.jpg)

Indian Financial System and Markets: Pulse of Indian Finance

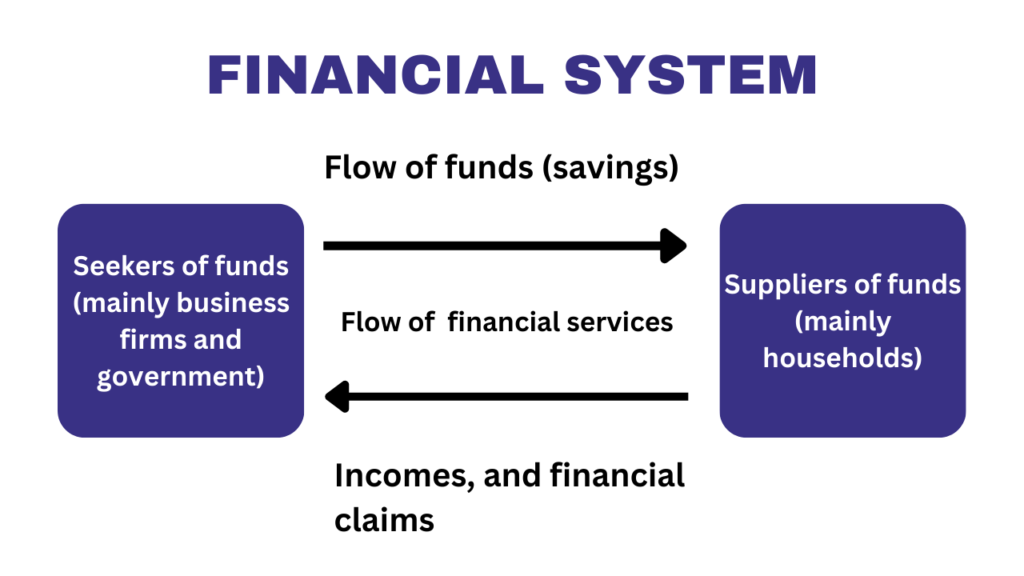

The development of a nation’s economy is shown by the progress of different economic sectors. These sectors are widely classified into Corporate, Government, and Household Sectors. There are areas or people with extra funds and there are those who don’t have surplus funds. This is where the role of an Indian Financial System and markets comes in. It functions as an intermediary and promotes the flow of funds from the surplus areas to the deficit areas.

A Financial System comprises various instruments, practices, regulations and laws, analysts, money managers, transactions, claims, and liabilities.

Financial markets, financial instruments, and services that support capital formation are only a few of the interrelated subsystems that make up the financial system. It provides a process for turning savings into investments.

Table of Contents

What is a Financial System?

When referring to the “financial system,” the word “system” refers to a collection of complexly interconnected economic institutions, agents, practices, markets, transactions, claims, and liabilities. Money, credit, and finance are three ideas that are interconnected but yet slightly different from one another that are addressed by the financial system. The Indian financial system is composed of the financial market, financial instruments, and financial intermediation.

Let’s dive into the world of the Indian financial system and Markets to understand how it looks and works

Indian Financial System and Markets Overview

An Indian financial system serves as an intermediary between investors and savers. It makes it easier for money to move from areas of surplus to areas of deficit. It is related to finances, credit, and money. These three components are interdependent and have a close relationship with one another.

A financial system is a collection of organizations, tools, and markets that encourage saving and direct money toward its most effective use. Individuals (savers), intermediaries, markets, and savings consumers (investors) make up this group.

Be an Expert in Finance MarketLearn from the Industry Experts |

|

| Stock Market For Beginners | Diploma in Financial Markets (DFM) |

Structure of the Indian Financial System and Markets

The term “financial structure” describes the structure, components, and order of the financial system. A formal (organized) financial system and an informal (unorganized) financial system can be used to broadly categorize the Indian financial system and Markets.

- Informal Indian Financial System: Individual lenders, groups of people acting as funds or associations, partnership firms made up of local brokers and pawnbrokers, as well as non-banking financial intermediaries like finance, investment, and chit-fund enterprises, make up the informal financial system.

