.jpg)

A-Z Accounting Terms for Every Aspirant & Professional

Accounting is like the Swiss Army Knife of recording financial transactions. What we’re going to deal with today is the very basic terms of this profession. To pursue any accounting course or any form of accounts training we need to have a solid foundation of the terminologies used in accounting.

Read on to know (or recapitulate) the very basic terminologies of accounting which will help you fly higher than your peers in any accounting course that you may enroll in.

Accounting

A systematic way of recording and reporting financial transactions for a business or organization.

Accounts Payable

The amount of money a company owes creditors (suppliers, etc.) in return for goods and/or services they have delivered.

Accounts Receivable

The amount of money owed by customers or clients to a business after goods or services have been delivered and/or used.

Accounting Period

An Accounting Period is designated in all Financial Statements (Income Statement, Balance Sheet, and Statement of Cash Flows). The period communicates the span of time that is reported in the statements.

Accrued Expense

An expense that been incurred but hasn’t been paid is described by the term Accrued Expense.

Assets (Fixed and Current)

Anything owned by a business that lends tangible or intangible value (including monetary value) to the business might be termed as assets.

Current assets (CA) are those that will be converted to cash within a year. Typically, this could be cash, inventory or accounts receivable. Fixed assets (FA) are long-term and will likely provide benefits to a company for more than one year, such as a real estate, land or major machinery.

Asset classes

An asset class is a group of securities that behaves similarly in the marketplace. The three main asset classes are equities or stocks, fixed income or bonds, and cash equivalents or money market instruments.

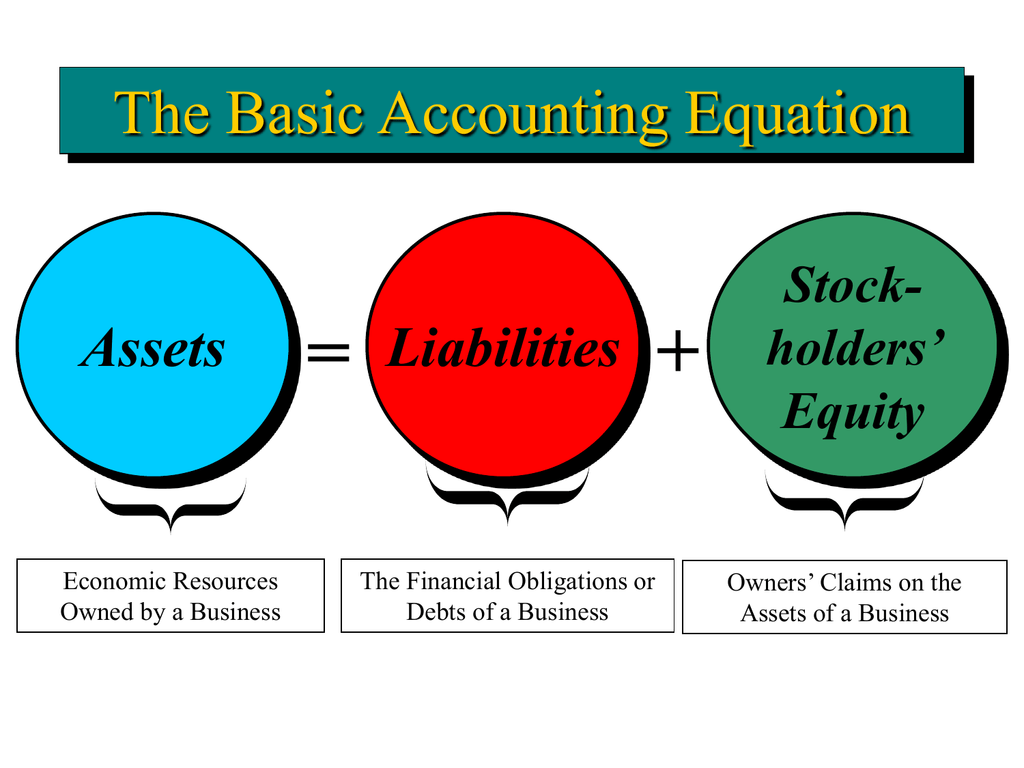

Balance sheet

A financial report that summarizes a company’s assets (what it owns), liabilities (what it owes) and owner or shareholder equity at a given time.

