.jpg)

Learn The Fundamentals of Accounting

Accounting can be described by roughly 3 adjectives – irreplaceable, inevitable and unputdownable! Accounting is something that is required in every single organization but the fundamentals of accounting are rather easy to learn. Be it full-fledged graduation courses or professional accounting courses, there are ample opportunities available in the market to learn this trade.

And guess what, no prior knowledge is required for candidates to join in and make the most of those professional accounting courses!

In the industry, accounting is often called the ‘Language of the Business’. It is the common financial language used to communicate financial information to individuals, organizations, and government agencies about various aspects of business such as financial position, operating results, and cash flows.

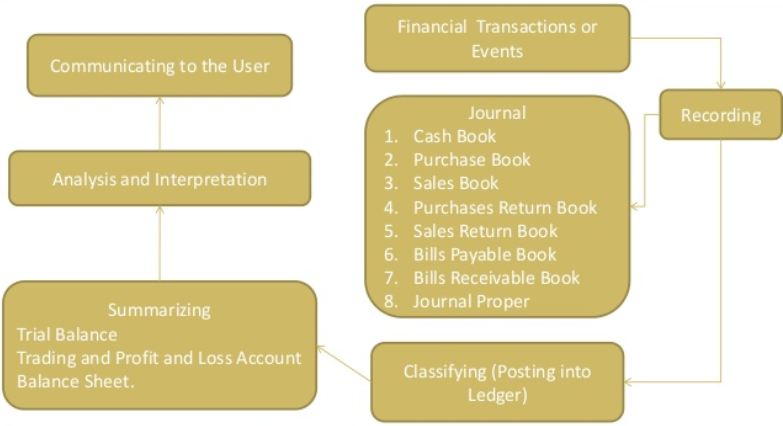

What exactly does the accounting process entail though? Well, everything from recording, classifying, summarizing to interpreting the financial information of an economic unit. This economic unit is generally considered as a ‘separate legal entity’ in accounting terminology.

A professional accounting course module generally starts with the fundamentals and then moves on to the trickier aspects of accounting. Let us now look at what all we are required to learn in order to be proficient in the fundamentals of accounting.

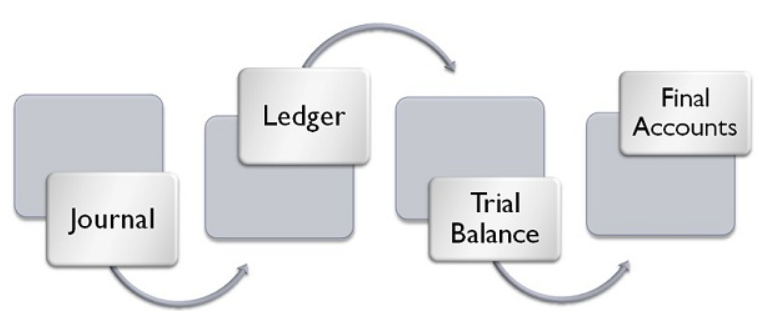

(Accounting Cycle)

Definition

Accounting, as defined by the American Accounting Association (AAA) is the “process of identifying, measuring and communicating economic information to permit informed judgments and decisions by the users of the information.”

Objectives of Accounting

The major objectives of accounting in a nutshell are :

- Keeping a Systematic Record of Transactions.

- Preventing misuse of assets/ funds of the company.

- Communicating ready-made financial results to interested parties.

- Making sure the company follows all prevalent legal protocols when it comes to recording financial transactions.

Accounting Equation

The basic accounting equation, considered as the backbone of accounting is as follows :

Assets = Liabilities + Capital (or Equity)

This equation is based on the principle that accounting is concerned with property and rights value to the property. The sum of the value of property owned is equal to the sum of the value of rights to the property.

The stuff owned by a business is collectively called assets and the rights to properties are called liabilities or equities of the business.

Why traditional? Choose a 90% Practical BBA Degree1-year paid internship + 10 Simulation Software + 4 Certifications that employers are looking for |

|

| BBA in accounting and finance |

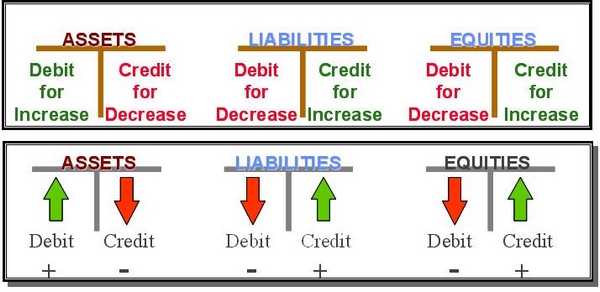

Concept of Debit and Credit

Debit and Credit concepts are imperative to learning the fundamentals of accounting.

