventory Valuation Process In Accounting: Importance, Methods, & Examples

- Depreciation Entry In Accounting: Meaning, Examples, How To Calculate It/a>

- Chart Of Accounts In Tally Prime: A Definitive Guide For Beginners

- Rectification Of Errors In Accounting: Key Types & Methods

Will AI Replace Accountants?

AI in accounting is no longer a futuristic concept—it’s already reshaping how audits, tax filings, and compliance are handled. Many fear this will lead to massive job cuts. But the truth is more subtle: AI will automate tasks, not entire professions.

Here’s a clear breakdown of what finance tasks are likely to be automated by 2030—and what human roles will remain essential:

| Task | % Automated by 2030 | Human Role Left |

|---|---|---|

| Data Entry | 90% | Oversight & Audit |

| Invoice Processing | 75% | Exception Handling |

| Fraud Detection | 80% | Strategic Risk Management |

| Forecasting | 60% | Business Advisory |

Instead of killing jobs, AI will shift them. Accountants will move from repetitive tasks (like punching invoices) toward higher-value activities like risk strategy, advisory, and decision-making support

Work-Life Balance & Human Value

One of the most surprising outcomes of AI adoption? Accountants feel happier.

A survey found 85% of accountants said AI improves their work-life balance. Why? Because they’re spending less time on mind-numbing repetitive tasks and more time on impactful, strategic work.

Think of it like this: instead of entering 1,000 invoices into Excel, you’re analyzing how cash flows affect company strategy. That’s not just a job upgrade — it’s a career transformation.

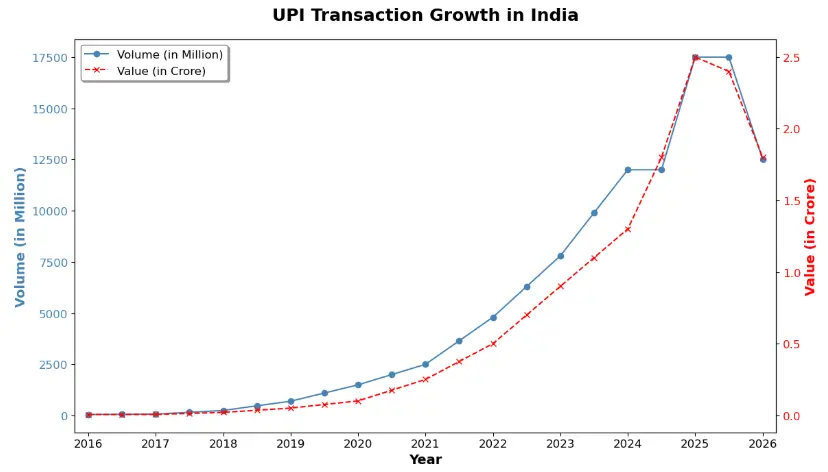

Global Perspective: India Leading the Charge

India is emerging as a powerhouse in AI-driven finance.

- ICAI (Institute of Chartered Accountants of India) has already trained 25,000 chartered accountants in AI tools.

- It predicts over 12.5 million new jobs in accounting will emerge thanks to AI.

- With UPI and fintech adoption skyrocketing, India is building a generation of AI-literate accountants ready for the global stage.

The Skills That Will Define the Future

Here’s the truth: the accountants of tomorrow will need very different skill sets.

In demand by 2025+:

In other words, the future of finance jobs is less about “Can you do this calculation?” and more about “Can you guide a company through financial uncertainty using AI-powered insights?”

Practical Examples of AI in Accounting Tools

- DataSnipper → Automates data extraction in Excel.

- Vic.ai → AI-powered accounts payable automation.

- MindBridge → AI auditing platform.

- Botkeeper → AI bookkeeping assistant.

- Zeni → AI financial management for startups.

- TaxDome → AI tax automation tool.

- Scribe → AI workflow and training automation.

AI In Accounting And Auditing

Core applications of AI In Accounting ( Where AI Is Used Today)

| Area | AI Use Case | Real Tools | Impact |

|---|---|---|---|

| Bookkeeping & Data Entry | OCR + NLP auto-categorizes invoices, receipts | Vic.ai, MindBridge, Xero AI, Dokka | 90%+ reduction in manual entry |

| Expense Audit | Anomaly detection on T&E | AppZen, Oversight Systems | Flags 1 in 7 fraudulent claims |

| Accounts Reconciliation | Auto-matching bank feeds, intercompany | BlackLine AI, FloQast AutoRec | 3–5 day close → same-day |

| Audit Sampling → 100% Audit | Risk-scoring every transaction | KPMG Clara, PwC Halo, EY Canvas AI, MindBridge Ai Auditor | From 2–5% sample to 100% population |

| Journal Entry Testing | Benford’s Law + ML clustering | CaseWare IDEA AI, Diligent HighBond | Detects round-tripping, unusual patterns |

| Revenue Recognition (IFRS 15 / ASC 606) | Contract parsing + revenue scheduling | Zuora RevPro AI, Aptitude RevStream | Auto-classifies performance obligations |

| Tax Provision & Compliance | Tax code mapping, scenario modeling | Thomson Reuters ONESOURCE AI, Vertex AI | Real-time tax impact simulations |

| Predictive Analytics | Cash flow, going concern, fraud risk | Sage Intacct AI, Workiva + AI | 6–12 month early warnings |

Frequently Asked Questions

What is AI in accounting?

AI in accounting uses automation and machine learning to handle tasks like bookkeeping, auditing, and data analysis.

How does AI improve accuracy?

It reduces human errors by automating repetitive and data-heavy processes.

Can AI help detect fraud?

Yes, AI quickly spots unusual patterns and anomalies in financial data.

Will AI replace accountants?

No, it supports accountants by handling routine tasks so they can focus on strategic work.

How does AI save time in accounting?

It automates data entry, reconciliations, and reporting, cutting down manual effort.

What are the main benefits of AI in accounting?

Speed, accuracy, fraud detection, cost savings, and better decision-making.

What challenges come with AI adoption?

High setup costs, data privacy issues, and the need for skilled professionals.

How are big firms using AI?

Firms like Deloitte and PwC use AI for auditing, tax compliance, and forecasting.

Is AI affordable for small businesses?

Yes, cloud-based AI tools make automation accessible even to small firms.

What are the best AI tools for accounting?

Popular tools include Botkeeper, Vic.ai, MindBridge, QuickBooks AI, and Zeni.

Key Takeaways for Accounting Professionals

The rise of AI in accounting isn’t a doomsday story.

Yes, routine tasks will vanish. But in their place, we’ll see more meaningful, more strategic, and more impactful finance careers. Professionals who embrace AI won’t just survive — they’ll thrive.

So, will automation kill finance jobs? No. It will kill the boring parts and create smarter, more human careers.

AI won’t take your job—someone who knows AI will. The only question is: Will that someone be you, or the person who gets hired instead of you?