A balance sheet abides by the basic accounting equation.

Basic Accounting Equation

Assets = Liabilities + (Owner’s) Equity

The accounting equation is considered to be the foundation of the double-entry accounting system. The accounting equation shows on a company’s balance sheet whereby the total of all the company’s assets equals the sum of the company’s liabilities and shareholders’ equity.

Based on this double-entry system, the accounting equation ensures that the balance sheet remains “balanced,” and each entry made on the debit side should have a corresponding entry (or coverage) on the credit side.

Carefully note down this equation in your memory for any accounting course you might end up enrolling in.

Book Value

As an asset is depreciated, it loses value. The Book Value shows the original value of an Asset, less any accumulated Depreciation.

Bonds and coupons

A bond is a form of debt investment and is considered a fixed income security. An investor, whether an individual, company, municipality or government, loans money to an entity with the promise of receiving their money back plus interest.

The “coupon”, sometimes called the “coupon rate” is the annual interest rate paid on a bond.

(One of the first ever US bonds)

Business Entity

This is the legal structure, or type, of a business. Common company formations include Sole Proprietor, Partnership, Limited Liability Corporation (LLC), Public Limited Company (Ltd.), Private Limited Company (Pvt. Ltd.) etc. Each entity has a unique set of requirements, laws, and tax implications.

Capital

A financial asset or the value of a financial asset, such as cash or goods. Working capital is calculated by taking your current assets subtracted from current liabilities—basically the money or assets an organization can put to work.

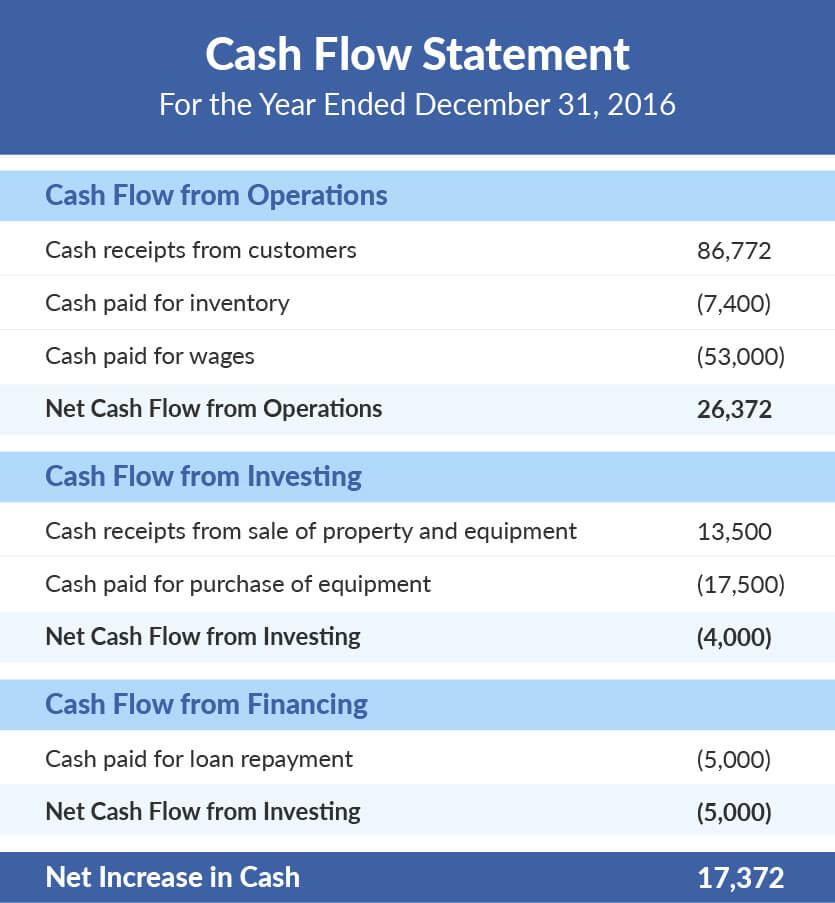

Cash Flow

The revenue or expense expected to be generated through business activities (sales, manufacturing, etc.) over a period of time.