Business transactions are those events that have a monetary significance on the financial statements of an organization. When accounting for these transactions, figures are recorded in two different accounts.

A debit is an accounting entry that increases an asset account/ expense account. It can also decrease a liability or equity account. It is recorded on the LHS of the sheet.

A credit is an accounting entry that increases a liability or equity account. It can also decrease an asset or expense account. It is recorded on the RHS of the sheet.

Bookkeeping vs Accounting

Book-keeping is mainly concerned with identifying, measuring and classifying financial transactions. It is the starting point of any activity attempting to record transactions of a concern. Book-keeping forms the basis of accounting. Important decisions cannot be taken by the Management based on book-keeping.

On the other hand, accounting implies processing, summarizing, interpreting and communicating financial transactions in much more detail than bookkeeping. As they say, accounting starts where bookkeeping ends. Management routinely takes important decisions based on accounting.

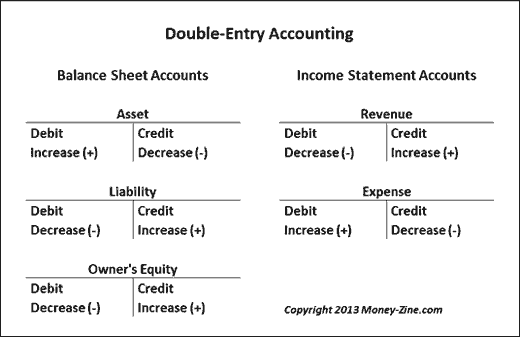

Double Entry System

The Double Entry Book-keeping system is based on the following principle: for every business transaction that takes place, two entries must be made in the accounts books. One is a debit entry (showing goods or value coming into the business) and the other is a corresponding credit entry (showing goods or value going out of the business).

(Courtesy – Money Zine)

Journal and Ledger

Double Entry Book-keeping process starts from journal followed by ledger, trial balance, and final accounts. Journal and Ledger are the two pillars that create the base for preparing final accounts. The Journal is a book where all the transactions are recorded immediately when they take place which is then classified and transferred into a concerned account known as Ledger.