- Formal Indian Financial System: Financial markets, financial instruments, financial services, and financial institutions make up the formal financial system.

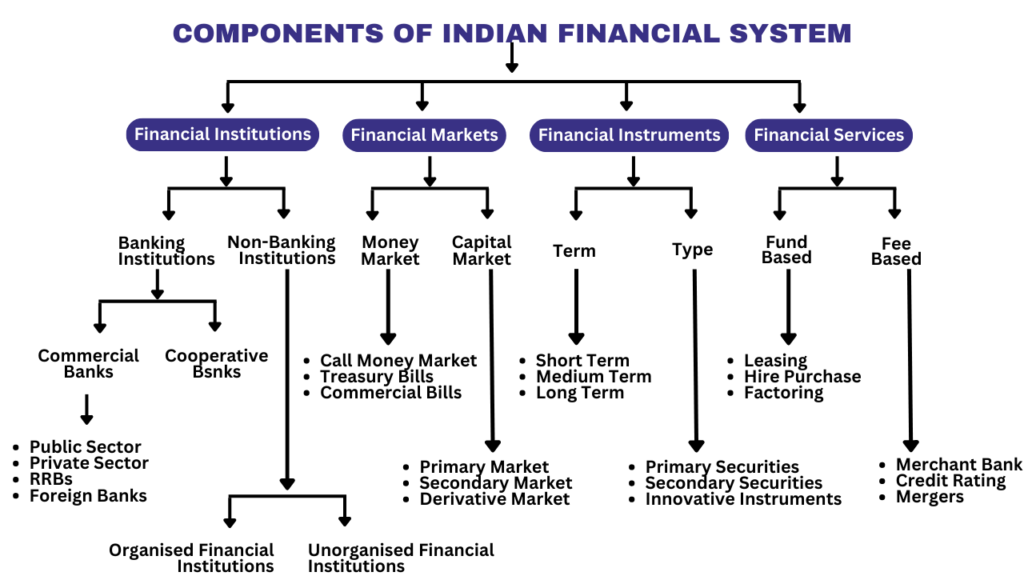

The Ministry of Finance, the RBI, the SEBI, and other regulating organizations make up the official Indian financial system. The Indian financial system is made up of the following elements, which will be briefly reviewed below

Now you can understand the actual difference between formal and informal Indian financial systems and markets. In the next part, we will describe the different components of the Indian financial system and markets.

Financial Institutions

Banking Institutions:

Commercial Banks

Commercial banks are financial institutions that offer services such as accepting deposits, providing loans, and basic investment products.

These include Public Sector Banks (e.g., State Bank of India), Private Sector Banks (e.g., ICICI Bank), Regional Rural Banks (RRBs), and Foreign Banks (e.g., HSBC).

Cooperative Banks

Cooperative banks are owned and operated by their customers to provide banking services to members.

These are financial entities that operate on a cooperative basis, catering to the financial needs of the members.

Non-Banking Institutions

Organized Financial Institutions

Organized financial institutions are licensed entities that offer financial services and products, often regulated by government authorities.

Examples: It includes insurance companies and pension funds.

Unorganized Financial Institutions

Unorganized financial institutions operate informally, often without legal recognition, providing financial services within communities.

These are informal financial entities such as moneylenders and community savings groups.

Financial Markets

Money Market

The money market is a segment of the financial market in which financial instruments with high liquidity and short maturities are traded.

This includes the Call Money Market, Treasury Bills, and Commercial Bills.

Call Money Market

The call money market facilitates short-term borrowing and lending, often among banks, with transactions usually within a day.

It consists of the Primary Market, Secondary Market, and Derivative Market.

Financial Instruments

Based on Types

Primary Securities

Primary securities are financial instruments offered for the first time to investors, typically through an initial public offering (IPO) or bond issuance. These include stocks and bonds issued directly to investors.

Secondary Securities

Secondary securities are financial instruments that have already been issued and are traded among investors in the secondary market. Examples are stocks traded on stock exchanges.

