.jpg)

GST Reforms: Anti-Profiteering Measures You Should Know

Goods and Services Tax (GST) as the poster boy of Indirect Taxation in India has been persistently in the news since its implementation. The tax came into effect from 1 July 2017 through the implementation of the 101st Amendment of the Indian Constitution. A thorough understanding of GST is a must for successfully pursuing any GST course.

To recall, GST is an Indirect Tax (or Consumption Tax) used in India on the supply of goods and services. The GST replaced existing multiple taxes levied by the central and state governments except for a few state taxes. It is a comprehensive, multistage, destination-based tax.

So what are the profiteering and anti-profiteering measures that come under the ambit of the GST regime? Read on.

Profiteering

Well, to understand profiteering, it’s imperative to understand profit margins. When a company sells products, it gathers a variety of expenses – like those incurred from taxes, building rent, raw material costs, and packaging costs.

Understandably, the company needs to charge a higher price to make a profit. The difference between those expenses and the revenue got from selling the products is the profit margin. Profiteering happens when product prices are inflated unfairly to create a higher profit margin. Companies may do this when there’s a high demand for their products, or when supplies are scarce.

As things stood right after the introduction of the GST regime, opportunities were readily created for profiteering, thus it called for strict measures right away.

Anti-Profiteering Measures under INDIAN GOODS AND SERVICES TAX ACT, 2017

Understanding profiteering measures is important to excel in any GST course.

The anti-profiteering rules are rather straightforward. If a company falls under a lower tax rate than in the pre-GST era, or if it gets a tax reduction due to the input tax credit, it must pass on those tax benefits to its customers now that GST is here.

The rules say that the firm should come up with a “commensurate reduction in prices” in order to achieve this. It is supposed to do the same if a particular product/ service from the entire product/ service range of the company is moved into a lower GST rate slab.

The government rules do not specify how a Company can pass on these benefits — instead, it gives the anti-profiteering Standing Committee the power to judge each company on an individual basis.

Official GoI measures listed in the GST Act, 2017 are as under :

- Section 171: relates to Anti-Profiteering measures

- Section 171(1): Any reduction in the rate of tax on any supply of goods and services or the benefit of the input tax credit shall be passed on to the recipient by way of commensurate reduction in the prices.

- Section 171(2): The Central Government may, on the recommendation of the Council, by notification, constitute an Authority or empower an existing Authority constituted under any law for the time being in force, to examine whether input tax credits availed by any registered persons or the reduction in the tax rate have actually resulted in a commensurate reduction in the price of the goods and services or both supplied by them.

- Section 171(3): The Authority referred to in sub-section (2) shall exercise such powers and discharge such functions as may be prescribed. In the case of inclusive contracts, in which payment is inclusive of taxes or when there is a reduction in the rate of taxes then the value of supply of goods or services should be reduced accordingly.

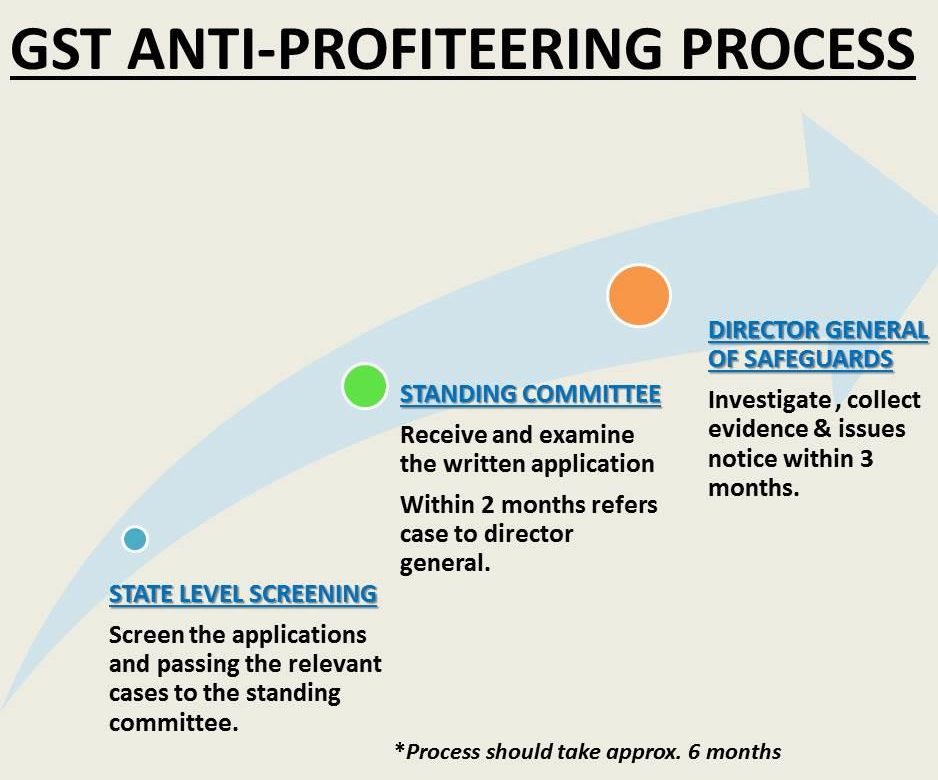

Process of Anti-Profiteering

The following infographic summarizes the entire process generally followed by the Government.

(Courtesy – NewsNow)

Benefits of Anti-Profiteering

Common masses have greatly benefitted from these measures as they are the ones to bear the maximum burden of consumption taxes.

The major benefits have been listed here :

- Reduction in prices of inputs because of a reduction in tax rates.

- Reduction in selling price of output because of a reduction in tax rates.

- Reduction in the number of levies on input and output.

- Preventing end-users from tax exploitation.

An Illustration

Let us assume the applicable tax rate on a particular business was 18% before GST, but that business was subsequently migrated to the 5% slab after GST.

If the business kept its prices the same, the profit margins would increase considerably. As one of the major goals of the GST regime is to create lower prices for consumers, the government would consider this 18-5 = 13% as profiteering. That’s because this 13% is being borne by the consumers and not the business.

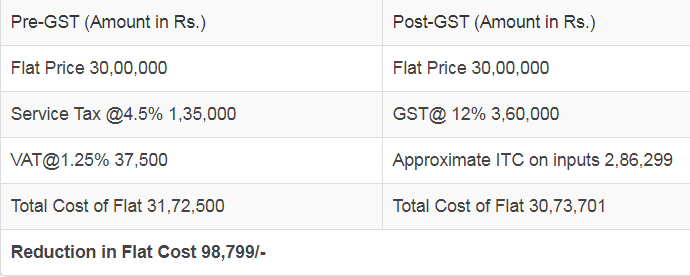

As an example of how to calculate the cost reduction, let us consider the following :

The office of Chief Commissioner of Central Tax and Customs, Vishakhapatnam, in a press note dated 6th December 2017, explained the methodology through which a flat builder, for instance, should calculate benefits and act accordingly.

(Courtesy – GoI)

So there you have it – mumbo jumbo of Anti-profiteering in brief. To learn about other standard GST course topics in detail you may contact us or check out our industry ready GST course.

Please check out our Facebook, Twitter and Instagram pages for informative content.

- 10 of the Best Accounting Software in India (Reviews with detailed comparison) - August 2, 2020

- Top Career Opportunities For Accountants - June 2, 2020

- Data Security in Tally.ERP 9 - June 1, 2020