Cost of Goods Sold

The direct expenses related to producing the goods sold by a business. The formula for calculating this will depend on what is being produced, but as an example this may include the cost of the raw materials (parts) and the amount of employee labor used in production.

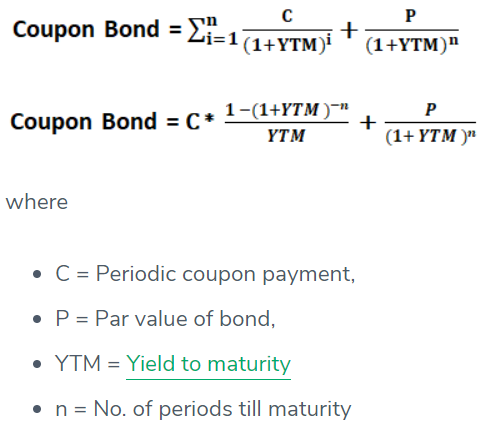

Coupon Bond Formula

The term “coupon bond” refers to bonds that pay coupons which is a nominal percentage of the par value or principal amount of the bond. The formula for calculation of the price of this bond basically uses the present value of the probable future cash flows in the form of coupon payments and the principal amount which is the amount received at maturity. The present value is computed by discounting the cash flow using yield to maturity.

Credit

An accounting entry that may either decrease assets or increase liabilities and equity on the company’s balance sheet, depending on the transaction. When using the double-entry accounting method there will be two recorded entries for every transaction: A credit and a debit.

Debit

An accounting entry where there is either an increase in assets or a decrease in liabilities on a company’s balance sheet.

Diversification

The process of allocating or spreading capital investments into varied assets to avoid over-exposure to risk.

Expenses

The fixed, variable, accrued or day-to-day costs that a business may incur through its operations.

Fixed expenses : payments like rent that will happen in a regularly scheduled cadence.

Variable expenses : expenses, like labor costs, that may change in a given time period.

Accrued expense : an incurred expense that hasn’t been paid yet.

Operation expenses : business expenditures not directly associated with the production of goods or services—for example, advertising costs, property taxes or insurance expenditures.

Equity and owner’s equity

In the most general sense, equity is assets minus liabilities. An owner’s equity is typically explained in terms of the percentage of stock a person has ownership interest in the company. The owners of the stock are known as shareholders.

Recall the Basic Accounting Equation Assets = Liabilities + Equity.

Fixed Cost

A Fixed Cost is one that does not change with the volume of sales. For example, rent and salaries won’t change if a company sells more. The opposite of a Fixed Cost is a Variable Cost.

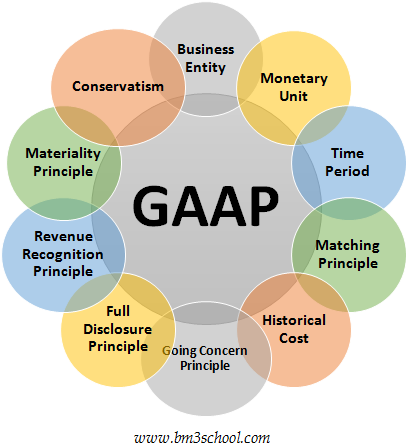

Generally accepted accounting principles (GAAP)

A set of rules and guidelines developed by the accounting industry for companies to follow when reporting financial data. Following these rules is especially critical for all publicly traded companies.

(Courtesy – www.bm3school.com)

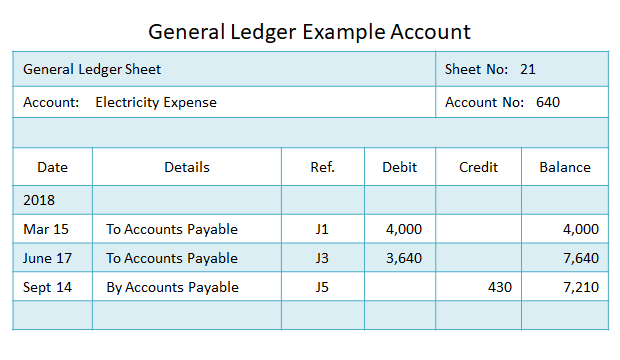

General ledger

A complete record of the financial transactions over the life of a company.

Insolvency

A state where an individual or organization can no longer meet financial obligations with lender(s) when their debts come due.