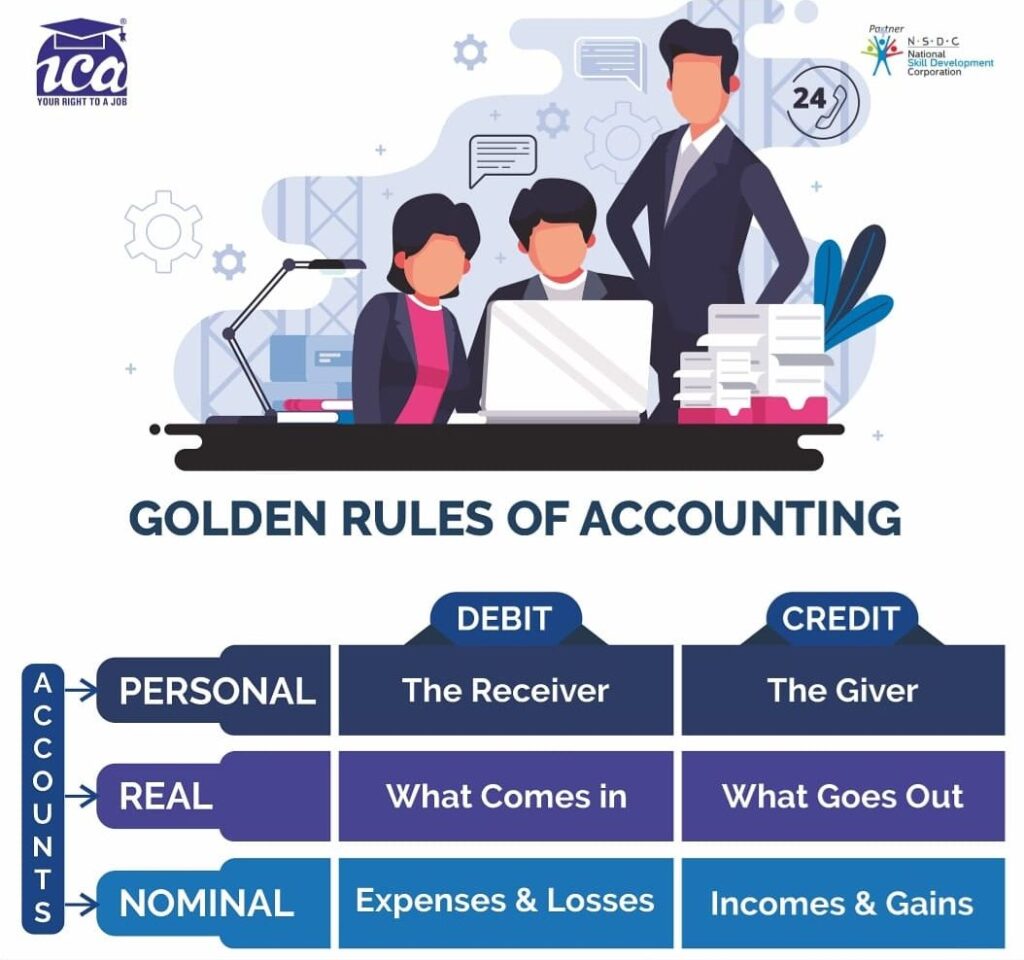

Account types and Golden Rules

Accounts are mainly of 3 types :

- Personal Account – These accounts record business dealing with a person or a firm.

- Real Account – These are mainly assets accounts.

- Nominal Account – These accounts record expenses, incomes, profits, and losses.

Accounting Standards or GAAP

Generally Accepted Accounting Principles (GAAP) refer to a common set of accepted accounting principles, standards, and procedures that businesses must adhere to when preparing and presenting financial statements. GAAP is one of the most important aspects of fundamental accounting.

GAAP is a combination of authoritative standards and the commonly accepted ways of recording and reporting financial information.

At the international level, such authoritative standards are known as International Financial Reporting Standards (IFRS) and in India we have standards are known as AS and IND-AS.

The Institute of Chartered Accountants of India (ICAI) had originally suggested 29 IND-AS but later 2 were deprecated, so currently there are 27 IND-AS standards.

Bases of Accounting

When learning about the fundamentals of accounting one must certainly understand the two bases of accounting which are :

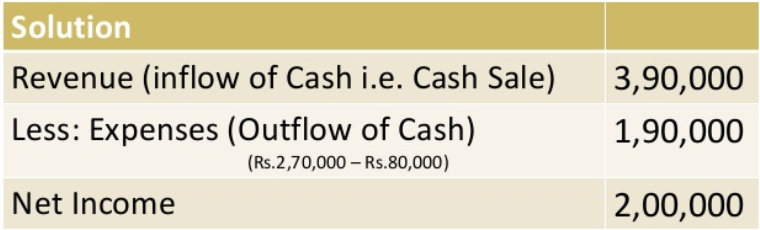

- Cash Basis – It is the method of accounting wherein income is recorded when cash is received and expenses are recorded when cash is paid.

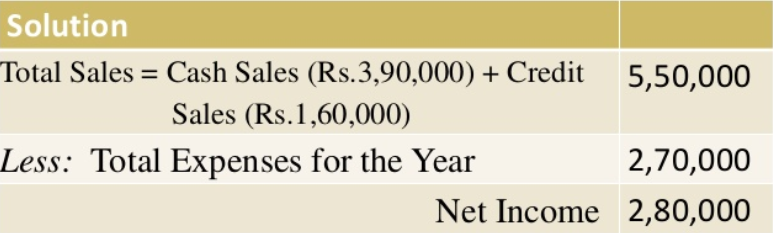

- Accrual Basis – Under this system both income earned and expenditures incurred are recorded irrespective of whether cash comes in or goes out.

For example, let us consider a real-life scenario where :

Amit has cash sales of Rs. 3,90,000 and credit sales of Rs. 1,60,000 during the financial year 2019-20. His expenses for the year were Rs. 2,70,000 out of which Rs. 80,000 are yet to be paid.

This is how we find out Amit’s income for the year 2019-20 under both the above systems of accounting.

Cash Basis :

Accrual Basis :

Well, that’s it for now. I hope this piece surely gave you some introductory ideas about the fundamentals of accounting. And if you are anything like us, the budding accounts manager in you must have gotten excited! Well, in that case, you are in luck . Check out the most in-demand accounting courses after the 12th to scale up your accounting knowledge.

Be sure to check out our Facebook, Twitter, and Instagram pages for more such awesome content!

- 10 of the Best Accounting Software in India (Reviews with detailed comparison) - August 2, 2020

- Top Career Opportunities For Accountants - June 2, 2020

- Data Security in Tally.ERP 9 - June 1, 2020