Innovative Instruments

Innovative instruments include sophisticated financial products designed to cater to specific investment strategies and risk appetites. These involve complex financial products like derivatives and ETFs.

If you are looking to learn financial marketing in depth then explore the courses designed by ICA experts here

Want to become a Finance ExpertBe confident! Learn Finance from Industry Experts |

|

| Browse Classroom Course | |

Based on Term

Short-Term Financial Instruments

- Easy to convert to cash within one year

- Highly liquid and flexible

- Offer lower returns than other types of investments

Examples: Treasury bills, Commercial bills, Call money market instruments

Medium-Term Financial Instruments

- Easy to convert to cash within one to five years

- Offer a balance of risk and return

- Good option for investors who are looking for moderate growth over a medium period

Examples: Some bonds, Some notes

Long-Term Financial Instruments

- Easy to convert to cash after five years or more

- Typically offer higher returns than other types of investments

- Also, involves higher risks

Examples: Stocks, Long-term bonds

Financial Services

Fund-Based Financial Services

Fund-based financial services involve providing capital to businesses for various purposes, often tied to specific assets or transactions.

Leasing, Hire Purchase, and Factoring: These services involve providing funds for asset acquisition and working capital needs.

Fee-Based Financial Services

Fee-based financial services generate revenue through fees charged for services like advisory, credit assessment, and facilitating mergers and acquisitions.

Merchant Banking, Credit Rating, and Mergers: These services charge fees for advisory, rating, and transactional services.

Hope now you can understand the key concepts of each component of the Indian Financial System and markets easily. Each component of the Indian financial system has its ways of contributing to the Indian economy.

If you are interested in knowing how the Indian financial system helps in economic growth keep reading

Role and Importance of the Indian Financial System in Economic Development

It connects investors and savers. It helps in efficiently and effectively mobilizing and allocating savings. It contributes significantly to economic growth through the process of saving and investing. Capital formation is the process of saving and investing.

- You can monitor corporate performance.

- It offers a method for reducing risk and managing uncertainty.

- It offers a means of moving resources across geographical boundaries.

- It provides options for portfolio adjustment (offered by financial markets and financial intermediaries).

- It helps lower transaction costs and increases returns. People will be inspired to save more money by this.

- It promotes the process of capital formation.

- It supports the deepening and broadening of the financial system.

Financial deepening refers to the development of a growing number and variety of players and instruments, whereas financial deepening refers to an increase in financial assets as a percentage of GDP.

A financial system accelerates economic progress, to put it briefly. It supports growth through advancing technology.

Key Takeaways

The Indian financial system and markets are vital to the country’s economic growth and development. India offers a dynamic and evolving landscape for investors, businesses, and individuals, with a wide range of financial institutions, markets, and instruments. The Indian financial system has shown flexibility and adaptability in the face of various economic challenges over the years.

As the Indian economy expands and globalizes, the financial sector is expected to grow in tandem. Government initiatives and technological advancements have created new opportunities for financial inclusion and innovation. Both seasoned and novice investors need to understand the complexities of the Indian financial system and markets to make informed decisions.

In this era of rapid change and digital transformation, it is critical to stay up-to-date on the latest trends and regulations. The Indian financial system and markets are poised for exciting developments, and those who navigate them wisely will be better positioned to capitalize on the opportunities they offer.

Read More articles to enhance your knowledge and skills.

- A Comprehensive Guide to GST Basic Concepts for Students

- Mastering SAC Codes: Key to GST Compliance

- Simplifying Accounting: E-Invoice in Tally Prime

- Reverse Charge Mechanism in GST: Definition, Example, Types, Applicability, Time of Supply

- Time of Supply in GST Explained

- GST HSN Codes List: Find the Right Code for Your Products

- GST Reporting: Complete Overview of 2-Factor Authentication in GST

- GST Return Types: Due Dates and Filing Procedures

- Types of GST in India: IGST, SGST, CGST & UTGST Made Easy for Students