Interest

Interest is the amount paid on a loan or line of credit that exceeds the repayment of the principal balance.

Inventory

Inventory is the term used to classify the assets that a company has purchased to sell to its customers that remain unsold. As these items are sold to customers, the inventory account will decrease in value.

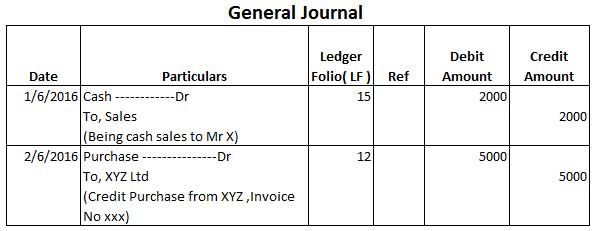

Journal Entry

Journal Entries are how updates and changes are made to a company’s books. Every Journal Entry must consist of a unique identifier (to record the entry), a date, a debit/credit, an amount, and an account code (that determines which account is altered).

Liabilities (current and long-term)

A company’s debts or financial obligations incurred during business operations. Current liabilities (CL) are those debts that are payable within a year, such as a debt to suppliers. Long-term liabilities (LTL) are typically payable over a period of time greater than one year. An example of a long-term liability would be a multi-year mortgage for office space.

Limited liability company (LLC)

An LLC is a corporate structure where members cannot be held accountable for the company’s debts or liabilities. This can shield business owners from losing their entire life savings if, for example, someone were to sue the company.

Liquidity

A term referencing how quickly something can be converted into cash. For example, stocks are more liquid than a house since you can sell stocks (turning it into cash) more quickly than real estate.

Material

Material is the term that refers whether information influences decisions. For example, if a company has revenue in the lakhs of rupees, an amount of 0.50 paisa is hardly material.

GAAP requires that all Material considerations must be disclosed.

Net Income

A company’s total earnings, also called net profit. Net income is calculated by subtracting total expenses from total revenues.

On Credit/On Account

A purchase that happens On Credit or On Account is a purchase that will be paid at a future time, but the buyer gets to enjoy the benefit of that purchase immediately.

For example, if you buy an accounting course now and pay for it later, you’ve made an ‘on credit’ purchase.

Overhead

Overhead are those Expenses that relate to running the business. They do not include Expenses that make the product or deliver the service. For example, Overhead often includes Rent, and Executive Salaries.

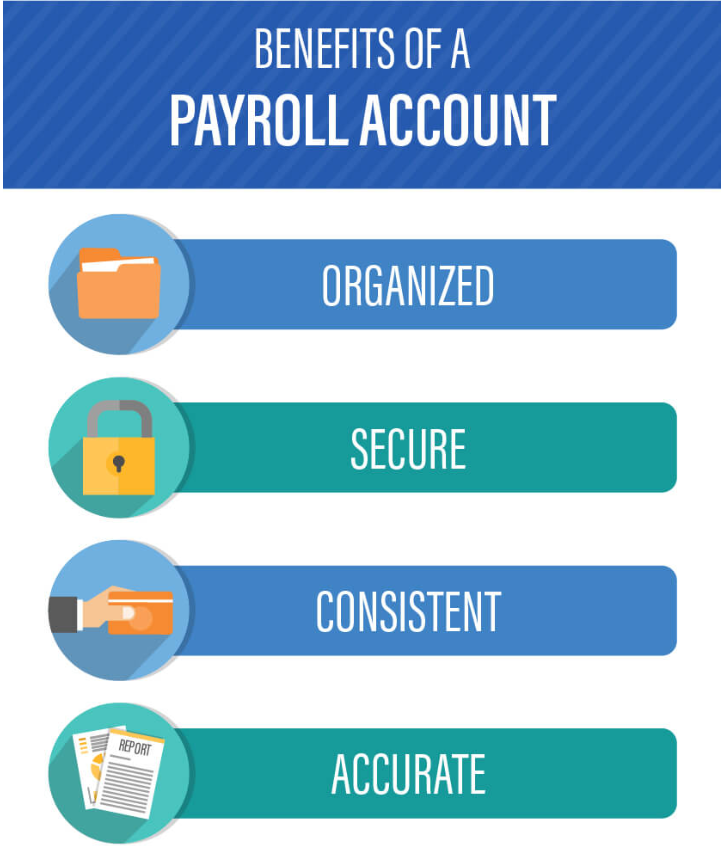

Payroll

Payroll is the account that shows payments to employee salaries, wages, bonuses, and deductions. Often this will appear on the Balance Sheet as a Liability that the company owes if there is accrued vacation pay or any unpaid wages.

