.jpg)

Reconciliation in Accounting: Your Financial Reality Check

Have you ever checked your bank balance and wondered why it doesn’t match your records? While this is a common frustration for individuals, in the business world, resolving this mismatch is not optional, it’s essential. This process is called reconciliation in accounting. Think of it as the fact-checking stage of your financial cycle, ensuring every transaction is accurate and accounted for.

In this guide, we will break down the accounts reconciliation meaning, explore different types of ledger checks, and show you how to keep your books crystal clear.

Table of Contents

- What is Reconciliation in Accounting?

- The Common Types of Ledger Account Reconciliation

- Common Reconciliation Errors and How to Avoid Them

- Reconciliation vs. Audit: What’s the Difference?

- Exploring Specialized Reconciliation Methods

- Using Technology: SAP, Zoho, and TallyPrime

- Best Practices for Effective Account Reconciliation

- The Step-by-Step Process

- Industry-Specific Reconciliation Examples

- A Sample Reconciliation Case Study

- Conclusion

- Frequently Asked Questions

What is Reconciliation in Accounting?

At its core, reconciliation in accounting involves comparing two sets of financial records to confirm they match. Most often, this means matching your internal general ledger with an external source such as a bank statement or vendor invoice.

Why Does It Matter?

Accuracy is critical. If your records show more money than you actually have, you risk overspending. If they show less, you could miss valuable growth opportunities. Regular reconciliation helps you:

- Catch errors before they escalate.

- Prevent internal and external fraud.

- Prepare accurate financial statements for tax season.

Opt for a NAAC A + AICTE approved BBA Degree1-year paid internship + 10 Simulation Software + 4 Certifications. 90% Practical Learning. |

|

| Bachelor in Accounting and Finance |

The Common Types of Ledger Account Reconciliation

Not all accounts function the same way, so reconciliation methods vary depending on the account type. Understanding the types of general ledger reconciliation is the first step toward a healthy balance sheet.

| Reconciliation Type | What is Compared? | Primary Goal |

| Reconciliation of Bank Statements | Cash book vs. Bank records | Match cash on hand with bank balances. |

| Vendor Account Reconciliation | Accounts payable vs. Vendor statements | Ensure you don’t overpay or miss bills. |

| Customer Reconciliation | Accounts receivable vs. Customer payments | Verify that all sales are paid in full. |

| Intercompany Reconciliation | Branch A records vs. Branch B records | Balance transactions between departments. |

Vendor Reconciliation in Accounts Payable

Managing debt is a delicate task. Vendor reconciliation in accounts payable involves checking your records against the statements sent by your suppliers. This ensures that every invoice received is recorded and that no duplicate payments are made.

Detailed Ledger Account Reconciliation

A ledger account reconciliation looks at specific accounts within your general ledger. For instance, you might reconcile your payroll account or a petty cash fund. This ensures that the balances reported in your financial statements are valid and accurate.

Common Reconciliation Errors and How to Avoid Them

Even the most careful accountants can run into hurdles. Identifying these common traps is vital for flawless reconciliation in accounting.

- Missing Bank Fees or Interest: It is easy to forget service charges or interest. Always check your statement for these small deductions before finalizing your accounts reconciliation statement.

- Tax Discrepancies: Errors often occur due to GST rate or amount mismatches between your records and the other party’s books.

- Unrecorded Tax Credits: Discrepancies frequently arise when TDS (Tax Deducted at Source) is deducted by a party but not yet entered into your own system.

- Timing Issues: “Goods in transit” can cause a temporary imbalance where one party has recorded a shipment while the other has not yet received it.

- Duplicate or Wrong Entries: Simple human error, such as a “wrong entry” or failing to record goods that were returned, can throw off your vendor account reconciliation

Reconciliation vs. Audit: What’s the Difference?

