.jpg)

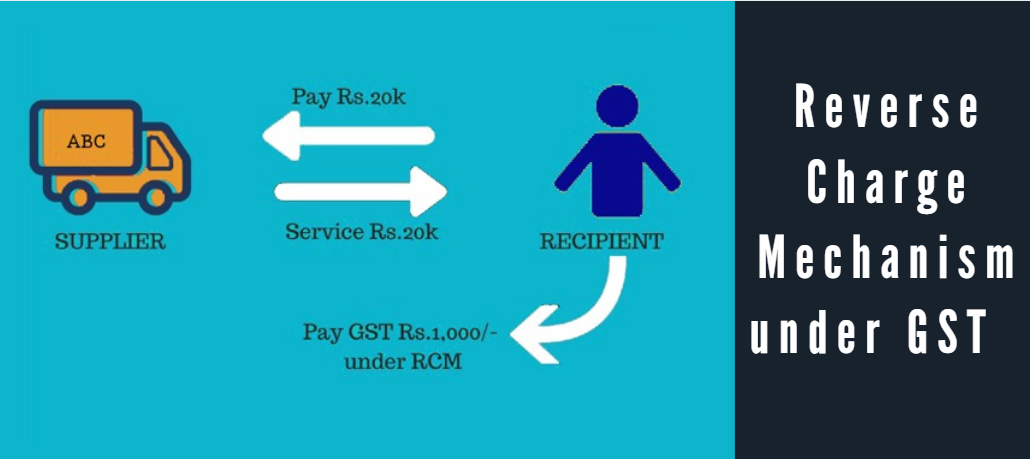

Reverse Charge Mechanism Under GST

GST (Goods and Services Tax) was brought into existence on 1st July 2017 by the Statutory GST Act of 2017. Since then a lot of changes and reforms have been brought about to iron out the wrinkles prevalent in the GST regime. One such modification brought about is the introduction of Reverse Charge Mechanism (RCM) under GST. Understanding this concept is important for students enrolled in a GST course.

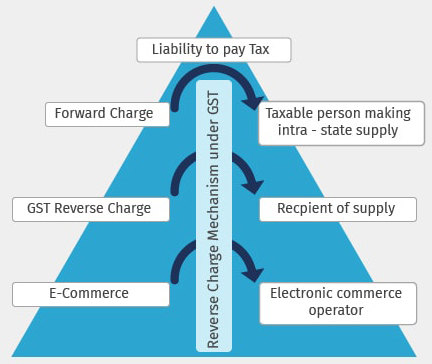

(RCM Schematic – Courtesy of TallySolutions)