Present value

The current value of a future sum of money based on a specific rate of return. Present value helps us understand how receiving Rs. 10,000 for an accounting course now is worth more than receiving Rs. 10,000 a year from now, as money in hand now has the ability to be invested at a higher rate of return.

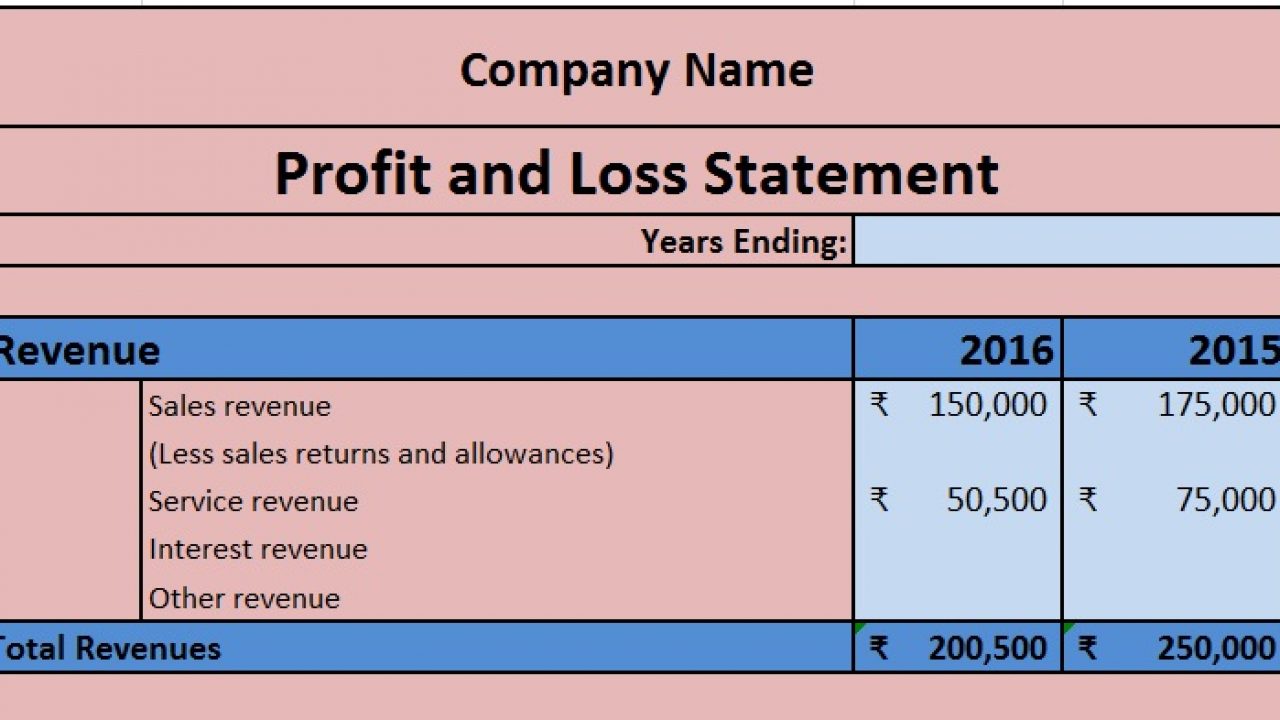

Profit and loss statement

A financial statement that is used to summarize a company’s performance and financial position by reviewing revenues, costs and expenses during a specific period of time, such as quarterly or annually.

Return on investment

A measure used to evaluate the financial performance relative to the amount of money that was invested. The ROI is calculated by dividing the net profit by the cost of the investment. The result is often expressed as a percentage.

Revenue

Revenue is any money earned by the business.