While both involve checking records, they serve very different purposes. Knowing the difference is great for clarity and compliance.

| Feature | Reconciliation | Audit |

|---|---|---|

| Purpose | To match two sets of records for accuracy. | To provide an official opinion on financial health. |

| Frequency | Ongoing (Daily or Monthly). | Periodic (Usually Annually). |

| Performed By | Internal accounting staff. | Independent third-party auditors. |

| Outcome | Adjusted and balanced ledgers. | An audit report for stakeholders. |

Exploring Specialized Reconciliation Methods

Depending on the size of your business and your industry, you might encounter more specific processes.

1. Batch Reconciliation

Batch reconciliation is often used by companies that process large volumes of transactions, like retail stores. It involves matching a “batch” of transactions (like a whole day of credit card sales) against the total deposit in the bank.

2. Custodian Reconciliation

For firms dealing with investments, custodian reconciliation is vital. This involves matching the company’s internal investment records with the reports provided by the bank or firm holding the assets (the custodian).

3. Accounts Reconciliation Statement

An accounts reconciliation statement is a formal summary. It explains the differences between two accounts. For example, if you have a “check in transit,” this statement lists it so the final balances still make sense.

Using Technology: SAP, Zoho, and TallyPrime

Manual work is prone to human error. Fortunately, modern software makes reconciliation in accounting much faster.

- Bank Reconciliation SAP: Large enterprises use SAP to automate complex matching. It handles high-volume data and integrates directly with global banking systems.

- Zoho Books Reconciliation: For small to medium businesses, Zoho Books offers a user-friendly way to fetch bank feeds. You can click “Match” on transactions, making the process almost instant.

- TallyPrime Reconciliation: TallyPrime is a powerful tool for generating a “Confirmation of Accounts” directly from your ledger.You can quickly navigate to this by pressing Alt+G (Go To), selecting Ledger Vouchers, and choosing the specific account.From there, you can generate the report by selecting Confirmation of A/cs under the print or export settings. This allows you to export the statement to MS Excel for easier comparison during an audit.

Best Practices for Effective Account Reconciliation

To maintain high standards, you need a consistent system. These practices ensure your ledger account reconciliation remains accurate and audit-ready.

- Stick to a Schedule: Set a fixed date each month to close the books.

- Standardize Your Workflow: Use a template for every accounts reconciliation statement.

- Separate Duties: To prevent fraud, the person who handles cash should not be the one performing the reconciliation.

- Keep Documentation: Always save copies of the bank statements or invoices used during the process.

The Step-by-Step Process

To perform a successful reconciliation, follow these simple steps:

- Retrieve Records: Get your internal ledger and the external statement (like a bank or vendor report).

- Compare Transactions: Match each entry. Look for dates, amounts, and payees.

- Identify Discrepancies: Note any items that appear in one record but not the other.

- Adjust the Books: Record bank fees, interest, or missing invoices via journal entries.

- Finalize: Ensure the adjusted balances match perfectly.

Industry-Specific Reconciliation Examples

Reconciliation in accounting looks different depending on your industry. Here are a few real-world scenarios:

- Retail & E-commerce: A store uses batch reconciliation to match the total from their Point of Sale (POS) system against actual bank deposits.

- Manufacturing: These firms focus heavily on vendor account reconciliation to ensure raw material costs match their purchase orders.

- Corporate & Branch Accounting: Large firms must perform “Branch Reconciliation.” This involves matching the Branch balance maintained at the Head Office with the Head Office balance maintained at the branch.

- Common Branch Discrepancies: Differences here often occur because of goods transferred between branches or expenses met by the Head Office without informing the branch.

Few related topics for your knowledge

- Job Guarantee Vs Job Assistance: Core Points Of Differences Between The Two

- 10 Life Changing Simulation Softwares To Learn In Upcoming Years

- Top 20 Journal Entries Questions And Answers For Interview

- 15 Essential Inventory Valuation Questions & Answers For Interview

- 25 Important BRS Questions For Interview Preparation

A Sample Reconciliation Case Study

To see reconciliation in accounting in action, consider this example of a company matching its books with a debtor (customer).