What is RCM

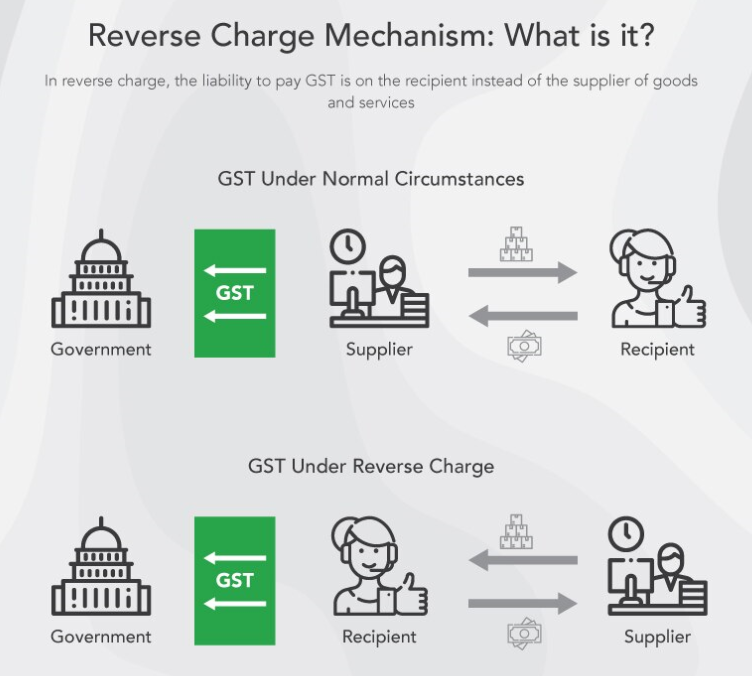

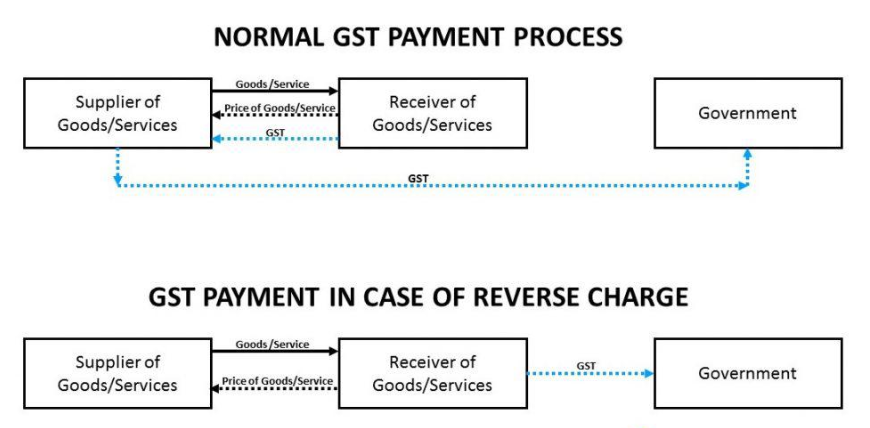

Normally the supplier of goods and services is liable to pay the Goods and Services Tax (GST). However, under the RCM, the receiver of the goods becomes the party that is liable to pay the taxes.

This also implies that all the provisions of the GST Act would be applicable to such a recipient as if he is the person responsible for paying the tax with regards to the supply of goods or services. In other words, in case the recipient is unable to pay the tax under RCM, the supplier holds no liability to pay such a tax.

GoI has defined a few instances in which the reverse charge mechanism is employed. Getting the hang of this can help businesses, their customers, as well as students, enrolled in a GST course understand these transactions better.

(Courtesy of ClearTax)

When is RCM applicable

The applicability of RCM is governed by the rules mentioned in Section 9 (4) of the Central Goods and Service Tax Act, 2017. This is important to understand to succeed if you have enrolled in any GST course.

Recently a change was made by the Government concerning the Reverse Charge Mechanism’s applicability by publishing notification no. 02/2019 on 29th January 2019.

RCM is applicable in the following scenarios.

When a GST registered dealer purchases from an unregistered one :

- If a goods supplier who is not registered as per the GST standards supplies goods or services to a vendor who has registered himself or herself onto the GST platform, then the reverse charge concept will be brought into effect.

- As per this mechanism, the buyer; that is the registered vendor, will have to pay a tax to the Government rather than the unregistered vendor. The buyer will then have to self-invoice the purchase he or she made and later pay Reverse Charge on it.

- If the purchase was made between states, then the buyer has to pay IGST while if the purchase was between vendors within the same state, then the registered vendor has to pay both CGST and SGST under the Reverse Charge Mechanism.

- As per notification no. 8/2017, 28th June 2017 transactions below INR 5,000 a day were exempted from having to pay Reverse Charges.

When an e-commerce operator or dealer is involved :

- If the buying of goods or services were made via an e-commerce operator, then the reverse charge mechanism becomes applicable to the operator, and hence, he or she will have to pay GST.Example: Let’s consider the company UrbanClap is an e-commerce platform that aggregates the services of technicians and using it. It can make available the services of thousands of plumbers, electricians, technicians, etc. As they provide such a service to people in and around a certain vicinity, UrbanClap is given the responsibility of paying the GST for their services, and this liability is lifted off the shoulders of the individual service providers who have listed themselves on the platform.

- If an e-commerce operator is not present in a particular geographical area, then their representative for that area is liable to pay the tax, and if there is no such representative, then the operator is expected to appoint someone for that role and then pay GST.

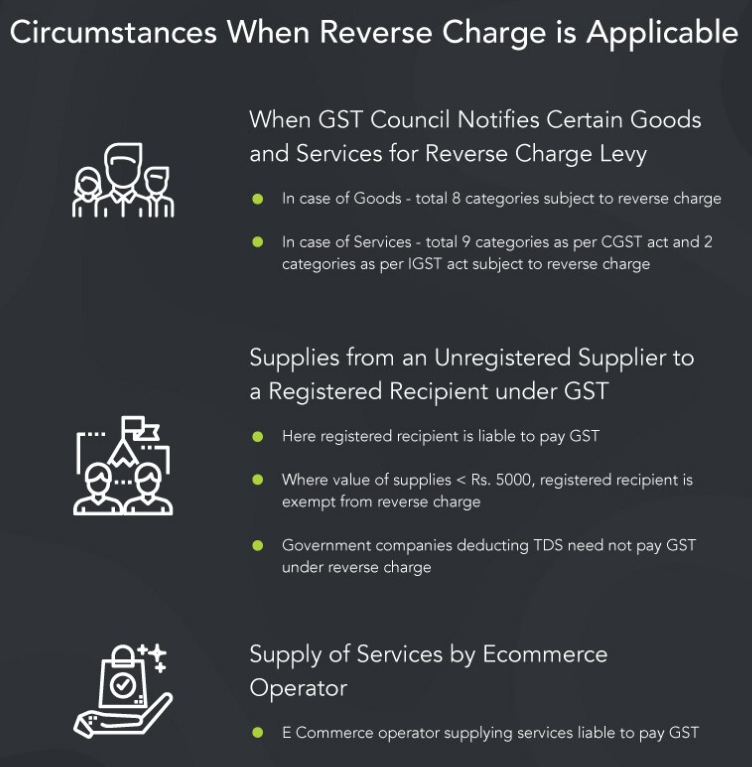

(Courtesy of ClearTax)

