.jpg)

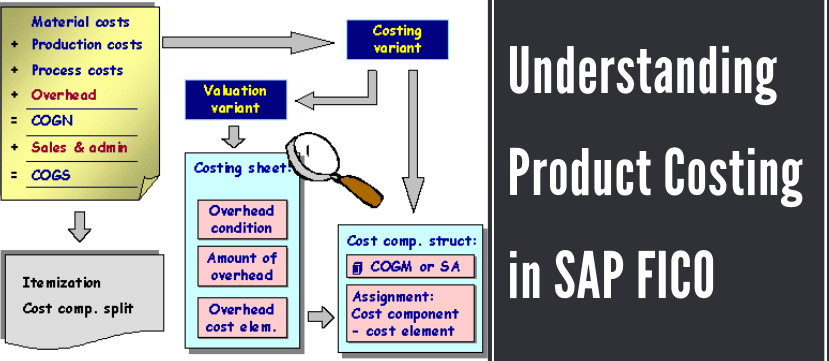

Understanding Product Costing in SAP FICO

You know the essential stuff about SAP FICO by now if you have been a regular follower of our blog. We are a reputed SAP training institute in India and provide modular courses on Excel, Accounting, GST, SAP among others.

SAP FICO is one of the 25 odd modules that SAP has to offer. It is one of the most useful in the industry as well.

Product costing is the cost accounting methodology for evaluating the expenses of creating company products. These costs include worker wagers, raw material purchases, transportation costs, production costs, and even retail or wholesale stocking fees.

Product costing comes under the ambit of the controlling module (CO in FICO). It ascertains the quantitative value of the internal cost of materials and production for the purposes of management accounting.

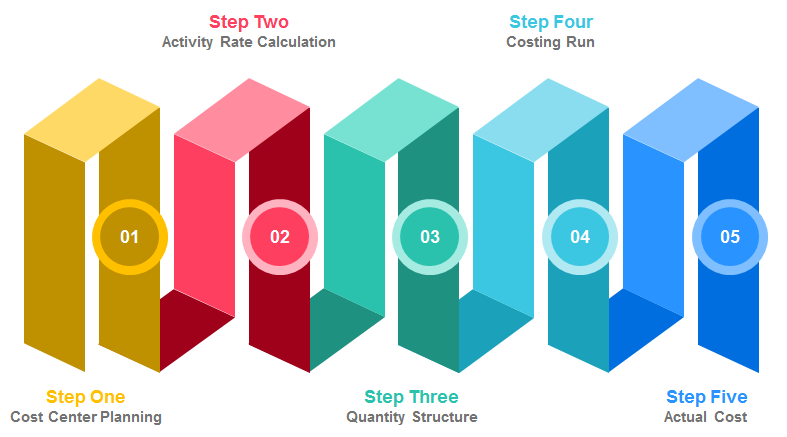

A SAP training institute like ours follows these basic five steps for understanding product costing in SAP FICO.

(Courtesy – SAPInfo)

1. Cost Center Planning

Cost center planning is the first step to understand product costing. The main aim of this is to plan the total money and quantities per cost center.

Assumptions:

- Company codes in the business are already planned out.

- Master data for profit and cost centers, primary and secondary cost elements, activity types, etc. have already been prepared.

In the KP06 transaction, cost center currencies are segregated by Activity type and cost element. Fixed and variable currencies are to be entered. The end-user can estimate costs in production cost centers that crop up through allocations.

KP26 transaction deals with the cost center quantities segregated by Activity type. Based on the previous fiscal’s actual values, the activity rate is manually entered. Planning activity quantities based on useful installed capacity accounts for interruption is what is generally followed.

2. Activity Rate Calculation

The primary objective of this step is to estimate the rates of each activity plan in each cost center in a factory or plant.

Assumptions:

- Cost Center Plans in transaction KP06 and Plan activity units in KP26 have been made and taken into account.

When cost center dollars and quantities are determined, activity rates to be implemented for evaluating internal activities for production are calculated. A mixed approach can also be used. Plan rates for a few cost centers can be calculated on the basis of other rates.corresponding to last activities.

When all cost center plans are drawn up, plan assessments and distributions to fixate costs are carried out for overhead cost centers.

3. Quantity Structure

This step is concerned with the calculation of the components of manufactured products and the cost of goods sold

Assumptions:

The assumptions are that the Master data has been created which include the following

- Material Masters

- Work Centers (Cost Centers and Activity Types)

- Bill of Materials (BOM)

- Routings (Product Planning)

- Master Recipes (Production Planning – Process Industries)

- Production Versions

- Product Cost Collectors (Production Planning Repetitive Manufacturing)

Quantity Structure serves as the basic integration point between Finance and Logistics modules. A material master has to be created for each product with a distinctive fit/form in a factory. It comprises of a number of views such as Material Resource Planning (MRP) views, accounting views, and cost views. Bill of Materials (BOM) is created for each and every produced material. The BOM list has the component materials and quantities required for producing a semi-finished or finished product.

4. Costing Run

Costing run helps estimate cost mass volumes of materials in a specific company code. This allows the user to select materials, denote quantity structure, and cost.

Assumptions or necessary stuff:

- Material Masters (MRP, Accounting and costing views)

- Quantity Structure (Master Recipe, BOM, Routing and Production versions)

- Condition types and production Information records

- Configuration

- CO Master Data

All of the materials are cost estimated for the duration of the annual or monthly costing processes. Transaction CK40N is used to create costing runs, analyze results, mark and release costs. This can be made using a controlling area, costing version, costing variant, company code, and transfer control.

5. Actual Cost

This is the final step. Actual costs are determined by actual expenses, purchase price, and production quantities. These costs are tallied to the standard costs through variance analysis. This is mostly to identify profitability and make decisions on management.

Assumptions or necessary stuff:

- Material Masters (MRP, Accounting and costing views)

- Quantity Structure (BOM, Master Recipe)

- Configuration

- CO Master Data

- Assessment/Distribution Cycles

- Actual Statistical Key Figures

Production confirmation consists of product cost by order, actual production yield, scrap, and activity quantities. The production costs are made of the production orders for review and settlement. In the case of product cost by period, product cost collectors are used to calculate WIP, variances, and settlement rather than just the planned orders.

Interested to learn more? Don’t forget to check this course from the SAP training institute around!

Follow our Facebook, Twitter, and Instagram pages if you want to stay abreast of the latest happenings in the field of Accountancy, SAP, GST, etc.

- 10 of the Best Accounting Software in India (Reviews with detailed comparison) - August 2, 2020

- Top Career Opportunities For Accountants - June 2, 2020

- Data Security in Tally.ERP 9 - June 1, 2020