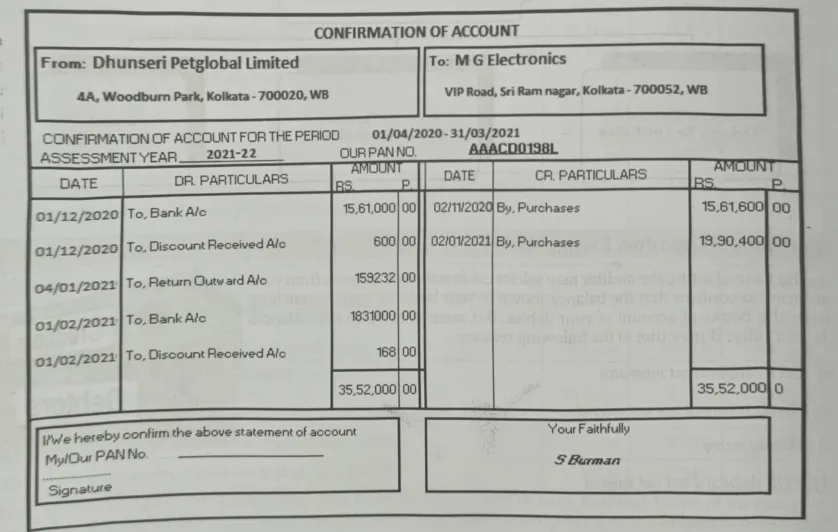

Example: You are the accountant of M G Electronics and the following transactions have been entered in the books of the enterprise –

The following confirmation of accounts for the year 2020-21 has been received from Dhunseri Petglobal Limited –

From the above two statements, we can see that, balance of Dhunseri Petglobal Limited as per books of account of your company maintained using Tally is Rs. 1,60,000 whereas the balance is Nil as per books of account maintained by Dhunseri Petglobal Limited.

Before preparation of Reconciliation Statement, we have to find out the reasons behind such mismatch. The differences arise due to the following reasons-

a) Discount of Rs. 600 allowed to them on 01/12/2020 was not entered in our books

b) Goods of Rs. 1,59,232 returned by the them on 04/01/2021 was not entered in our books

c) Discount of Rs. 168 allowed to them on 01/02/2021 was not entered in our books

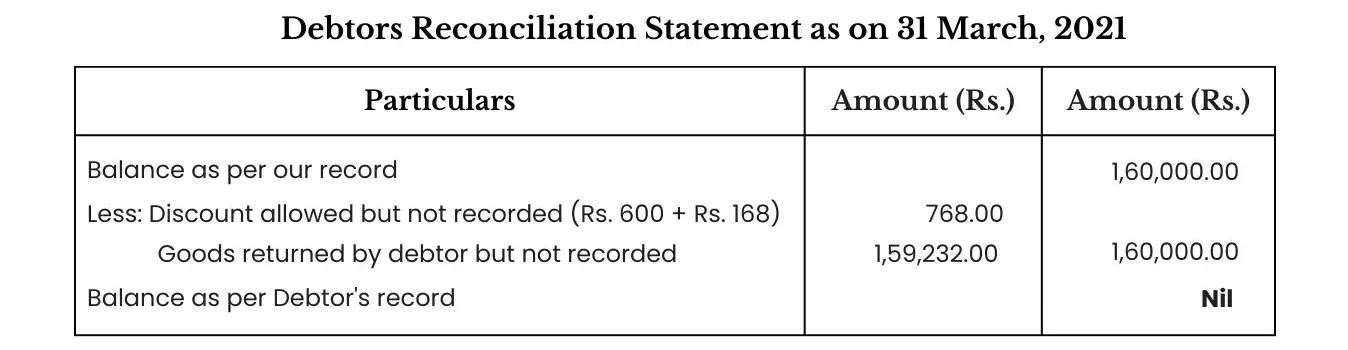

Now we can prepare the Debtors Reconciliation Statement:

So, the main concept behind preparation of reconciliation statement is finding out the differences between two balances and matching of the same

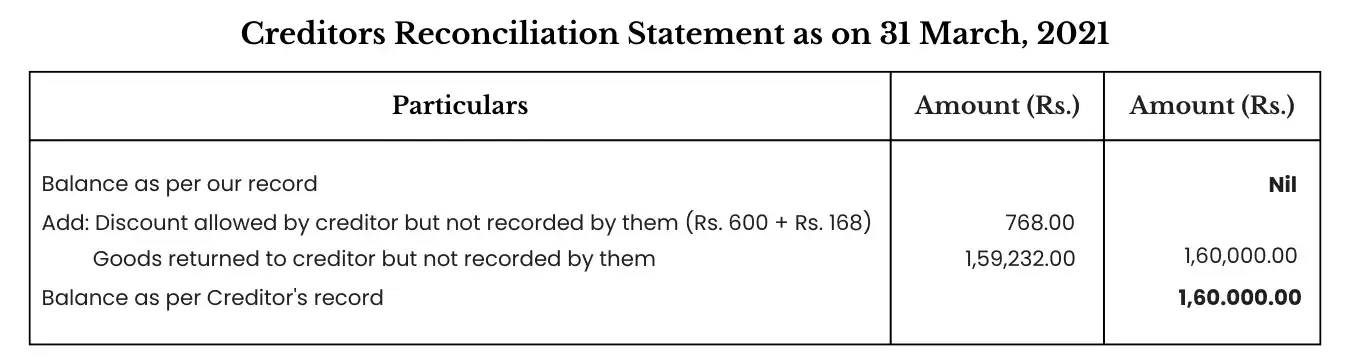

Here, you have prepared a Debtors Reconciliation Statement on behalf of your company. In contrast to it, Dhunseri Petglobal Limited will prepare Creditors Reconciliation Statement:

Conclusion

Mastering reconciliation in accounting is the best way to maintain a pulse on your business’s financial health. Whether you are performing a simple reconciliation of bank statements or a complex vendor account reconciliation, the goal is the same: total accuracy.

Ready to take control of your finances? Start by setting a monthly schedule for your ledger reviews. If you need help, consider using automated tools to save time and reduce stress.

Frequently Asked Questions

1. What is the basic account reconciliation meaning?

It is the process of comparing internal financial records with external statements to ensure the balances match and are accurate.

2. How often should I perform vendor reconciliation in accounts payable?

Most businesses should perform this monthly. It helps catch missed invoices or overcharges before the next payment cycle.

3. What is the difference between manual and automated bank reconciliation SAP?

Manual reconciliation requires a person to tick off every transaction on paper. SAP automates this by using algorithms to match thousands of transactions instantly.

4. Why is a ledger account reconciliation necessary for small businesses?

Even small businesses can have errors. Checking your ledger ensures your tax filings are correct and prevents you from spending money you don’t actually have.

5. What is a batch reconciliation used for?

It is used to verify groups of transactions at once. It is very common in industries with many small transactions, like grocery stores or e-commerce sites.

6. Can Zoho Books reconciliation help with my bank statements?

Yes. Zoho Books connects to your bank account, imports your transactions, and suggests matches, which simplifies the reconciliation of bank statements.

- No Experience? No Problem. Here’s How Freshers Are Landing SAP FICO Jobs in India Right Now - June 19, 2026

- Stop Wasting Hours on Spreadsheets: The Ultimate Guide to Excel Training for Beginners (And How It Lands Jobs) - June 12, 2026

- The Laptop Lifestyle: How to Pivot to a High-Paying Data Career in 2026 - June 6, 2026