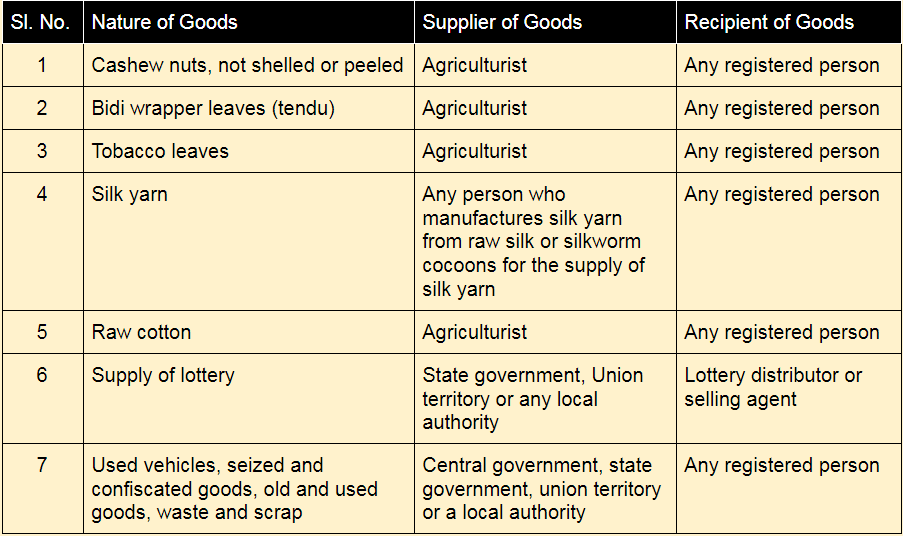

List of Goods under RCM in GST

There are several categories of goods subject to RCM as per section 9(3) of the CGST Act. These are the goods under RCM in GST.

Time Period to Supply Services Under RCM

Under RCM, the time of supply of services shall be the earlier of the following:

- 60 days (2 months) from the date of issue of invoice

- Date of payment

Now, the date of payment shall be taken as the earlier of the following :

- Date on which the amount was debited from the bank account as shown in the bank statement

- Date of recording the payment in the books of accounts by the recipient

Illustration :

Let us understand the above though an illustration like any good GST course would provide.

Suppose Malhotra & Co. Pvt. Ltd. is an unregistered supplier that offers Accounting services to Sharma Ltd and issues an invoice on August 7, 2019.

Now let us assume that the quality of the services offered was not up to the mark, so the payment got delayed, and hence it was made on November 16, 2019. It was made via cheque and the same was recorded in the books of accounts of the recipient.

Now, the time of supply in the above case shall be the earlier of:

- 60 days (2 months) from the date of issue of the invoice (August 7, 2019)

- Date of payment (November 16, 2019)

August 7, 2019, would be effectively the time of supply of services.

Self Invoicing

Section 31 of the CGST Act, 2017 allows a registered recipient subject to reverse charge mechanism is required to issue an invoice.

Self invoicing can be referred to as the process followed whenever a purchase is made from a GST-unregistered vendor. Such purchases come under the ambit of RCM as per GST laws, as discussed earlier.

This occurs because in such cases, the supplier cannot file a GST-compliant invoice as they are not registered on the portal and as a result, become liable to pay the Reverse Charges on their behalf.

As per prevalent GST norms in India, businesses having a turnover lesser Rs. 40 lakh from the sale of goods are not required to register themselves for GST. However, the limit remains at Rs. 20. lakh for service providers. This is an exemption created by the Government of India in order to help newer businesses and startups flourish. The threshold or limit for GST registration in India was Rs. 20 lakh prior to the 31st of March 2019. This limit remains the same for Kerala and Telangana states.

Let’s wrap up by taking a quick look at an infographic summarizing RCM.

(Courtesy of ClearTax)

So that’s it – our primer on Reverse Charge Mechanism under GST. If you’re interested in taking your learning experience further and enroll in a good GST course, you are welcome to try ours.

Check our Facebook, Twitter, and Instagram pages on a daily basis to know more about GST, Accounting, SAP, Advanced Excel, and the like.

- 10 of the Best Accounting Software in India (Reviews with detailed comparison) - August 2, 2020

- Top Career Opportunities For Accountants - June 2, 2020

- Data Security in Tally.ERP 9 - June 1, 2020