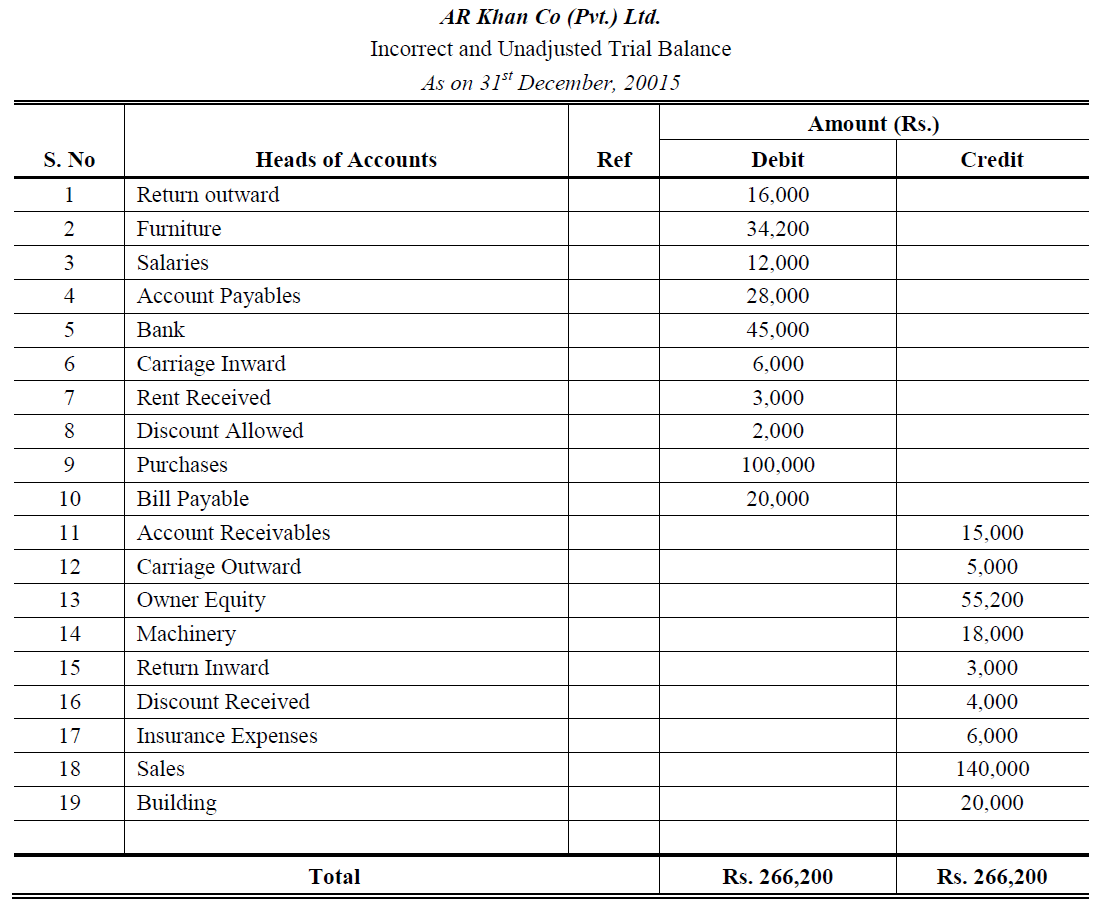

Trial Balance

Trial Balance is a listing of all accounts in the General Ledger with their balance amount (either debit or credit). The total debits must equal the total credits, hence the balance.

Variable Cost

These are costs that change with the volume of sales and are the opposite of Fixed Costs. Variable costs increase with more sales because they are an expense that is incurred in order to deliver the sale.

For example, if a company sells an accounting course and more students enroll in it each day, it will require more faculty members in order to meet the increase in demand.

I hope you had fun reading our almost comprehensive list of accounting terminologies. We recommend a careful study and conceptual understanding of all these terms before enrolling in any accounting course, such as ours.

Do check out our Facebook, Twitter and Instagram pages for more such informative content!

[blogcta url=”https://www.icacourse.in/online-accounting-courses/” label=”Online Accounting Courses”]

Explore the Best Accounting Certification Training and Courses

[/blogcta]

- 10 of the Best Accounting Software in India (Reviews with detailed comparison) - August 2, 2020

- Top Career Opportunities For Accountants - June 2, 2020

- Data Security in Tally.ERP 9 - June 1, 2020